Last Update 24 May 26

Fair value Decreased 4.08%PMT: Recalibrated Earnings And Margins Will Support Future Upside Potential

Analysts have trimmed their average price target on PennyMac Mortgage Investment Trust by about $0.54 to $12.61, citing updated assumptions around fair value, discount rates, revenue trends, profit margins, and future P/E expectations.

Analyst Commentary

Recent research updates around PennyMac Mortgage Investment Trust point to a more balanced and selective stance. Several firms have lowered ratings or reduced price targets, with commentary focused on valuation assumptions, return hurdles, and how future earnings might track against prior expectations.

For you as an investor, the key takeaway is that analysts are recalibrating both upside and risk, rather than reacting to a single headline event.

Bullish Takeaways

- Analysts are still assigning explicit price targets, which suggests they see a range of potential outcomes that can be framed in valuation terms rather than a binary call on the stock.

- The emphasis on fair value and P/E assumptions indicates that some bullish analysts are focused on how earnings power, if sustained, could support current or moderately higher valuation multiples over time.

- By refining discount rate and margin assumptions, bullish analysts appear to be looking for scenarios where execution on revenue and cost control keeps the investment case intact, even at more conservative hurdle rates.

- The clustering of price targets around the low to mid teens signals that bullish views are anchored in incremental upside rather than aggressive growth stories. This can appeal if you prefer more measured expectations.

Bearish Takeaways

- Rating cuts toward more neutral stances point to concern that, at recent prices, the margin of safety relative to revised fair value estimates may have compressed.

- Lowered price targets suggest bearish analysts see pressure on prior assumptions around revenue trends and profit margins, which could make it harder for the stock to justify earlier valuation levels.

- Commentary around future P/E expectations signals caution that earnings visibility may not fully support previously used multiples, especially if growth or profitability falls short of earlier models.

- The spread of trims across multiple research houses highlights a shared concern that risk, return, and execution are now more finely balanced. This could cap near term enthusiasm even if longer term views remain open.

What's in the News

- PennyMac Mortgage Investment Trust and PennyMac Financial Services launched the "Welcome Home: Athlete Mortgage Program" to support Team USA athletes with homeownership resources and guidance (Key Developments).

- The program offers dedicated home lending experts who are focused on the distinct financial profiles of Team USA athletes (Key Developments).

- Athletes in the program gain access to exclusive home loan benefits and a range of mortgage options, including support for home equity, refinancing, and home purchases (Key Developments).

- The "Home Team Training Center" provides tailored educational content, webinars, and tools aimed at helping athletes make informed housing and mortgage decisions (Key Developments).

- The initiative builds on Pennymac's existing work with individual Team USA athletes and is now being expanded to the broader Team USA community through a partnership with the USOPC (Key Developments).

Valuation Changes

- Fair Value: Trimmed from $13.14 to $12.61, a modest reduction that narrows the implied upside versus prior assumptions.

- Discount Rate: Adjusted slightly higher from 9.01% to 9.01%, indicating a very small increase in the return hurdle used in the models.

- Revenue Growth: Updated from a prior decline of 28.48% to a smaller decline of 22.79%, reflecting less severe pressure on revenue in the latest assumptions.

- Net Profit Margin: Reduced from 57.05% to 51.38%, pointing to expectations for lower profitability on each dollar of revenue than previously modeled.

- Future P/E: Lowered from 9.35x to 8.89x, suggesting analysts are now applying a slightly more conservative earnings multiple to the stock.

Key Takeaways

- Vertically integrated operations and digital transformation enhance efficiency, enabling access to high-quality loans and driving potential revenue and earnings growth.

- Strategic investments in technology and partnerships foster operational scale, support stable earnings, and improve returns through high-quality assets and cost control.

- High exposure to interest rate risk, credit risk, unsustainable dividends, increased leverage, and declining loan growth threatens earnings stability and long-term investor confidence.

Catalysts

About PennyMac Mortgage Investment Trust- Through its subsidiary, primarily invests in residential mortgage-related assets in the United States.

- The continued growth in U.S. household formation and the steady demand for residential mortgages, combined with PennyMac's robust vertically integrated origination and servicing platform, position PMT to access a consistent pipeline of high-quality loans, supporting future revenue and earnings growth.

- Ongoing digital transformation and the ability to organically create securitizations through technology-enabled processes are enabling PMT to efficiently structure and retain higher-yielding credit-sensitive non-agency MBS and CRT assets, which could drive net margin expansion as operational efficiencies scale.

- A sustained increase in nonowner-occupied and jumbo loan volumes, facilitated by PMT's partnership with PFSI, is expected to create additional opportunities for the firm to deploy capital into attractive risk-adjusted return investments, potentially lifting future returns on equity (ROE) and net interest income.

- The strong demand from institutional investors for yield in a low interest rate environment is contributing to a resilient and active private label securitization market, providing PMT with favorable pricing and execution, which could support higher valuation multiples and improved capital access, benefitting long-term book value.

- Targeted strategic investments in loan servicing technology and infrastructure continue to reduce PMT's cost-to-service and enhance credit loss mitigation, supporting operational scale, contained operating expenses, and stable earnings, especially as the company benefits from low delinquency rates and high-quality underlying collateral.

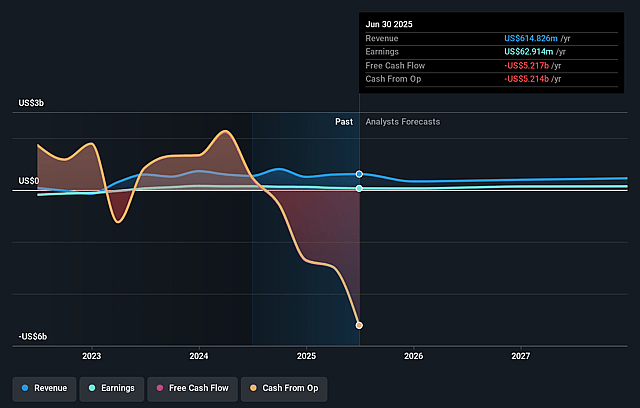

PennyMac Mortgage Investment Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming PennyMac Mortgage Investment Trust's revenue will decrease by 22.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.9% today to 51.4% in 3 years time.

- Analysts expect earnings to reach $159.8 million (and earnings per share of $1.57) by about May 2029, up from $100.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 9.0x on those 2029 earnings, down from 9.1x today. This future PE is lower than the current PE for the US Mortgage REITs industry at 11.5x.

- Analysts expect the number of shares outstanding to grow by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.01%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent exposure to interest rate and spread volatility, as seen in the most recent quarter's fair value declines and interest rate hedge losses, creates potential for ongoing book value declines and lower net interest income, especially if long-term rates rise or spreads widen.

- High reliance on non-Agency and jumbo securitizations increases credit risk; any deterioration in borrower credit or real estate values could increase delinquencies and default rates, adversely impacting revenue streams and net margins.

- Continued high dividend payout ratios remain unsupported by current run-rate earnings ($0.38 per share vs. $0.40 dividend), raising the risk of unsustainable dividends, possible dividend cuts, and reduced investor confidence, which would pressure share price multiples.

- The rapid increase in leverage, particularly via nonrecourse debt tied to retained securitizations, amplifies exposure to funding and liquidity risks in less robust MBS market environments, threatening earnings stability and capital structure robustness.

- Structural decline in mortgage refinancing and potential for persistent home affordability issues could limit the pool of new loans and dampen future correspondent production growth, putting pressure on PMT's origination-driven revenue and long-term earnings potential.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $12.61 for PennyMac Mortgage Investment Trust based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $11.25.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $311.0 million, earnings will come to $159.8 million, and it would be trading on a PE ratio of 9.0x, assuming you use a discount rate of 9.0%.

- Given the current share price of $10.5, the analyst price target of $12.61 is 16.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PennyMac Mortgage Investment Trust?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.