Last Update 30 Jun 26

Fair value Increased 18%BANDHANBNK: Fair Value Reset Puts Execution And Governance Under Closer Scrutiny

Analysts have lifted their blended fair value estimate for Bandhan Bank to about ₹194 from roughly ₹165, reflecting updated assumptions around revenue growth, profitability, discount rate and forward P/E. These changes are broadly consistent with the kind of thesis shifts seen in recent Street research, where higher price targets were linked to improved monetization opportunities, stronger recurring revenues and perceived competitive advantages.

Analyst Commentary

Analysts covering Bandhan Bank are treating the higher fair value estimate as a reflection of shifting assumptions around how effectively the bank can convert its opportunities into sustainable earnings, rather than as a call on near term share price moves. The Street research on Bandwidth, while focused on a different company, gives a useful template for how analysts think through valuation when monetization drivers, recurring revenues and perceived competitive positioning start to reframe the long term earnings power story.

Taking cues from that research pattern, the current stance on Bandhan Bank can be grouped into areas where bullish analysts see upside to the fair value framework, and areas where more cautious voices are focused on execution and risk management.

Bullish Takeaways

- Bullish analysts point to the higher blended fair value estimate of about ₹194 as evidence that the underlying earnings framework for Bandhan Bank, including assumptions on revenue mix and profitability, now screens better than in earlier models.

- The revised assumptions echo how analysts have treated companies with expanding monetization channels, suggesting that if Bandhan Bank can deepen fee income and improve yield on existing customer relationships, there could be more support for current valuation multiples.

- Stronger recurring style revenue streams, such as stable interest income from a seasoned loan book and predictable fee flows, are viewed as key for justifying the updated P/E assumptions that underpin the new fair value work on Bandhan Bank.

- Perceived competitive advantages in the bank's core segments, such as strong local franchise strength or differentiated distribution, are being treated as factors that can support execution on growth plans without requiring aggressive discount rate assumptions.

Bearish Takeaways

- More cautious analysts focus on the fact that a higher fair value estimate also tightens the margin for error, so any slip in Bandhan Bank's execution on asset quality, deposit growth or operating costs could put pressure on the revised P/E and earnings assumptions.

- There is concern that comparisons to companies with rapidly growing recurring software revenues may not fully translate to a bank context, which could leave Bandhan Bank vulnerable if actual revenue growth patterns differ from the scenarios embedded in the fair value models.

- Some bearish analysts highlight that the uplift in fair value is sensitive to assumptions around discount rates and long term profitability, meaning a shift in funding costs or credit risk could require another reset of the valuation framework.

- The focus on perceived competitive advantages also carries risk, as any loss of differentiation in Bandhan Bank's key markets, including increased competition for deposits or loans, could challenge the thesis that supports a richer valuation multiple.

What’s in the News for Bandhan Bank

- A board meeting is scheduled for Jun 25, 2026 to review and consider the capital plan of Bandhan Bank, source: Key Developments.

- There is a proposal to appoint Mr. Debasish Panda as an Additional Independent Director on the board from Jul 05, 2026 for a three-year term, subject to shareholder approval, source: Key Developments.

- Bandhan Bank plans to designate Mr. Debasish Panda as Non Executive Chairman for a three-year period starting Jul 05, 2026, subject to shareholder approval, source: Key Developments.

- A special/extraordinary shareholders meeting via postal ballot is scheduled for Jun 05, 2026 to consider the appointment of Mr. Debashish Mukherjee as an independent director, source: Key Developments.

- A board meeting will be held on Apr 28, 2026 to consider audited financial results for Q4 and the financial year ended Mar 31, 2026, and to consider recommending a dividend, if any, source: Key Developments.

Valuation Changes for Bandhan Bank

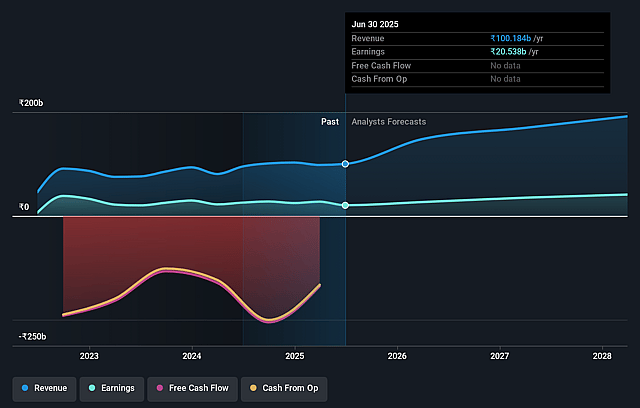

- Fair Value: The blended fair value estimate has risen from about ₹165.21 to roughly ₹194.21, indicating a higher assessed worth for Bandhan Bank shares in updated models.

- Discount Rate: The discount rate has edged down slightly from 14.04% to about 13.95%, implying a modestly lower required rate of return in the valuation work.

- Revenue Growth: Assumed revenue growth has been reduced from roughly 40.56% to about 29.35%, signalling more moderate growth expectations in the updated framework while still using ₹ as the reporting currency.

- Net Profit Margin: The assumed net profit margin has increased from around 17.05% to about 20.99%, pointing to higher expected earnings retention per ₹ of revenue in the Bandhan Bank model.

- Future P/E: The forward P/E multiple has moved slightly higher from about 10.47x to roughly 10.75x, indicating a small uplift in the earnings multiple used for Bandhan Bank.

Key Takeaways

- Diversifying into non-microfinance segments and strengthening the deposit base are reducing risk, stabilizing earnings, and supporting higher net interest margins.

- Digital innovations and a favorable macro environment are driving operational efficiencies, supporting growth in revenue, fee income, and long-term profitability.

- Elevated credit risk in microfinance, margin pressure, intense competition, geographic concentration, and legacy portfolio stress threaten profitability, growth, and stability.

Catalysts

About Bandhan Bank- Engages in the provision of banking and financial services for personal and business customers in India.

- The ongoing recovery and expected normalization in the microfinance (EEB) portfolio, aided by disciplined implementation of new industry guardrails and improving asset quality, should restore above-industry loan growth from Q3 FY26 onwards-supporting topline revenue and loan growth.

- Continued strong growth in the bank's non-EEB segments-especially secured retail, housing, and wholesale banking loans (growing 27%+ YoY)-and further asset mix diversification are likely to reduce concentration risk and credit costs, leading to more stable earnings and improved net interest margins.

- Robust growth in retail term deposits (up 34% YoY) and the strategic shift towards a more granular, stable deposit base, alongside targeted efforts to boost CASA, are expected to lower funding costs, improving net interest margins and supporting profitability.

- Investments in digital collections (e.g., WhatsApp communication, QR-based customer payments), process automation, and advanced analytics are poised to drive further operational efficiencies, reduce cost-to-income ratios, and enhance overall net margins.

- The supportive macro environment-marked by resilient GDP growth, falling interest rates, government-backed financial inclusion efforts, and rising per capita incomes-should fuel greater demand for formal credit, deposit products, and fee-based services, benefitting revenue and fee income streams and underpinning long-term earnings power.

Bandhan Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Bandhan Bank's revenue will grow by 29.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.0% today to 21.0% in 3 years time.

- Analysts expect earnings to reach ₹42.9 billion (and earnings per share of ₹26.61) by about June 2029, up from ₹12.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹56.4 billion in earnings, and the most bearish expecting ₹35.7 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.8x on those 2029 earnings, down from 26.9x today. This future PE is lower than the current PE for the IN Banks industry at 12.1x.

- Analysts expect the number of shares outstanding to decline by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.95%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistently high credit risk in the microfinance (EEB) portfolio-evidenced by elevated slippages, high NPA ratios, ongoing technical write-offs, and management's expectation that EEB challenges will persist at least into the next quarter-could lead to continued elevated provisioning and impairments, which may weigh on net margins and earnings.

- Margin (NIM) compression is likely to continue in the near to medium term due to a combination of asset mix shift towards lower-yielding secured loans, declining microfinance yields (with no scope for rate hikes), and moderating cost reductions; this reduces profitability potential even if overall loan growth resumes.

- Intense competition and tightening regulatory guardrails in core microfinance geographies and segments have led to higher rejection rates (16-18% of loan applicants now ineligible), regional growth challenges (e.g., muted growth in Tamil Nadu and Karnataka), and constrain both volume and pricing power, impeding revenue growth and customer acquisition.

- Bandhan Bank remains highly geographically concentrated in eastern India (West Bengal and Bihar representing substantial portions of assets and liabilities), making it particularly vulnerable to local economic shocks, policy interventions, or political disruptions, elevating risk to asset quality and causing earnings volatility.

- The bank's old vintage unsecured and group lending portfolios are increasingly showing stress-with NPA ratios in aged books and some retail and housing portfolios rising-indicating that incomplete asset mix diversification and legacy portfolio issues may continue to drag on normalized profitability and pose risks to long-term revenue and margin recovery.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹194.21 for Bandhan Bank based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹250.0, and the most bearish reporting a price target of just ₹130.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹204.2 billion, earnings will come to ₹42.9 billion, and it would be trading on a PE ratio of 10.8x, assuming you use a discount rate of 13.9%.

- Given the current share price of ₹204.18, the analyst price target of ₹194.21 is 5.1% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bandhan Bank?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.