Last Update 29 Jul 26

Fair value Decreased 33%JUSH.F: DEA Schedule III Registrations And U.S. Domestication Will Support Rerating

Analysts have reduced their price target for Jushi Holdings to $1.00 from $1.50, citing updated assumptions that include a slightly higher discount rate, a modestly lower revenue growth outlook, improved profit margin expectations, and a lower future P/E multiple.

What’s in the News for Jushi Holdings

- On June 24, 2026, Jushi Holdings shareholders approved a special resolution at the 2026 Annual General and Special Meeting to move forward with a plan of arrangement under Section 288 of the Business Corporations Act of British Columbia. Source: Management Information Circular and Proxy Statement Appendix A.

- The approved plan of arrangement includes the continuance and domestication of Jushi Holdings from the laws of British Columbia, Canada, to the laws of the State of Nevada in the United States, as outlined in the company’s Circular.

- Jushi Holdings submitted applications to the U.S. Drug Enforcement Administration for registration of certain state-licensed medical marijuana operations under the federal framework that followed the rescheduling of medical marijuana to Schedule III under the Controlled Substances Act. Source: company announcement.

- The DEA introduced a streamlined registration pathway for qualified state-licensed medical marijuana operators that submit applications within an initial 60-day filing window, which may allow expedited registrations for manufacturing, distributing, and dispensing Schedule III medical cannabis products.

- Jushi Holdings stated that its DEA applications are intended to position the company within the evolving federal framework while it continues to serve medical patients under applicable state medical cannabis laws.

Valuation Changes for Jushi Holdings

- Fair Value has been reduced from $1.50 to $1.00, which reflects a lower implied price level for Jushi Holdings.

- Discount Rate has risen slightly from 9.43% to 9.84%, indicating a modestly higher required return in the updated assumptions.

- Revenue Growth has been trimmed slightly from 13.40% to 13.05%, signaling a more cautious outlook for future $ revenue expansion.

- Net Profit Margin has increased from 19.69% to 21.47%, implying higher expected profitability on each $ of revenue in the model.

- Future P/E has been reduced from 5.36x to 3.35x, which points to a lower valuation multiple being applied to Jushi Holdings earnings in the forecast period.

Key Takeaways

- Regulatory changes in key states and at the federal level could unlock new markets, enhance margins, and increase liquidity for Jushi.

- Strategic retail expansion and product innovation are expected to drive higher revenue, lower costs, and capture greater market share.

- Eroding profit margins, high debt, geographic concentration, and regulatory uncertainty heighten risks to Jushi's growth, earnings stability, and future expansion opportunities.

Catalysts

About Jushi Holdings- A vertically integrated cannabis company, engages in the cultivation, processing, retail, and distribution of cannabis for the medical and adult-use markets in the United States.

- The company is poised to benefit from expected regulatory shifts in Pennsylvania and Virginia, where bipartisan and bicameral discussions on adult-use legalization and favorable gubernatorial election polling could unlock significant increases in Jushi's addressable market. If realized, this would provide a material uplift to revenue, cash flow, and operating margins by leveraging existing infrastructure and underutilized fixed costs.

- Expansion of Jushi's retail footprint, particularly in strategically selected, limited-license states such as Ohio and New Jersey, aligns with growing consumer demand, adding new revenue streams and improving scale efficiencies, which should further support margin expansion over the next several quarters.

- Implementation of vertically integrated cultivation and processing improvements, along with planned canopy expansions, are projected to drive lower unit costs and enhance yields; this positions Jushi to capture greater gross profit and expand net margins as new harvests come online and adult-use sales ramp up.

- Broadening and innovating within the branded product portfolio-such as the launch of new high-margin SKUs and strong proprietary brands-positions Jushi to capture a greater share of the mainstream wellness and cannabis-derived product markets, potentially increasing average transaction values and strengthening overall gross margin.

- Anticipated federal-level reforms, including more favorable tax treatment and potential rescheduling of cannabis, could significantly improve access to capital, reduce non-cash expenses, and enhance liquidity, positively impacting earnings and making Jushi more attractive from a financial standpoint if and when regulatory changes materialize.

Jushi Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

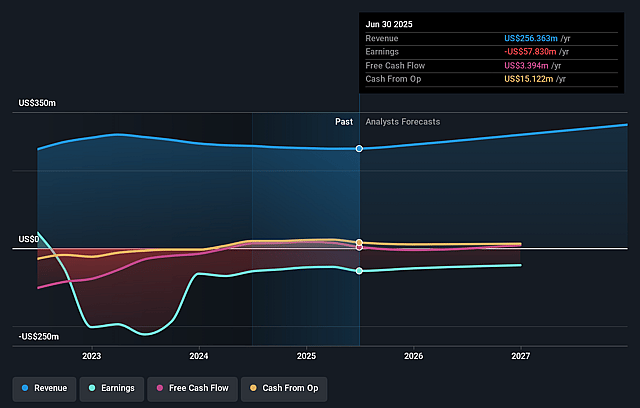

- Analysts are assuming Jushi Holdings's revenue will grow by 13.1% annually over the next 3 years.

- Analysts are not forecasting that Jushi Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Jushi Holdings's profit margin will increase from -26.9% to the average US Pharmaceuticals industry of 21.5% in 3 years.

- If Jushi Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $82.4 million (and earnings per share of $0.39) by about July 2029, up from -$71.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 3.4x on those 2029 earnings, up from -1.1x today. This future PE is lower than the current PE for the US Pharmaceuticals industry at 15.5x.

- Analysts expect the number of shares outstanding to grow by 1.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.84%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent competitive pricing pressure across key retail markets, as noted by management, continues to erode gross profit margins (from 50% a year ago to 44%), causing revenue growth to outpace profitability and creating risk to future net margins and earnings.

- Material declines in wholesale revenue-particularly in Virginia and Massachusetts-demonstrate Jushi's growing reliance on internal retail channels and expose the company to risks from limited geographic diversification and heightened market concentration, which could increase revenue volatility.

- Jushi remains burdened by significant debt ($192 million outstanding), with future refinancing subject to uncertain industry conditions and cost of capital; this leverage, alongside continued net losses, increases risk of future dilution or limits ability to fund growth, ultimately impacting earnings per share.

- The company's aggressive retail expansion is increasingly being scaled back in favor of capital-light projects, reflecting a need for prudent cash management but also highlighting the risk of saturating markets and possibly slower top-line growth than originally anticipated, affecting both revenues and future expansion opportunities.

- The outlook for growth is heavily dependent on uncertain state-level regulatory changes (e.g., adult-use legalization in Pennsylvania and Virginia) and favorable macro trends; any delays, failure to enact reform, or continued pressure from illicit channels and hemp-derived cannabinoids could constrain Jushi's addressable market, impairing revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $1.0 for Jushi Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $383.6 million, earnings will come to $82.4 million, and it would be trading on a PE ratio of 3.4x, assuming you use a discount rate of 9.8%.

- Given the current share price of $0.39, the analyst price target of $1.0 is 61.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Jushi Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.