Last Update 28 Mar 26

CTY1S: Future Control Shift To Majority Owner Will Support Bullish Case

Analysts have reaffirmed their price target for Citycon Oyj at €3.80, with no change in underlying fair value, discount rate, revenue trajectory, profit margin assumptions or forward P/E expectations. This reflects a steady view on the shares based on current information.

What's in the News

- G City Ltd completed the acquisition of an additional 27.3% stake in Citycon Oyj for approximately €200 million on March 6, 2026, increasing its direct ownership to 66.6% of the company. This followed a mandatory tender offer priced at €4.00 per share and €0.38 per stock option 2025D, 2025E and 2025F (Key Developments).

- A mandatory tender offer process for Citycon shares has been running, with the offer period commencing on January 2, 2026 and currently scheduled to expire on March 6, 2026, following Swedish foreign direct investment approval on January 19, 2026 (Key Developments).

- The Board of Directors proposed, and the Extraordinary General Meeting on March 23, 2026 resolved, a distribution of €0.90 per share from the reserve of invested unrestricted equity as a return of capital, totaling approximately €165.21 million, with payment scheduled for April 1, 2026 to shareholders on record as of March 25, 2026 (Key Developments).

- Citycon provided earnings guidance for 2026, stating that like for like net rental income is expected to grow compared to the previous year (Key Developments).

- Citycon reported completion of a share buyback program announced on June 24, 2025, having repurchased 694,801 shares for €2.64 million, representing 0.38% of shares, with no shares repurchased between October 1 and December 31, 2025 (Key Developments).

Valuation Changes

- Fair Value: €3.80 per share, unchanged with no revision to the underlying estimate.

- Discount Rate: 11.32%, unchanged, indicating no adjustment to the risk or return assumptions used in the valuation model.

- Revenue Growth: 7.29% decline assumption maintained, with no change in the projected like for like revenue trend used in the analysis.

- Net Profit Margin: 23.14% assumption effectively unchanged, reflecting a stable view on expected profitability levels.

- Future P/E: 16.94x, unchanged, suggesting the same earnings multiple is being applied to Citycon Oyj's projected earnings.

Key Takeaways

- Resilient urban asset demand and improved tenant activity support higher occupancy, rental income, and potential revenue growth.

- Sustained cost efficiencies and proactive financial management enhance operating margins, stabilize asset values, and position the company for future growth.

- Reliance on asset sales, rising financial costs, volatile energy savings, and significant share collateralization expose Citycon to earnings, balance sheet, and share price risks.

Catalysts

About Citycon Oyj- A real estate investment company, owns and develops mixed-use centers in Finland, Norway, Sweden, Denmark, and Estonia.

- Strong like-for-like net rental income growth (5.2% overall, 7.6% in Finland and Estonia) and high occupancy (95%) reflect the resilience and demand for centrally located, necessity-based urban assets, positioning Citycon to benefit from ongoing urban migration and population growth-likely supporting future revenue growth.

- Continued improvement in tenant sales and footfall, along with the ability to achieve positive leasing spreads and rent increases with new tenants, indicates growing consumer demand for mixed-use and experiential retail environments, which should lead to higher occupancy and rental income, positively impacting revenue and operating margins.

- Successful execution of cost-saving initiatives, particularly in Finland and Estonia, has led to record NOI margins demonstrated as sustainable, suggesting ongoing operating efficiency and margin improvement, which supports future net margins and earnings stability.

- Asset values are stabilizing with a recent fair value gain of €33.5 million, driven by improved cash flows in key properties and external appraisers' more optimistic view on growth prospects, especially in Sweden; this aligns with growing institutional investor interest in resilient, transit-oriented real assets, potentially supporting higher portfolio valuations and return on equity.

- Proactive balance sheet management, including substantial debt repayment, refinancing at attractive terms, and a highly flexible unencumbered asset base, positions Citycon to better manage its cost of capital and pursue redevelopment or green initiatives-likely to reduce interest expenses and enhance earnings growth over the medium term.

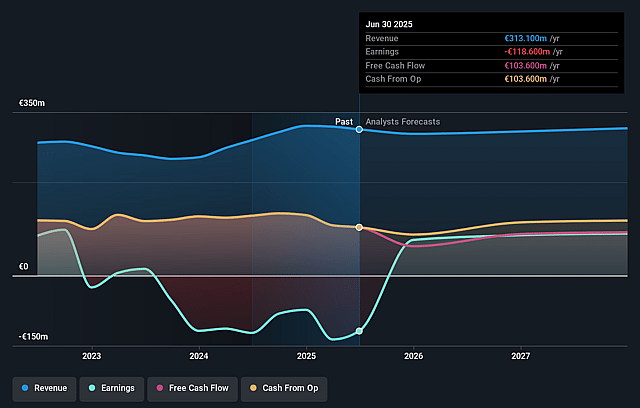

Citycon Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Citycon Oyj's revenue will decrease by 7.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 17.6% today to 23.1% in 3 years time.

- Analysts expect earnings to reach €56.0 million (and earnings per share of €0.83) by about March 2029, up from €53.3 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.0x on those 2029 earnings, up from 10.7x today. This future PE is greater than the current PE for the GB Real Estate industry at 13.4x.

- Analysts expect the number of shares outstanding to decline by 0.36% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Citycon's reported net rental income for the quarter was €1.4 million below the previous year, and EPRA earnings fell by €7.8 million year-over-year, largely due to asset disposals-signaling pressure on revenue base and future earnings if replacement of disposed income streams lags or proceeds from divestments are inadequate.

- Increased financial costs following the issuance of a €400 million green bond and refinancing at higher interest rates have compressed net earnings, and ongoing inflation or further rate hikes could continue to erode margins and limit retained earnings growth.

- The company's bottom line was supported by significant cost savings, particularly in energy and operational expenses-however, management acknowledges that fluctuations in energy prices may reverse some of these gains, introducing volatility to operating margins and net income.

- The strategy of asset sales remains critical for balance sheet derisking, but recent failed disposals (e.g., a buyer walking away last-minute) highlight execution risks; further dependence on asset sales at potentially unfavorable prices could depress book value and long-term revenue streams.

- A substantial portion of the company's shares is pledged by its main shareholder as collateral (about 30% of all Citycon shares), raising concerns about forced selling risk in adverse scenarios, which could pressurize share price and increase volatility for remaining shareholders.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €3.8 for Citycon Oyj based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €242.0 million, earnings will come to €56.0 million, and it would be trading on a PE ratio of 17.0x, assuming you use a discount rate of 11.3%.

- Given the current share price of €3.11, the analyst price target of €3.8 is 18.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Citycon Oyj?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.