Last Update 22 Jun 26

SEER: Activist Bid And Buybacks Will Test Bullish Repricing Thesis

Analysts have raised their price target on Seer to $4.00, citing updated assumptions for higher revenue growth, a modestly higher discount rate, and a lower future P/E multiple as the key drivers of this revised view.

What’s in the News for Seer

- Bradley L. Radoff and Michael Torok reaffirmed a fully financed proposal to acquire Seer for $2.40 per share in cash plus a contingent value right for 80% of net asset sale proceeds, and issued an open letter on May 27, 2026, alleging the board’s rejection reflects an apparent breach of fiduciary duty and launching a preliminary proxy filing to seek three board seats. (Source: Activist communication, May 27, 2026)

- Seer’s board has repeatedly rejected revised unsolicited non binding proposals from the Radoff JEC Group, most recently on May 21, 2026 for an offer of $2.40 per share in cash plus a contingent value right, stating that the proposal significantly undervalues the company and is not in the best interests of stockholders. (Source: Company announcements, April 27 to May 21, 2026)

- Radoff and Torok escalated their campaign throughout April and May 2026, moving from an initial $2.25 per share non binding offer to $2.35 and then $2.40, while criticizing Seer’s leadership and seeking to replace three directors with their own nominees at the 2026 annual meeting. (Source: Activist and nomination related communications, April 13 to May 14, 2026)

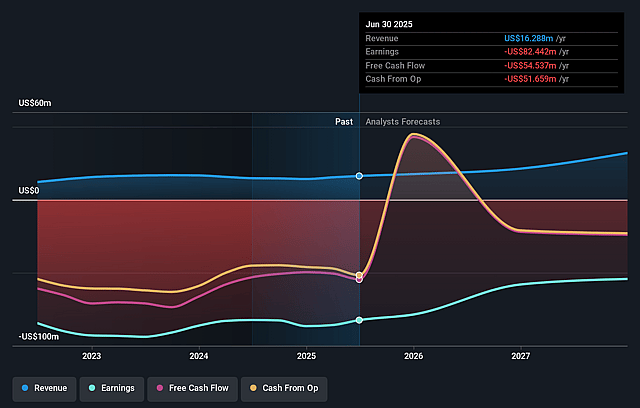

- Seer reaffirmed full year 2026 revenue guidance of US$16 million to US$18 million. The company described this as representing 3% growth at the midpoint compared with full year 2025 revenue. (Source: Corporate guidance, March 2026)

- From January 1 to March 31, 2026, Seer repurchased 1,461,747 shares for US$2.6 million. The company reported that it has now completed repurchases of 13,196,658 shares for US$24.54 million under the buyback that was announced on May 8, 2024. (Source: Buyback tranche update, March 2026)

Valuation Changes for Seer

- Fair Value: Updated price target is set at $4.00 per share, broadly in line with the prior $4 fair value estimate.

- Discount Rate: The discount rate has risen slightly from 8.24% to about 8.38%, reflecting a modestly higher required return in the model.

- Revenue Growth: The revenue growth assumption has risen from about 19.65% to roughly 25.98%.

- Net Profit Margin: The assumed net profit margin is broadly unchanged, moving marginally from about 15.57% to roughly 15.57%.

- Future P/E: The future P/E multiple has been reduced from roughly 64.25x to about 55.02x, indicating a lower valuation multiple applied to projected earnings.

Key Takeaways

- Strategic investments in commercial infrastructure and leadership aim to support revenue growth through increased productivity and sales effectiveness.

- Expanding partnerships and product innovation target enhanced adoption and customer value, potentially boosting sales and overall gross margins.

- Reliance on large contracts and macroeconomic challenges may restrict revenue growth and profitability, compounded by high expenses and prolonged sales ramp-up times.

Catalysts

About Seer- A life sciences company, develops and commercializes products to decode the biology of the proteome.

- Seer anticipates expanding its customer base and enhancing access to its Proteograph Product Suite, which is expected to drive revenue growth as more institutions adopt their technology for various research applications.

- The company plans to drive product innovation and application expansion, which could enhance customer value propositions leading to an increase in consumable sales and service revenue, potentially boosting overall gross margins.

- Seer has made strategic investments in its commercial infrastructure, including doubling the size of its commercial team and onboarding new leadership in sales. This is expected to support revenue growth in 2025 as these new hires become more productive.

- The expanded partnership with Thermo Fisher is expected to enhance commercial reach and drive adoption of the Proteograph Product Suite, potentially increasing sales of instruments and consumables and thus impacting revenue positively.

- Continued validation of Seer's platform by generating more customer publications and compelling research is expected to drive broader adoption of its technology, paving the way for increased revenue from both product sales and related services.

Seer Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Seer's revenue will grow by 26.0% annually over the next 3 years.

- Analysts are not forecasting that Seer will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Seer's profit margin will increase from -464.8% to the average US Life Sciences industry of 15.6% in 3 years.

- If Seer's profit margin were to converge on the industry average, you could expect earnings to reach $4.7 million (and earnings per share of $0.09) by about June 2029, up from -$70.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 55.1x on those 2029 earnings, up from -1.4x today. This future PE is greater than the current PE for the US Life Sciences industry at 40.5x.

- Analysts expect the number of shares outstanding to decline by 2.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company experienced a decrease in revenue by 15% in 2024 compared to 2023, with lower product sales and no grant revenue recognized, impacting overall financial performance. This could affect future revenue growth and the company's ability to achieve profitability.

- The ongoing macroeconomic challenges and budget constraints, particularly in government and academic funding such as the NIH, introduce uncertainty that could restrict the purchasing capacity of Seer's primary customer base, potentially impacting future revenues.

- Seer's total operating expenses in 2024 were substantial at $107.2 million, and although they decreased compared to 2023, the high expenses contributed to a significant net loss of $86.6 million for the year. Sustained losses could put pressure on the company's financial stability and earnings.

- The company's reliance on a few large biopharma and government contracts exposes it to risks associated with budgetary fluctuations and funding uncertainties, which may lead to volatility in revenue streams and financial projections.

- The lengthy ramp-up time for new sales representatives (6 to 9 months) and the anticipated variability in gross margins suggest potential challenges in rapidly scaling revenue and maintaining consistent profit margins, impacting short-term earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $4.0 for Seer based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $30.3 million, earnings will come to $4.7 million, and it would be trading on a PE ratio of 55.1x, assuming you use a discount rate of 8.4%.

- Given the current share price of $1.74, the analyst price target of $4.0 is 56.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Seer?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.