Last Update 06 Jul 26

Fair value Increased 6.21%2899: Index Inclusions And Buybacks Will Support Further Rerating

Analysts have lifted their price target for Zijin Mining Group to HK$53.71 from HK$50.57, reflecting updated assumptions around fair value, discount rate, revenue growth, profit margin and future P/E estimates.

What’s in the News for Zijin Mining Group

- A board meeting is scheduled for August 21, 2026 to review and approve Zijin Mining Group’s 2026 interim results for the six months ended June 30, 2026, and to consider an interim dividend payment, if any (source: company board agenda).

- Zijin Mining Group has been added as a constituent to the S&P International 700 index (source: index announcement).

- Zijin Mining Group has been added as a constituent to the S&P Global 1200 index (source: index announcement).

- Between April 1 and April 14, 2026, Zijin Mining Group repurchased 24,444,500 shares for CNY 817.98m, bringing total buybacks under the March 20, 2026, program to 77,474,592 shares for CNY 2,499.75m, representing 0.29% of shares (source: company buyback update).

Valuation Changes

- Fair Value: HK$53.71 compared with the previous HK$50.57, indicating a slightly higher assessed level for Zijin Mining Group.

- Discount Rate: now 9.53% versus 9.41% previously, reflecting a small upward adjustment in the rate used to discount future cash flows.

- Revenue Growth: assumption held effectively unchanged at about 15.10% CN¥, with only a minor numerical adjustment from the prior 15.10%.

- Net Profit Margin: assumption remains effectively stable at about 18.69% CN¥, with only a very small numerical change.

- Future P/E: now 15.52x compared with the previous 14.53x, indicating a modestly higher valuation multiple being applied to Zijin Mining Group’s forward earnings.

Key Takeaways

- Strategic focus on cost control, AI, and M&A activities aims to improve efficiency, expand resource base, and boost long-term revenue and profitability.

- Emphasis on sustainability initiatives and clean energy positions Zijin for favorable market perception and potential regulatory benefits.

- Rising geopolitical risks, increased costs, and uncertain market conditions could pressure Zijin Mining's margins and profitability despite ambitious expansion and investment strategies.

Catalysts

About Zijin Mining Group- A mining company, engages in the exploration, mining, processing, refining, and sale of gold, non-ferrous metals, and other mineral resources in Mainland China and internationally.

- The company is accelerating the construction of incremental copper, gold, and lithium projects, including Phase 2 expansion for Julong Copper and debuting new projects like the lithium extraction, which is expected to enhance output and contribute to revenue growth.

- Zijin Mining is strategically focusing on cost control measures, particularly in overseas mines, which could potentially improve net margins and enhance profitability despite challenges such as degrading ore grades.

- The company is committed to leveraging AI and improving its global operations management, which could drive efficiency and optimize earnings by reducing operational costs and enhancing output quality.

- Zijin's robust pipeline of M&A activity, including potential acquisitions and strategic investments, aims to expand its resource base and output capacity, likely boosting long-term revenue and earnings growth.

- Their focus on sustainability and ESG improvements, alongside advances in low-carbon and clean energy development, positions Zijin for favorable market perception and potential regulatory advantages, supporting stable financial performance and future profitability.

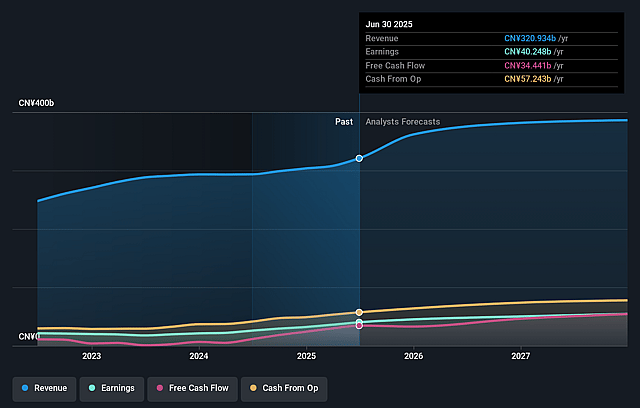

Zijin Mining Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Zijin Mining Group's revenue will grow by 15.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 16.7% today to 18.7% in 3 years time.

- Analysts expect earnings to reach CN¥105.0 billion (and earnings per share of CN¥3.53) by about July 2029, up from CN¥61.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CN¥134.7 billion in earnings, and the most bearish expecting CN¥74.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.5x on those 2029 earnings, up from 12.1x today. This future PE is greater than the current PE for the HK Metals and Mining industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.53%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Geopolitical factors and resource nationalism are rising, leading to increased overseas risks, which could negatively impact earnings and profits from international operations.

- Degrading ore grades and increasing costs in areas like transportation, labor, and depreciation could pressure Zijin's ability to maintain its margins.

- Uncertainty in the lithium market, with declining demand and prices, could hinder revenue growth and the profitability of Zijin's new projects.

- The company’s expansion strategy involves significant investments and M&A activities, which carry financial risks that could affect net margins if the ventures do not perform as expected.

- The emphasis on large-scale, long-term projects like the Julong Copper mine may tie up capital and resources, potentially impacting short-term earnings and financial flexibility.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of HK$53.71 for Zijin Mining Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$61.78, and the most bearish reporting a price target of just HK$46.34.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CN¥562.1 billion, earnings will come to CN¥105.0 billion, and it would be trading on a PE ratio of 15.5x, assuming you use a discount rate of 9.5%.

- Given the current share price of HK$31.2, the analyst price target of HK$53.71 is 41.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Zijin Mining Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.