Last Update 07 Jul 26

Fair value Increased 2.48%A017670: AI Data Center Buildout Will Support Future Upside Despite Dividend Halt

Analysts have modestly lifted their fair value estimate for SK Telecom, raising the implied price target from ₩93,740 to ₩96,062.50, citing updated assumptions for profit margins and future P/E while keeping the discount rate broadly unchanged.

What’s in the News for SK Telecom

- SK Telecom plans to pursue construction of AI data centers with total capacity of 15GW, including the Ulsan AI Data Center, aiming to open 5GW of domestic capacity in stages starting in 2029 as part of Korea’s "AI G3" ambitions and regional development efforts. (Source: company disclosure)

- The company is reviewing funding options for the 15GW AI data center buildout, including strategic partner investment from global technology and overseas investors, long-term customer contracts, and project financing, with final investment amounts and timing yet to be determined. (Source: company disclosure)

- SK Telecom and NVIDIA, together with other SK Group affiliates, are expanding their alliance to include joint research on next generation AI factory architectures, focusing on full stack optimization across accelerated computing, memory, and data center operations. (Source: company disclosure)

- SK Telecom, Arm, and Rebellions are collaborating to develop AI servers that combine Arm AGI CPUs with Rebellions’ RebelCard accelerators, with systems to be validated in SK Telecom’s AI data center environment and potential use for SK Telecom’s A.X K1 foundation model. (Source: company disclosure)

- SK Telecom has joined Huawei, LG Electronics, Nokia, BlackBerry, and JVCKENWOOD in making patents available for license through Sisvel’s point of sale cellular connectivity program covering 2G, 3G, 4G, and 5G technologies. (Source: Sisvel program announcement)

Valuation Changes for SK Telecom

- Fair Value: The estimated fair value for SK Telecom has been revised from ₩93,740 to ₩96,062.50, indicating a modest upward adjustment in the valuation model.

- Discount Rate: The discount rate assumption is essentially unchanged at 7.036%, suggesting a consistent view of SK Telecom’s risk profile in the model.

- Revenue Growth: The long term revenue growth assumption has shifted slightly from 2.86% to 2.79%, reflecting a more cautious stance on top line expansion in ₩ terms.

- Profit Margin: The profit margin assumption has moved from 7.65% to 7.67%, a minor upward revision in expected earnings strength for SK Telecom.

- Future P/E: The future P/E multiple used in the valuation has been raised from 17.17x to 17.67x, implying a slightly higher assumed earnings multiple for SK Telecom in the forecast period.

Key Takeaways

- Growth in AI, cloud, and data demand positions SK Telecom for expanded margins and new revenue streams through premium services and advanced connectivity infrastructure.

- Strategic partnerships, regulatory support, and emphasis on cybersecurity enable stronger brand reputation, B2B diversification, and more stable revenue amid evolving digital trends.

- Persistent customer churn, costly cybersecurity fallout, and competitive pricing pressures threaten recovery of margins, even as risky AI and data center investments aim to offset legacy business declines.

Catalysts

About SK Telecom- Engages in the provision of wireless telecommunication services in South Korea.

- The rapid proliferation of AI and data-driven applications is driving robust demand for hyperscale data centers and advanced connectivity infrastructure, positioning SK Telecom to benefit from long-term secular growth in AI computing and cloud adoption as evidenced by rising AI/data center revenue and the upcoming Ulsan AI Data Center-potentially boosting revenue and expanding operating margins over time.

- Increased adoption of digital consumption, remote work, and streaming is fueling sustained growth in data demand, which enables SK Telecom to sustain and ultimately grow ARPU through premium 5G offerings and network upgrades-supporting top-line growth and margin recovery as the subscriber base stabilizes post-incident.

- Strategic investments and partnerships, such as collaboration with AWS on AI data infrastructure and SK Telecom's involvement in sovereign AI projects, are expected to unlock new high-margin B2B and enterprise opportunities, accelerating revenue diversification and supporting long-term earnings expansion.

- Execution of the Information Protection Innovation Plan-including significant investment in cybersecurity and customer assurance programs-is set to restore customer trust and strengthen brand reputation, aiding in subscriber recovery and stabilizing revenue streams by minimizing future churn risk.

- Regulatory tailwinds-including strong government backing for AI and digital infrastructure in South Korea-should facilitate capital investment, enhance competitive positioning, and provide a more supportive environment for long-term revenue and EPS growth in SK Telecom's core and emerging businesses.

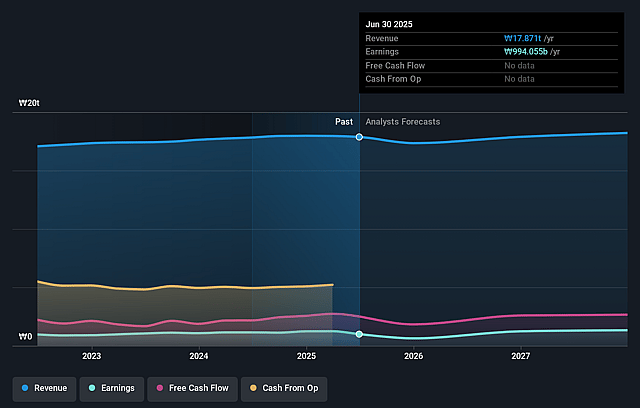

SK Telecom Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming SK Telecom's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.0% today to 7.7% in 3 years time.

- Analysts expect earnings to reach ₩1419.9 billion (and earnings per share of ₩6515.79) by about July 2029, up from ₩346.6 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₩2037.2 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.7x on those 2029 earnings, down from 52.7x today. This future PE is lower than the current PE for the GB Wireless Telecom industry at 31.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.04%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The significant cybersecurity incident has led to subscriber losses, lower revenues, and higher one-off costs, and there is a risk that ongoing investments in information protection and customer incentives (e.g., heavy tariff discounts, compensation programs, USIM replacements) could create a prolonged drag on net margins and earnings if customer trust and the subscriber base are slow to recover.

- The large-scale investment into information protection (₩700 billion over five years) and substantial new AI/data center CapEx, alongside only partial offset from new AI business revenues, could strain free cash flow and challenge the company's ability to maintain both high dividend payouts and margin expansion, directly impacting net income and shareholder returns.

- The notable net loss of MNO subscribers (handset subscriber base shrinking by 750,000) and declining 5G, broadband, and IPTV users following the incident highlight the risk that sustained customer churn and slow market share recovery could depress long-term core telecom revenues and ARPU, particularly in a highly saturated and competitive South Korean market.

- Continuing dependence on customer-facing promotions (e.g., heavy discounts, restored membership benefits, newly allowed handset subsidies) to win back users may pressure operating margins, especially if competitive responses from other telcos or the abolition of the handset subsidy law trigger additional industry-wide price competition, impairing profitability.

- While the AI and data center businesses promise growth, there is execution risk: delays, underperformance, or failure to scale these new revenue streams could leave SK Telecom exposed to a structural decline in high-margin legacy businesses and regulatory challenges, with slow replacement of lost earnings from telecom operations.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₩96062.5 for SK Telecom based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₩150000.0, and the most bearish reporting a price target of just ₩55000.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₩18503.4 billion, earnings will come to ₩1419.9 billion, and it would be trading on a PE ratio of 17.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of ₩85700.0, the analyst price target of ₩96062.5 is 10.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on SK Telecom?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.