Last Update 17 Jun 26

SCHN: Refined Discount Rate And Profitability Assumptions Will Support Gradual Bullish Repricing

Schindler Holding's analyst price target has been raised by CHF 3, as analysts cite recent target revisions and a fresh upgrade that reflect updated assumptions around discount rates, profitability and P/E expectations.

Analyst Commentary

Recent research on Schindler Holding highlights a mix of optimism and caution as analysts revisit their assumptions on discount rates, profitability and P/E multiples, with one major bank moving to an upgrade and another lifting its price target.

Bullish Takeaways

- Bullish analysts point to refreshed assumptions on profitability as support for a higher valuation framework for Schindler Holding, reflected in the recent CHF 3 price target adjustment.

- The recent upgrade by Goldman Sachs signals increased confidence in Schindler Holding's ability to execute on its current plan, which some analysts see as better aligned with their return expectations.

- Revisions to discount rate assumptions are viewed by bullish analysts as better capturing the risk profile of Schindler Holding, which, in their view, helps justify current P/E expectations.

- Supportive research argues that the updated targets bring published valuations more in line with how bullish analysts already viewed Schindler Holding's earnings power and cash generation potential.

Bearish Takeaways

- Bearish analysts remain cautious that the higher price targets could leave limited room for error if Schindler Holding falls short on profitability assumptions embedded in these models.

- Some caution that the revised P/E expectations rely on execution staying on track, and that any delays or setbacks could challenge the recent target moves.

- There is concern among more cautious analysts that changes to discount rate inputs may understate potential risks, which could make current valuations for Schindler Holding appear demanding.

- A few bearish analysts view the cluster of recent positive revisions as increasing the bar for future performance, which could raise the risk of disappointment if subsequent research turns more neutral.

What’s in the News for Schindler Holding

- Schindler Holding scheduled an Analyst/Investor Day, giving analysts and investors a platform to hear updated management views and ask questions about the company’s priorities. (Source: Key Developments)

- The Schindler Holding AG Analyst/Investor Day event is flagged as a key development, indicating that recent analyst discussions and model updates are being informed by direct engagement with management. (Source: Key Developments)

- The timing of the Schindler Holding Analyst/Investor Day is influencing how some research houses frame their discount rate, profitability and P/E assumptions, linking recent rating and target changes to the insights shared around this event. (Source: Key Developments)

Valuation Changes for Schindler Holding

- Fair Value: Modelled fair value remains unchanged at CHF 304.08, with the latest update keeping the previous estimate intact.

- Discount Rate: The discount rate has fallen slightly from 5.20% to 5.09%. This indicates a modest adjustment to the risk input used in the valuation work on Schindler Holding.

- Revenue Growth: The revenue growth assumption is effectively unchanged and remains close to 4.06% in the refreshed model.

- Net Profit Margin: The net profit margin has edged down marginally from 10.42% to 10.39%. This is a very small move in the earnings profile used in the analysis.

- Future P/E: The future P/E multiple has dipped slightly from 38.23x to 38.21x. This reflects a minimal change in how Schindler Holding's earnings are being capitalised.

Key Takeaways

- Strong growth in Modernization and Service, especially in China and Asia-Pacific, supports higher-margin, recurring revenues amid global sustainability and urbanization trends.

- Operational streamlining and digital innovation enhance profitability and position the company for stable earnings despite short-term installation market challenges.

- Exposure to low-growth, price-competitive regions and external cost pressures threaten sustainable margin improvement, limiting long-term revenue expansion and earnings quality.

Catalysts

About Schindler Holding- Engages in the production, installation, maintenance, and modernization of elevators, escalators, and moving walks worldwide.

- The rapid acceleration in Schindler's Modernization business-showing double-digit growth globally and particularly robust order momentum in China (supported by government programs to upgrade aging elevators)-positions the company to capitalize on global modernization and sustainability trends, driving recurring, higher-margin revenue growth.

- Expansion and strength in Service (mid-single-digit growth and portfolio expansion, especially in fast-growing regions like Asia-Pacific and China) supports revenue stability and margin improvement, leveraging rising demand for accessible mobility and ongoing urbanization.

- Operational efficiency initiatives, including significant structural streamlining (particularly in China), procurement savings, and SG&A reduction, are beginning to deliver visible improvements in operating margins, setting the stage for sustained net margin expansion even as topline growth moderates.

- Growing backlog, especially in Modernization and Service, combined with building order momentum outside of China, underpins future revenue increase and earnings visibility despite near-term new installation weakness in China.

- Strategic development of new product offerings (e.g., U.S. mid-rise elevators) and investment in digital services are expected to bolster differentiated revenue streams and enhance long-term profitability, supporting higher long-term returns as industry demand for smart, sustainable solutions rises.

Schindler Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

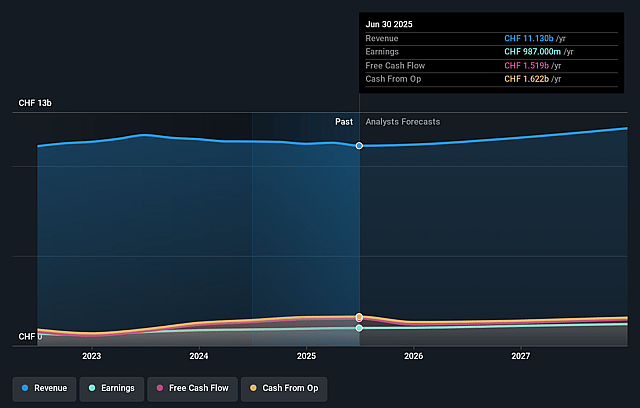

- Analysts are assuming Schindler Holding's revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.4% today to 10.4% in 3 years time.

- Analysts expect earnings to reach CHF 1.3 billion (and earnings per share of CHF 11.86) by about June 2029, up from CHF 1.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CHF1.0 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.3x on those 2029 earnings, up from 27.0x today. This future PE is greater than the current PE for the GB Machinery industry at 24.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.09%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged contraction in China's New Installation (NI) market, with multi-year double-digit declines in residential floor space starts, is leading to a smaller installed base; this reduces future Service and Modernization growth potential, directly limiting long-term revenue expansion.

- Company restructuring and ongoing efficiency initiatives, especially in China, reflect the risk of sustained margin pressure from low-margin orders, negative scale effects, and challenging market dynamics, which could compress group net margins and EBIT growth in future years.

- Persistent Swiss franc strength is generating significant currency headwinds, consistently eroding order intake and revenue reported in Swiss francs, creating long-term pressure on top-line growth and earnings for the group.

- Heightened global tariffs, particularly those impacting input materials like copper and specific markets post-August, introduce structural cost risks and customer project viability challenges that may not be fully mitigated by pricing or supply chain adaptation, weighing on future group profitability.

- Modernization and New Installation segments in China currently deliver margins below group average, and sectoral overexposure to low-growth, price-competitive regions (e.g., Western Europe, China) could prolong a reliance on lower-profit business lines, impeding sustainable net margin improvement and potentially undermining long-term earnings quality.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF304.08 for Schindler Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF345.0, and the most bearish reporting a price target of just CHF275.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CHF12.2 billion, earnings will come to CHF1.3 billion, and it would be trading on a PE ratio of 38.3x, assuming you use a discount rate of 5.1%.

- Given the current share price of CHF257.5, the analyst price target of CHF304.08 is 15.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Schindler Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.