Key Takeaways

- Overdependence on microfinance and limited geographic diversification expose Bandhan Bank to elevated credit and regional risks, undermining sustained profitability and stability.

- Intensifying digital competition and rising compliance costs are constraining Bandhan Bank's margin expansion, limiting its ability to match sector-leading returns.

- Accelerated secured loan mix, broadening geographic presence, expanding low-cost deposits, digital innovation, and regulatory tailwinds position the bank for improved stability and sustainable long-term profitability.

Catalysts

About Bandhan Bank- Engages in the provision of banking and financial services for personal and business customers in India.

- The rapid adoption of digital banking, payments, and fintech products in India is expected to accelerate, increasing competition from nimble digital-first lenders and neobanks; this could erode Bandhan Bank's customer acquisition momentum and fee-based income, thereby placing long-term pressure on revenue growth and operating profitability.

- Heightened regulatory focus on data privacy, consumer protection, and cybersecurity will likely drive sustained increases in compliance and technology costs; these rising expenses are poised to weigh on net margins and limit operational leverage, especially as Bandhan Bank transitions to a more tech-driven operating model.

- Bandhan Bank's historic and ongoing overexposure to the microfinance and low-income borrower segment, coupled with only gradual progress in diversifying away from these loans, leaves it structurally vulnerable to spikes in credit costs and loan delinquencies during macro or regional downturns, undermining any sustained earnings recovery.

- Despite attempts at geographic diversification, Bandhan Bank's concentrated presence in Eastern and North-Eastern India exposes it to heightened risks from region-specific economic, political, or climate-related shocks, which could lead to higher provisioning requirements, increased NPAs, and ongoing instability in earnings and balance sheet quality.

- The rising cost-to-income ratio driven by necessary investments in people, technology, and new branches, combined with only moderate improvement in efficiency over the next two years, signals limited room for margin expansion; this is likely to cap return on assets and return on equity well below sector leaders for the foreseeable future, resulting in structurally subdued profitability.

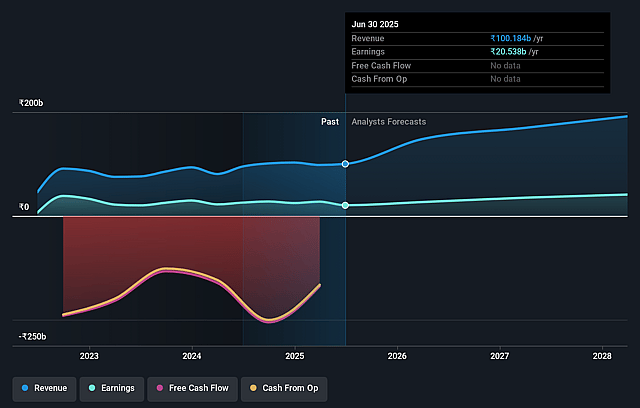

Bandhan Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Bandhan Bank compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Bandhan Bank's revenue will grow by 21.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 25.7% today to 17.3% in 3 years time.

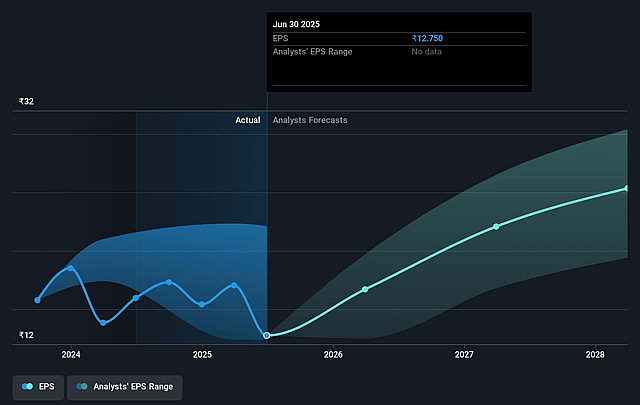

- The bearish analysts expect earnings to reach ₹33.1 billion (and earnings per share of ₹20.71) by about July 2028, up from ₹27.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.9x on those 2028 earnings, down from 10.8x today. This future PE is lower than the current PE for the IN Banks industry at 12.7x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.57%, as per the Simply Wall St company report.

Bandhan Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Bandhan Bank is actively diversifying its loan book with the secured loan mix rising to over 50%, robust growth in retail, housing, and wholesale banking assets, and ambitious plans to further increase secured advances to 55% or more by 2027, which can improve asset quality and reduce credit losses, positively impacting net margins and earnings stability in the medium to long term.

- The bank has made significant strides in geographical diversification, reducing dependence on the East and North-East from 53% of advances in FY22 to 39% in FY25 and expanding into the North, West, and South, which should lower regional risk concentration and support more stable revenue growth.

- Strong deposit franchise growth-with retail term deposits up 30% year-on-year and retail/CASA deposits now at 69% of total-improves funding stability, reduces cost of funds as rates fall, and enhances profitability by supporting sustainable advances growth and margin resilience.

- Continued investment in digital banking, operational streamlining, and technology modernization, as well as the rollout of new digital products and transaction platforms, are expected to deliver operational efficiencies, lower the cost-to-income ratio, and strengthen long-term profitability.

- Regulatory clarifications reducing risk weights on eligible MFI and secured loans, along with Bandhan Bank's solid capital adequacy ratio of 18.7%, provide ample headroom for future loan growth and business expansion, which could boost revenue, operating leverage, and potentially deliver higher returns on assets and equity over the strategic planning horizon.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Bandhan Bank is ₹134.53, which represents two standard deviations below the consensus price target of ₹185.68. This valuation is based on what can be assumed as the expectations of Bandhan Bank's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹225.0, and the most bearish reporting a price target of just ₹130.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹190.8 billion, earnings will come to ₹33.1 billion, and it would be trading on a PE ratio of 9.9x, assuming you use a discount rate of 14.6%.

- Given the current share price of ₹183.68, the bearish analyst price target of ₹134.53 is 36.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.