Last Update 06 Apr 26

AMG: Saudi Storage Projects And Earnings Quality Will Shape Future Share Returns

Narrative Update

The analyst price target for AMG Critical Materials has moved to €42, with analysts pointing to updated assumptions on discount rate, revenue growth, profit margin and a slightly lower future P/E multiple as key drivers of the change.

Analyst Commentary

Recent research updates on AMG Critical Materials point to a mixed backdrop. One major bank has moved to a more constructive stance with a €42 price target, while another raised its price target by €10. Even with these changes, research notes still highlight execution and valuation risks that readers should keep in mind.

The €42 target reflects updated assumptions on discount rate, revenue growth and profit margins, as well as a slightly lower future P/E multiple. For readers, the key takeaway is that analysts are placing more weight on the quality and visibility of future earnings than on short term share price swings.

At the same time, the €10 increase in the other price target suggests that expectations for the company’s earnings power and cash generation are under active review. The revised targets are anchored in detailed financial models, but they still come with clear caveats, especially around how consistently the company can execute on its plans.

Bearish Takeaways

- Bearish analysts flag that the use of a slightly lower future P/E multiple in recent models can signal concern that the market may be unwilling to pay as high a valuation for AMG Critical Materials if execution or growth disappoints.

- Some research commentary hints at downside risk if revenue growth or profit margins fall short of the assumptions embedded in the €42 target, which could leave the shares exposed to a derating if expectations prove too optimistic.

- Bearish analysts also point out that a €10 uplift in a price target, without a clearly stronger track record already in place, may leave limited room for error, increasing the focus on how management delivers against forecasts.

- There is an underlying concern that any change in discount rate assumptions could work against the stock if risk perceptions rise, which would pressure valuation even if headline earnings remain in line with forecasts.

What's in the News

- AMG Critical Materials, via its subsidiary AMG LIVA, plans to install its Hybrid Energy Storage System that combines Lithium Ion and Vanadium Redox Flow batteries with artificial intelligence and self learning algorithms at Aramco's Bulk Plant in Tabuk, Saudi Arabia, integrated into the site's existing solar plant (Company announcement).

- The Tabuk project is intended to support Saudi Arabia's 2030 Vision goals around carbon emissions reduction, wider use of renewable energy, and development of grid independent energy storage capabilities, positioning LIVA's system as part of that framework (Company announcement).

- The Hybrid ESS installation links to the broader IK Metals Reclamation and Catalyst Manufacturing Project, known as the IK Supercenter, which focuses on recycling metals such as vanadium concentrate from spent catalysts and gasification ashes from Aramco's Jazan facility to lower the carbon footprint versus classic mining (Company announcement).

- Through the jointly owned Advanced Circular Materials Company, the IK Supercenter is planned to include a vanadium electrolyte production plant intended to supply Saudi Arabia's vanadium flow battery market and support a made in KSA value chain for energy storage materials (Company announcement).

- AMG highlights its broader mission around critical materials and process technologies for a less carbon intensive world, with activities across lithium, vanadium, tantalum, advanced metallurgy, LIVA batteries, nuclear fuel via NewMOX SAS, and mineral processing in graphite, antimony, and silicon metal across production sites in multiple countries (Company announcement).

Valuation Changes

- Fair Value remained steady at €38.64, with no change between the prior and updated assessment.

- The Discount Rate rose slightly from 8.04% to 8.27%, implying a marginally higher required return in the updated model.

- Revenue Growth edged up from 4.73% to 4.93%, reflecting a modestly higher revenue growth assumption.

- Net Profit Margin moved from 6.47% to 6.69%, indicating a small uplift in earnings margin expectations.

- Future P/E was reduced from 15.61x to 14.97x, pointing to a slightly lower valuation multiple in the updated scenario.

Key Takeaways

- Technological changes, recycling trends, and evolving battery chemistry threaten long-term demand for AMG's core materials, risking revenue and asset utilization.

- Geopolitical tensions, resource nationalism, and commodity price swings heighten earnings volatility and may compress margins amid heavy ongoing investment.

- Strategic global expansion in refining, battery materials, and recycling strengthens AMG's position in critical supply chains, fostering steady revenue, margin growth, and order visibility.

Catalysts

About AMG Critical Materials- Develops, produces, and sells energy storage materials.

- Anticipated technological shifts in battery chemistry or large-scale substitution away from lithium or vanadium could significantly erode long-term demand for AMG's production base, leading to structural revenue decline and potential asset underutilization.

- Ongoing geopolitical risks and the rise of resource nationalism may disrupt supply chains, introduce new regulatory hurdles, and inflate costs for cross-border projects, all of which threaten to erode net margins and undermine future earnings predictability.

- Heavy capital expenditure required for ongoing expansion in lithium and chrome refining, alongside the ramp-up of new facilities, exposes AMG to material downside risk if projected demand growth falters or if pricing pressure intensifies, leading to lower return on capital and strained free cash flow for several years.

- Heightened exposure to commodity price volatility, particularly for lithium, vanadium, and antimony, leaves AMG's earnings profile vulnerable to periods of oversupply and cyclical price weakness, which can rapidly compress net margins and reduce profitability despite recent strong quarters.

- Accelerating adoption of circular economy practices, increased recycling rates, and decarbonization policies-especially in key markets-could suppress long-term demand for primary critical materials production, ultimately decreasing AMG's total addressable market, constraining revenue growth, and putting downward pressure on EBITDA over the coming decade.

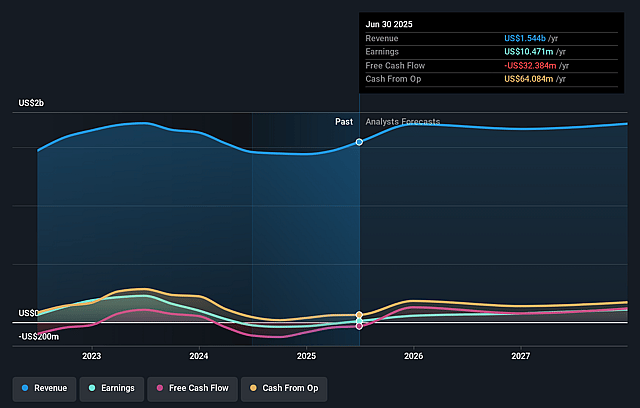

AMG Critical Materials Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on AMG Critical Materials compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming AMG Critical Materials's revenue will grow by 4.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -1.1% today to 6.7% in 3 years time.

- The bearish analysts expect earnings to reach $132.0 million (and earnings per share of $4.16) by about April 2029, up from -$18.6 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $266.1 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 15.1x on those 2029 earnings, up from -71.5x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 144.4x.

- The bearish analysts expect the number of shares outstanding to grow by 3.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.27%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The growing global focus on energy transition, electrification, and regional supply chain security is driving sustained and government-supported demand for critical materials such as lithium, vanadium, antimony, and chrome, which form the core of AMG's product portfolio and are highlighted as experiencing robust, multi-regional demand-potentially supporting long-term revenue and reducing demand risk.

- AMG is strategically expanding and investing in critical material refining in the US, EU, and Middle East, which aligns closely with industrial policies, government incentives, and regulatory requirements promoting domestic self-sufficiency; this enhances AMG's competitive positioning and underpins long-term customer contracts, likely contributing to stable or growing revenues.

- The continued ramp-up of AMG's battery-grade lithium hydroxide production and further investment in European and Brazilian lithium assets positions AMG at the center of European and global battery supply chains, a sector with multi-year secular growth projected to drive higher top-line sales and improved margins.

- AMG's high-and rising-engineering order backlog, particularly in its Technologies segment, suggests robust multi-year customer commitments across aerospace, energy, and industrial markets; this order visibility increases near

- and mid-term earnings predictability and could support upward pressure on net margins.

- AMG is expanding its recycling and spent catalyst processing businesses in the US, Europe, and Middle East, leveraging proprietary technology to create high-margin, circular-economy revenue streams poised to benefit from structural tailwinds around ESG, resource efficiency, and environmental regulations, supporting margin resilience and long-term earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for AMG Critical Materials is €38.64, which represents up to two standard deviations below the consensus price target of €43.51. This valuation is based on what can be assumed as the expectations of AMG Critical Materials's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €46.13, and the most bearish reporting a price target of just €38.64.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $2.0 billion, earnings will come to $132.0 million, and it would be trading on a PE ratio of 15.1x, assuming you use a discount rate of 8.3%.

- Given the current share price of €35.76, the analyst price target of €38.64 is 7.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AMG Critical Materials?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.