Last Update 16 Jun 26

GRAB: foodpanda Taiwan Deal And AI Will Support Long Term Upside

Analysts have made modest reductions to their average price targets on Grab Holdings, generally in the range of $0.10 to $1.00, as they factor in recent report updates on areas such as the foodpanda transaction, projected EBITDA timing and revised growth and margin assumptions.

Analyst Commentary

Recent Street research on Grab Holdings gives you a mixed picture, with some analysts seeing upside from the foodpanda deal and others trimming price targets as they reassess growth, margins and execution timelines. The balance of these views can help frame how you think about risk and reward in Grab stock.

Bullish Takeaways

- Bullish analysts highlight the foodpanda transaction as a potential long term positive for Grab Holdings, with one Jefferies report indicating the deal could add to EBITDA from 2028, which feeds into longer dated valuation models.

- The upgrade from China Renaissance signals that some on the Street see current pricing as attractive relative to Grab Holdings' execution on its regional platform and its path toward stronger profitability.

- Supportive commentary around future EBITDA contributions suggests that, if Grab delivers on integration and cost control, the stock could benefit from higher conviction in its earnings profile.

- Ongoing coverage and detailed modeling of items such as the foodpanda deal, growth assumptions and margin paths show that Grab Holdings remains firmly on the radar of major institutions, which can help with liquidity and price discovery.

Bearish Takeaways

- Several bearish analysts have trimmed price targets on Grab Holdings by amounts ranging from $0.10 to $1.00, reflecting more cautious views on growth pacing, margin expansion and timing of EBITDA improvements.

- JPMorgan price target adjustments of $0.10 and $0.20 and the $1.00 reduction cited for another large brokerage indicate that some models now assume more conservative execution or profitability outcomes.

- These lower targets suggest concern that the benefits from the foodpanda transaction and other initiatives could take longer than previously expected to be reflected in earnings and cash flow.

- For investors, the cluster of cuts from major firms, including JPMorgan and Morgan Stanley, underlines that the path to Grab Holdings' valuation targets may depend heavily on consistent delivery against EBITDA and margin milestones.

What’s in the News for Grab Holdings

- Grab Holdings agreed to acquire Delivery Hero’s foodpanda Taiwan unit for about US$600 million, subject to regulatory approval in Taiwan. The deal is expected to contribute at least US$60 million to adjusted EBITDA by 2028, according to recent news reports.

- The company highlighted plans for the foodpanda Taiwan integration that include income guarantees for delivery couriers, support for merchants, AI powered tools to help partners manage operations, and a focus on cybersecurity and compliance with local regulations, based on the same reports.

- Recent coverage described Grab Holdings as a central platform in Southeast Asia’s quick commerce market opportunity. The reports cited its role in food delivery, grocery and non food instant retail as well as its existing scale in food delivery as drivers of user engagement and operating leverage, according to a June 13, 2026 article.

- Grab launched GrabStays with travel technology partner Nuitée, adding hotel booking inside the Grab app. Users can access Nuitée’s global hotel inventory, earn GrabCoins on stays and use an AI chatbot to tailor accommodation choices, with Singapore as the first launch market in 2026.

- Grab and WeRide started public operations for the Ai.R autonomous ride service in Punggol, using autonomous shuttles that have accumulated 30,000 km of mileage during trials. The rollout also created new roles such as Safety Operator and Remote Operator for Grab driver partners.

Valuation Changes for Grab Holdings

- Fair Value: Model fair value for Grab Holdings stock is unchanged at $5.97, indicating no revision in the central valuation estimate.

- Discount Rate: The discount rate has edged lower from 8.14% to 8.13%, a very small adjustment to the risk assumption used in the valuation model.

- Revenue Growth: The forecast revenue growth rate is effectively unchanged at 19.98%, suggesting no material update to top line expectations in the latest model run.

- Net Profit Margin: The projected net profit margin is effectively flat at 15.70%, with the updated estimate differing only at the fourth decimal place.

- Future P/E: The assumed future P/E multiple is largely stable, moving slightly from 32.38x to 32.37x, indicating minimal change in how Grab Holdings' future earnings are being valued.

Key Takeaways

- Superapp ecosystem growth and fintech expansion are driving higher user engagement, new revenue streams, and long-term earnings potential.

- Tech investments and operational efficiencies are boosting margins, while advancements in urban mobility may further enhance future profitability.

- Increasing competition, regulatory risks, heavy incentive spending, and large tech investments threaten Grab's margins, revenue growth, and long-term profitability in core Southeast Asian markets.

Catalysts

About Grab Holdings- Engages in the provision of superapps in Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

- Accelerated digital payments and fintech adoption in Southeast Asia is expanding Grab's addressable market and boosting transaction volumes, as evidenced by the rapid growth in GrabFin and digital bank loan disbursals; this supports strong long-term revenue and earnings potential.

- Rising smartphone and internet penetration, alongside urbanization and expanding middle-class affluence across the region, is driving higher user engagement and increased frequency of usage within Grab's superapp ecosystem, underpinning robust GMV and top-line growth.

- Expansion and monetization of cross-vertical products (e.g., Mart, food delivery, premium rides, loyalty programs, and bundled services) are increasing revenue per user and creating new avenues for higher-margin advertising and financial services; this is expected to enhance margin and earnings over time.

- Operational efficiencies from continued tech investments (AI, automation, product-led growth, cost discipline) are producing operating leverage and improving net margins, as shown by margin improvement despite increased investment in affordability and new user acquisition.

- The ongoing development of autonomous vehicle fleets and partnerships positions Grab to benefit from future advancements in urban mobility, which could lower long-term costs, boost utilization, and drive new revenue streams, positively impacting profitability and long-term earnings growth.

Grab Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Grab Holdings's revenue will grow by 20.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.7% today to 15.7% in 3 years time.

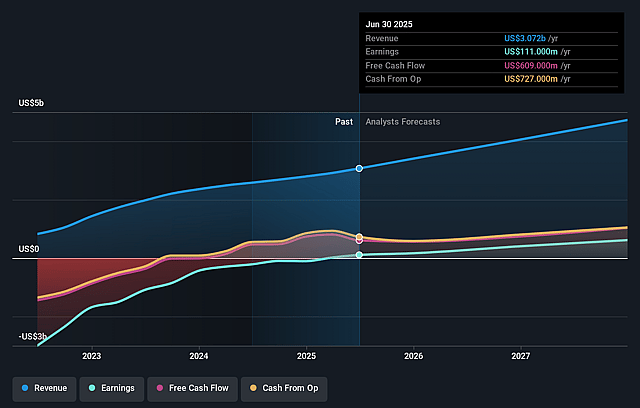

- Analysts expect earnings to reach $963.0 million (and earnings per share of $0.22) by about June 2029, up from $380.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $688.9 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.4x on those 2029 earnings, down from 37.5x today. This future PE is lower than the current PE for the US Transportation industry at 40.1x.

- Analysts expect the number of shares outstanding to grow by 0.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.13%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition in key markets, particularly Vietnam (with new food delivery entrants) and across Southeast Asia from both local and regional players, risks compressing take rates and increasing promotional spending, which may erode net margins and limit Grab's ability to sustainably grow earnings.

- Ongoing heavy investments in affordability (Saver rides/delivery) and persistent reliance on incentives (consumer incentive spending at 7%+ of GMV) could delay operating leverage, suppress underlying margins in Delivery and Mobility segments, and weigh on both revenue per user and overall earnings growth.

- Looming macroeconomic uncertainties in major markets (Thailand, Indonesia) and globally-such as consumption slowdowns and political/trade tensions-could constrain consumer discretionary spending, increasing volatility in core revenue streams.

- The prospect of regulatory changes (e.g., labor laws affecting driver classification, fintech/lending oversight) or licensing hurdles in Southeast Asian markets threatens to increase compliance costs and operational complexity, pressuring long-term profitability.

- High capital expenditure required for autonomous vehicle rollout and electrification, as well as the uncertain timeline and monetization path for these technologies, could strain free cash flow, raise fixed costs, and dilute returns if adoption or regulatory frameworks do not progress as expected.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $5.97 for Grab Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $8.0, and the most bearish reporting a price target of just $4.1.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.1 billion, earnings will come to $963.0 million, and it would be trading on a PE ratio of 32.4x, assuming you use a discount rate of 8.1%.

- Given the current share price of $3.48, the analyst price target of $5.97 is 41.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Grab Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.