Last Update 18 Jun 26

KOPN: FPV Drone Programs And Defense Backlog Will Drive Stock Upside

Analysts have lifted the average Kopin price target into the mid single digits, with recent moves such as Craig-Hallum's increase to $10 from $6 and other boosts into the $6 to $7 range, largely tied to positive views on the FPV drone opportunity and management's reiterated $56 million revenue outlook for FY26.

Analyst Commentary

Recent Street research on Kopin centers on how the FPV drone opportunity, the Sentinel FPV headset rollout, and management's reiterated FY26 revenue outlook of $56 million might affect the stock's risk and reward profile. Price targets have been adjusted across several firms, and the commentary around those changes highlights both upside potential and execution questions that investors should weigh.

Bullish Takeaways

- Bullish analysts are tying higher price targets in the US$6 to US$10 range to Kopin's reiterated FY26 revenue outlook of $56 million, viewing that guidance as an anchor for their growth assumptions and valuation work.

- The FPV drone market is a key focus, with particular attention on the Sentinel FPV complete headset solution, which bullish analysts see as a way for Kopin to better monetize its technology and support revenue visibility.

- Several reports describe Kopin's recent quarterly results as "solid" and point to a growing project pipeline, which they argue could support longer term revenue expansion and justify higher valuation multiples if execution stays on track.

- Some bullish commentary highlights the proposed U.S. congressional drone budget and the potential for up to three million units in the 2027 to 2028 timeframe, viewing this as a very large addressable opportunity that could be material to Kopin's future growth trajectory if the company captures a meaningful share.

Bearish Takeaways

- While targets have moved higher, the wide range from mid single digits to US$10 reflects uncertainty around how much of the FPV drone opportunity Kopin can realistically capture, which could limit upside if adoption or contracts fall short of expectations.

- The reiterated FY26 revenue outlook of $56 million is central to many models, so any execution slip on product delivery, defense or drone program timing, or customer orders could pressure both Kopin's valuation framework and future target revisions.

- Analysts' focus on proposed U.S. drone budgets underscores a dependency on government spending and program follow through, which may add policy and timing risk to Kopin's growth story and make the stock more sensitive to changes in defense priorities.

- The emphasis on the FPV segment and Sentinel solution suggests a relatively concentrated thesis, so setbacks in this product area or increased competition in FPV headsets could weigh on Kopin's growth outlook and compress the multiples implied by current targets.

What’s in the News for Kopin

- Kopin reported a Q4 2025 revenue decline tied to procurement delays from a government shutdown, while entering 2026 with an approximately US$37 million defense backlog and US$56 million of new funding from strategic and institutional investors, according to recent earnings coverage.

- The company filed an SEC registration statement effective May 29, 2026 that confirms a US$21.5 million follow on defense production contract for U.S. made thermal imaging assemblies and describes the build out of a full scale OLED microdisplay manufacturing facility in the U.S. to support domestic defense demand. Source: SEC filing summary.

- Theon International Plc converted all 1,000 shares of Kopin’s Series A Convertible Preferred Stock into common stock on May 28, 2026, retiring that preferred class and increasing Theon’s equity exposure after its earlier US$15 million investment and European joint development agreements. Source: company announcement.

- Kopin announced a US$3.2 million initial order for an optical module for a partner’s next generation FPV goggle system, tied to a program that contemplates up to 40,000 goggles by the end of 2028 and leveraging the Sentinel FPV module for tactical drone applications. Source: company press release.

- The company disclosed that it would be unable to file its next 10 K by the SEC deadline, highlighting a filing delay that investors may want to monitor. Source: company SEC filing notice.

Valuation Changes for Kopin Stock

- Fair Value: Model fair value for Kopin is unchanged at $7.63 per share, indicating no shift in the central valuation estimate.

- Discount Rate: The discount rate has risen slightly from 10.96% to 11.10%, which modestly increases the hurdle rate applied to Kopin's future cash flows.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged at 38.02%, suggesting no material adjustment to the sales outlook built into the model.

- Net Profit Margin: The projected net profit margin has eased slightly from 17.21% to 16.88%, reflecting a minor reduction in expected profitability levels for Kopin.

- Future P/E: The implied future P/E multiple has risen slightly from 125.85x to 128.78x, pointing to a marginally higher valuation multiple applied to Kopin's forward earnings in the model.

Key Takeaways

- Strategic partnership and investments expand access to global defense markets, driving revenue growth and improving earnings reliability.

- Advanced manufacturing, automation, and display innovation boost efficiency, lower costs, and increase margins while strengthening technology leadership and market opportunities.

- Ongoing losses, reliance on volatile government funding, unproven cost-saving efforts, nonexclusive partnerships, and rapid tech shifts threaten Kopin's profitability, margins, and future relevance.

Catalysts

About Kopin- Develops, manufactures, and sells microdisplays, subassemblies, and related components for defense, enterprise, industrial, and consumer products in the United States, the Asia-Pacific, Europe, and internationally.

- The strategic partnership and $15 million investment from Theon International positions Kopin to broaden its reach into key defense markets in Europe, Southeast Asia, and NATO allied countries, allowing access to increased defense budgets and long-term military modernization programs; this is expected to drive significant revenue growth and improved earnings visibility.

- Application-specific solutions (such as DayVAS and DarkWAVE), developed in collaboration with Theon, and increased manufacturing utilization at the Dalgety Bay facility are likely to boost production efficiency and capacity absorption, thereby increasing gross margins and reducing operating costs.

- Acceleration in automation and optical inspection within Kopin's manufacturing line is set to yield material operating expense reductions by late 2025 and into 2026, raising profitability and net margins as volume scales.

- Major secular increases in global defense spending and a $22 billion+ pipeline of U.S. military technology upgrades (such as the SBMC/IVAS program), for which Kopin's microdisplays are integral, support a robust outlook for future contract wins, enhancing long-term revenue stability and growth.

- Ongoing innovation in OLED, MicroLED, and custom neural display hardware for AR, VR, and next-gen soldier vision systems strengthens Kopin's technology leadership, leading to new market opportunities and premium product mix, with the potential to improve both top-line revenue and gross profitability over time.

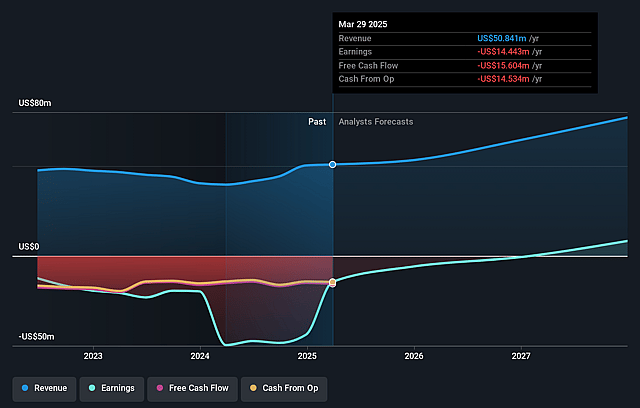

Kopin Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Kopin's revenue will grow by 38.0% annually over the next 3 years.

- Analysts are not forecasting that Kopin will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Kopin's profit margin will increase from 4.9% to the average US Semiconductor industry of 16.9% in 3 years.

- If Kopin's profit margin were to converge on the industry average, you could expect earnings to reach $17.5 million (and earnings per share of $0.08) by about June 2029, up from $1.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 129.4x on those 2029 earnings, down from 443.3x today. This future PE is greater than the current PE for the US Semiconductor industry at 68.3x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.1%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent net losses (Q2 2025 net loss of $5.2 million on $8.5 million in revenue), high operating expenses, and negative cash flow ($7.6 million used in operating activities in H1 2025) raise concerns about long-term profitability and may require future capital raises, potentially diluting shareholders and impacting earnings per share.

- The company's significant reliance on government and defense sector funding exposes Kopin to budgeting delays and volatility, as seen in Q2 when government uncertainty led to a "sales vacuum"; continued dependency could destabilize revenue streams and limit margin visibility in the long term.

- Although new partnerships like Theon present opportunities, the manufacturing automation and cost-saving initiatives are not yet fully operational or proven, and delays or underperformance in these could keep gross margins low (94% cost of product revenues in Q2 2025), directly affecting net margins and profitability.

- Theon's supply agreements are nonexclusive and Kopin's competitors also have OLED supply deals with them; this lack of exclusivity risks limited market share gains, raises the threat of pricing competition, and could constrain Kopin's revenue growth and margin improvement if competitors outpace on technology or price.

- Market and technology trends suggest rapid evolution in display technologies (e.g., OLED, MicroLED, LCD), with the risk that if Kopin cannot match or surpass competitors in innovation, quality, and scalability, its core products may lose relevance and its long-term revenues and earnings potential could diminish.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $7.62 for Kopin based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $6.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $103.4 million, earnings will come to $17.5 million, and it would be trading on a PE ratio of 129.4x, assuming you use a discount rate of 11.1%.

- Given the current share price of $4.86, the analyst price target of $7.62 is 36.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kopin?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.