Last Update 02 Jul 26

Fair value Increased 8.38%AKSO: Dividends And Energy Transition Contracts Will Frame Mixed Research Outcomes

The analyst fair value estimate for Aker Solutions has been adjusted from NOK 41.11 to NOK 44.56, reflecting recent shifts in Street price targets between NOK 44 and NOK 48 and updated assumptions on discount rates, revenue trends, profit margins, and future P/E levels.

Analyst Commentary

Recent Street research on Aker Solutions has sent mixed signals, with some bullish analysts lifting price targets and others turning more cautious or cutting ratings. This blend of views feeds directly into how investors might think about the stock's valuation, execution risks, and growth profile around the new fair value estimate.

Bullish Takeaways

- Bullish analysts have highlighted enough positives to support price targets as high as NOK 48, which sits above the updated fair value estimate and suggests confidence in Aker Solutions' earnings power and project pipeline assumptions.

- The raise in one major firm's target from NOK 42 to NOK 48 points to a reassessment of revenue and margin assumptions that is supportive of a higher P/E multiple than previously applied.

- JPMorgan's earlier decision to raise its price target by NOK 14 indicates that, at least at that point in time, there was a more constructive view on execution and cash flow visibility versus prior expectations.

- The presence of multiple price targets clustered in the mid to high NOK 40s provides an anchor range that can help investors frame upside scenarios around Aker Solutions if the company meets or exceeds current operational assumptions.

Bearish Takeaways

- Several bearish analysts have shifted to more cautious ratings, which points to concerns around execution risks, order quality, or the sustainability of margins that could limit how much of the Street's target range is realized in practice.

- Recent downgrades signal that some on the Street see risk that current assumptions on growth or profitability may be demanding, which in turn can cap the P/E level investors are willing to pay for Aker Solutions.

- The move by JPMorgan to trim its price target from NOK 45 to NOK 44, while modest, underlines that even major houses are fine tuning expectations rather than uniformly moving higher, reflecting a more balanced risk reward profile.

- With multiple firms moving to more bearish stances in a short time window, the dispersion in views has widened, which can add pressure if Aker Solutions underperforms current expectations on revenue, margins, or project delivery.

What’s in the News for Aker Solutions

- Aker Solutions has been awarded a substantial contract, defined by the company as between NOK 2,500 million and NOK 4,000 million, to deliver an HVDC substructure for a European offshore wind project. The order intake is planned for the second quarter of 2026 in the Renewables and Field Development segment (source: client announcement).

- The company secured a sizeable contract, defined as between NOK 500 million and NOK 1,500 million, with Tussa Energi to supply all electromechanical equipment for the Tussa II hydropower plant in western Norway. Delivery is scheduled for completion in 2030, with order intake expected in the second quarter of 2026 (sources: recent news, client announcement).

- Aker Solutions signed a sizeable five year agreement with Cenovus Energy for engineering and maintenance services on White Rose field assets, including the West White Rose platform and the SeaRose FPSO. The contract will be booked as order intake in the second quarter of 2026 in the Life Cycle segment (source: client announcement).

- Aker Solutions' Entr business received CAD 1.2 million in funding from the Government of Canada to study offshore carbon transport and storage solutions for eastern Canada under the federal Energy Innovation Program (source: regulatory announcement).

- At the April 16, 2026 AGM, Aker Solutions approved an ordinary dividend of NOK 3.60 per share and an extraordinary dividend of NOK 5.00 per share, both payable to shareholders of record on that date. The shares traded ex dividend from April 17, with payment scheduled for April 27, 2026 (source: AGM announcements).

Valuation Changes for Aker Solutions

- Fair Value: Updated from NOK 41.11 to NOK 44.56, a modest uplift that reflects the latest set of assumptions in the model for Aker Solutions.

- Discount Rate: Adjusted slightly lower from 6.99% to 6.86%, which increases the present value placed on future cash flows in the valuation framework.

- Revenue Growth: The assumed near term revenue trend has been revised to a slightly smaller decline, from a fall of 18.25% to a fall of 17.76%.

- Net Profit Margin: The margin assumption has been fine tuned from 3.93% to 3.69%, implying a slightly more cautious view on profitability per NOK of revenue.

- Future P/E: The applied forward P/E multiple has moved from 19.0x to 21.2x, indicating a higher valuation being placed on Aker Solutions' expected earnings stream in the updated model.

Key Takeaways

- High order intake in offshore wind and CCS projects could drive future revenue growth and improve project margins.

- Strategic contract shifts and cost-saving synergies may enhance net margins and EBITDA, bolstering earnings growth.

- Operational challenges and geopolitical risks in renewables projects might affect margins and earnings, whereas increased oil and gas tenders hint at a strategic focus shift.

Catalysts

About Aker Solutions- Provides solutions, products, systems, and services to the oil and gas industry in Norway, the United States, Brazil, the United Kingdom, Malaysia, Angola, Brunei, Canada, India, and internationally.

- Aker Solutions is experiencing high order intake driven by new contracts, particularly in offshore wind and carbon capture and storage (CCS) projects. This suggests potential future revenue growth as these projects are executed.

- The company’s strategic shift from traditional lump-sum contracts to models with balanced risk-reward profiles and joint incentives is expected to improve project margins. This may result in better net margins as risks and upsides are more closely tied to Aker’s performance.

- Significant progress on projects such as Johan Castberg FPSO and Aker BP initiatives highlights Aker Solutions’ capability to deliver complex projects. Continued success and timely execution of these projects can drive future earnings growth and improve the bottom line.

- Ongoing development of synergies in its OneSubsea operations, alongside an ambition to save $100 million annually, points to cost reductions that could increase EBITDA margins over time.

- With a robust tender pipeline of NOK 85 billion, primarily in Europe, and anticipated growth in the subsea and lifecycle services segments, Aker Solutions is well-positioned to expand its revenue base in the coming years.

Aker Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

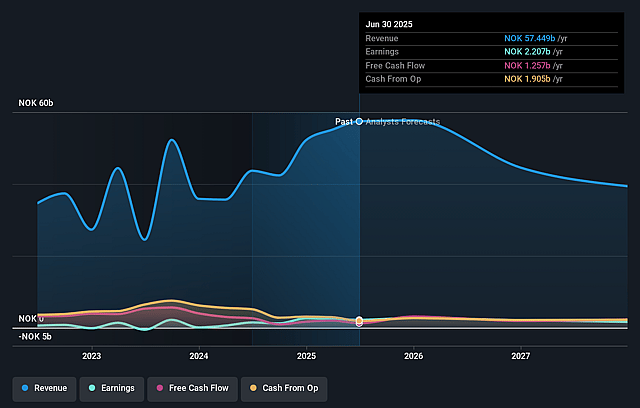

- Analysts are assuming Aker Solutions's revenue will decrease by 17.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 4.7% today to 3.7% in 3 years time.

- Analysts expect earnings to reach NOK 1.3 billion (and earnings per share of NOK 3.59) by about July 2029, down from NOK 2.9 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting NOK2.0 billion in earnings, and the most bearish expecting NOK835.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.3x on those 2029 earnings, up from 7.4x today. This future PE is greater than the current PE for the GB Energy Services industry at 6.3x.

- Analysts expect the number of shares outstanding to grow by 0.49% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.86%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The legacy renewables projects are described as both operationally and commercially challenging, which could continue to negatively impact net margins until 2025.

- Challenges in resolving commercial issues with clients and subcontractors in legacy renewables projects might prolong, creating uncertainties or additional costs, affecting earnings.

- The geopolitical situation, particularly concerning tariffs and trade restrictions, is being closely monitored and could potentially disrupt the supply chain, impacting future revenue and operational costs.

- The segment of oil and gas in the tender pipeline is increasing, suggesting a potential shift in focus that could impact long-term revenue stability if renewables don't perform as expected.

- Potential delays in client investment decisions due to geopolitical factors could affect the timing and realization of new orders, thereby impacting future revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NOK44.56 for Aker Solutions based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK70.0, and the most bearish reporting a price target of just NOK33.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NOK34.1 billion, earnings will come to NOK1.3 billion, and it would be trading on a PE ratio of 21.3x, assuming you use a discount rate of 6.9%.

- Given the current share price of NOK44.3, the analyst price target of NOK44.56 is 0.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Aker Solutions?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.