Last Update 23 Jun 26

Fair value Increased 0.17%TCS: Expanding AI Partnerships Will Support Future Services Demand

Analysts have made a small upward adjustment to their fair value estimate for Tata Consultancy Services, with the price target moving from ₹2,939.58 to ₹2,944.56. This reflects updated assumptions around discount rates, revenue growth, profit margins and future P/E levels.

What's in the News

- Tata Consultancy Services has a board meeting scheduled for July 9, 2026, to consider audited standalone and consolidated interim financial results for the quarter ending June 30, 2026, and to consider an interim dividend for equity shareholders. (Source: Company board meeting notice)

- QAD | Redzone announced an expanded collaboration with Amazon Web Services and Tata Consultancy Services to offer an AI driven manufacturing platform that connects shop floor operations with enterprise systems, using cloud infrastructure and agentic AI to support modernization projects. (Source: QAD | Redzone announcement)

- Rezolve Ai and Tata Consultancy Services entered a global partnership under which TCS will resell Rezolve’s AI powered commerce platform to enterprise clients, with the technology also featured in TCS Pace Port innovation centers. (Source: Rezolve Ai announcement)

- PixerLens and Tata Consultancy Services agreed a joint offering that deploys PixerLens’ Annotet AI platform on the TCS SovereignSecure Cloud, giving enterprises AI based insights into application quality, performance and security, and aiming to meet data sovereignty and regulatory requirements. (Source: PixerLens announcement)

- Nokian Tyres is expanding its cooperation with Tata Consultancy Services, transferring maintenance and development of IT applications and related on site support to TCS from June 1, 2026, as part of Nokian Tyres’ broader IT transformation. (Source: Nokian Tyres announcement)

Valuation Changes

- Fair Value: The fair value estimate for Tata Consultancy Services is set at ₹2,944.56, compared with the earlier figure of ₹2,939.58, indicating a very small upward revision.

- Discount Rate: The discount rate assumption has risen slightly from 14.78% to 15.17%, indicating a modest change in the risk or return expectations used in the model.

- Revenue Growth: The revenue growth assumption is effectively unchanged, remaining at 6.30% based on the revised inputs.

- Net Profit Margin: The profit margin assumption remains broadly flat at 19.61%.

- Future P/E: The future P/E multiple used in the valuation has risen slightly from 25.57x to 25.87x, reflecting a marginally higher multiple applied to projected earnings.

Key Takeaways

- TCS is leveraging AI integration and talent development to enhance revenue growth and meet tech-driven project demands, boosting net margins.

- Strategic investment in AI, legacy modernization, and BFSI technology stack modernization poises TCS for market share growth and improved revenue.

- Revenue declines in key markets, coupled with delayed projects and shrinking operating margins, pose challenges to future growth and profitability.

Catalysts

About Tata Consultancy Services- Provides information technology (IT) and IT enabled services in the Americas, Europe, India, and internationally.

- TCS has seen significant traction and momentum in AI, particularly AI for business, which involves deploying AI across various value chains to improve customer experience and operational speed. This is expected to drive net new revenue opportunities and enhance revenue growth.

- The strong TCV (Total Contract Value) of $12.2 billion in Q4, with a good mix of large, medium, and small deals, is an indicator of future revenue visibility. This suggests a potential increase in revenue as these deals convert to actual projects and executions.

- Investments in talent development and an increase in the percentage of digital-specific hires, with a shift towards higher-end skills such as AI and GenAI, suggest that TCS is preparing to meet future demand for tech-driven projects. This strategic hiring is likely to support higher realization rates and improve net margins over time.

- The emphasis on modernizing technology stacks for BFSI clients, including legacy modernization and cloud adoption, should provide TCS opportunities for significant revenue gain as clients undertake comprehensive digital transformation initiatives.

- TCS's strategic focus on AI infrastructure investments, legacy modernization, and expanding its product portfolio and platforms indicate a strong potential for capturing a larger market share, which could lead to improvements in both revenue and operating margins as these businesses scale.

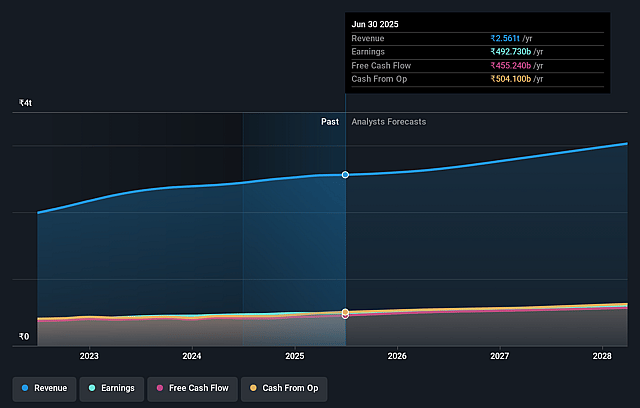

Tata Consultancy Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Tata Consultancy Services's revenue will grow by 6.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.4% today to 19.6% in 3 years time.

- Analysts expect earnings to reach ₹628.9 billion (and earnings per share of ₹173.44) by about June 2029, up from ₹492.1 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹706.6 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.9x on those 2029 earnings, up from 15.1x today. This future PE is greater than the current PE for the IN IT industry at 22.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.17%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- A decline in revenue from North America, the largest market, where revenue decreased by 1.9% year-on-year, poses a risk to future revenue growth.

- The Consumer Business Group declined by 0.2% and faces caution and delays in discretionary projects due to reduced consumer sentiment, impacting revenue growth.

- A potential slowdown in the manufacturing sector, particularly in the auto subsegment, due to uncertainties in the EV market and supply chain disruptions, could negatively affect future revenues.

- Instances of delayed decision-making and discretionary spending scrutinies in sectors like insurance and healthcare, driven by global economic uncertainties, could adversely affect revenue and earnings.

- Declining operating margins, affected by tactical interventions such as promotions and marketing expenses, suggest challenges in maintaining profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹2944.56 for Tata Consultancy Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3841.0, and the most bearish reporting a price target of just ₹2250.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹3207.6 billion, earnings will come to ₹628.9 billion, and it would be trading on a PE ratio of 25.9x, assuming you use a discount rate of 15.2%.

- Given the current share price of ₹2059.6, the analyst price target of ₹2944.56 is 30.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Tata Consultancy Services?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.