Catalysts

About Taylor Morrison Home

Taylor Morrison Home is a U.S. homebuilder focused on entry-level, move up, resort lifestyle and single family rental communities.

What are the underlying business or industry changes driving this perspective?

- Planned openings of well over 100 new communities in 2026 and mid to high single digit outlet growth, combined with faster cycle times that are roughly 90 days shorter than two years ago, give the company more capacity to convert buyer interest into home closings, which directly supports revenue and earnings.

- A portfolio that is approximately 70% move up and resort lifestyle buyers, plus a Premier Esplanade brand that serves an affluent customer base and is described as relatively insulated from interest rate concerns, can support pricing power and mix, which is important for gross margins and net income.

- A growing off balance sheet and asset lighter lot position, with 60% of lots controlled through options and other structures and a goal of at least 65%, along with a $3b Yardly financing vehicle, is intended to keep capital needs lower and improve returns on equity and long term earnings efficiency.

- Negotiated improvements on roughly 3,400 lots, including an average 8% land price reduction, development cost relief of about 5% to 6% and increased access to finished lots, aim to keep future land spend more efficient and can provide support for future gross margins and cash flow.

- Expanded use of tech enabled sales tools, including an AI powered digital assistant, strong financial services capture at 88% and a reservation system that has reduced co broker participation by several hundred basis points, are all intended to lower selling costs and support SG&A leverage and overall profitability.

Assumptions

This narrative explores a more optimistic perspective on Taylor Morrison Home compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

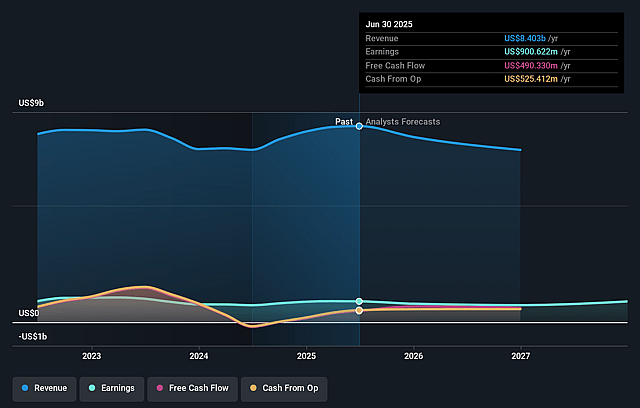

- The bullish analysts are assuming Taylor Morrison Home's revenue will decrease by 5.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 10.2% today to 10.6% in 3 years time.

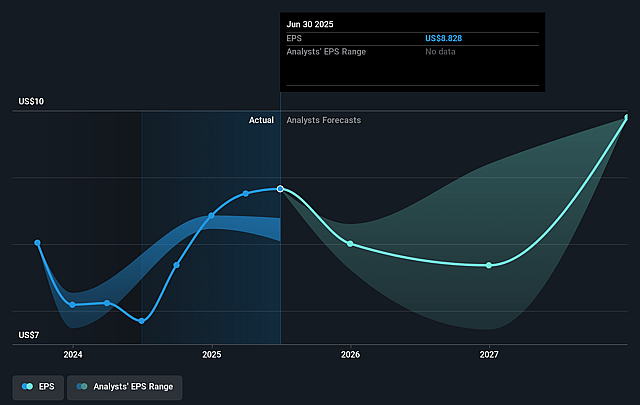

- The bullish analysts expect earnings to reach $757.1 million (and earnings per share of $8.46) by about January 2029, down from $850.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 14.2x on those 2029 earnings, up from 7.5x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.7x.

- The bullish analysts expect the number of shares outstanding to decline by 3.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Buyer confidence across all segments is described as sensitive to macroeconomic and political uncertainty, and management repeatedly links move up and resort lifestyle demand to improved confidence. A prolonged period of weak sentiment could keep monthly absorption paces below the long term target and weigh on revenue and earnings.

- The company is leaning heavily on incentives, including mortgage rate buydowns, adjustable products and closing cost support, to move a high mix of spec homes. Management points out that the most expensive incentives are tied to entry level buyers, which could pressure homebuilding gross margins and limit any improvement in net margins if this incentive intensity persists.

- The current reliance on spec inventory, with specs accounting for 72% of quarterly sales and 61% of closings and an expectation that spec penetration will increase, leaves Taylor Morrison exposed if demand weakens in key markets such as Texas or Florida. This could lead to higher cancellations, slower inventory turns and softer revenue and earnings.

- Long term growth plans depend on an asset lighter land strategy and off balance sheet structures like the US$3b Yardly facility. However, higher net interest expense already tied to land banking and the need to continually renegotiate or walk away from land deals could constrain returns on equity and limit future improvement in net margins and earnings.

- The portfolio is concentrated in markets that have seen strong migration and significant building activity, including Florida, Texas, Arizona and parts of California. Management highlights issues such as hypercompetitive low price points in Dallas, affordability constraints for first time buyers and tech related softness in the Bay Area, all of which could cap pricing power and pressure both revenue and gross margins if supply stays elevated or demand cools.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Taylor Morrison Home is $94.54, which represents up to two standard deviations above the consensus price target of $75.0. This valuation is based on what can be assumed as the expectations of Taylor Morrison Home's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $95.0, and the most bearish reporting a price target of just $62.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $7.1 billion, earnings will come to $757.1 million, and it would be trading on a PE ratio of 14.2x, assuming you use a discount rate of 9.4%.

- Given the current share price of $65.35, the analyst price target of $94.54 is 30.9% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Taylor Morrison Home?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.