Last Update 22 Jul 26

Fair value Decreased 6.67%RGLD: Future Upside Will Hinge On Hod Maden Stake And Margin Resilience

The Royal Gold analyst price target has been trimmed from about $327.50 to roughly $305.67. This reflects analysts’ more cautious commodity price assumptions and expectations for near term margin pressure across gold and silver producers.

Analyst Commentary

Recent research on Royal Gold highlights a mixed set of views, with analysts adjusting price targets to reflect updated assumptions on gold and silver prices, cost trends, and project specific developments. For you as an investor, the key debate centers on how commodity price scenarios and operating updates might influence margins and valuation over the next few quarters.

Bullish Takeaways

- Bullish analysts continue to see Royal Gold as relatively well positioned within the precious metals group, with Buy or Outperform ratings maintained even as price targets are trimmed. This signals ongoing confidence in the company’s long term royalty and streaming model.

- Some research points to gold producers, including Royal Gold’s counterparties, still operating with near record margins and returning record capital. If this trend is sustained, it can support the value of the company’s royalty interests and its cash flow profile.

- Higher silver price assumptions in certain research updates support a more constructive view on parts of Royal Gold’s portfolio that are linked to silver. This can help offset pressure from more cautious gold price forecasts.

- The relatively modest target reductions from the high US$310s to just above US$300 in several reports suggest that, in bullish analysts’ view, recent commodity price and cost swings primarily warrant calibration to models rather than a reset in the long term equity story.

Bearish Takeaways

- Bearish analysts have taken a more cautious stance on Royal Gold, cutting targets more sharply into the low US$200s and assigning Underperform ratings. This reflects concerns about sector wide commodity price forecast reductions and their impact on valuation.

- Several reports reference a period of likely margin compression for gold related companies, driven by lower gold prices and elevated diesel and other costs. This could feed through to softer royalty revenue growth and weigh on earnings expectations.

- Commentary around a mixed Q2 reporting season, with tough comparisons and rising costs, points to execution risk and the potential for earnings volatility to pressure Royal Gold’s multiple in the near term.

- Project specific updates, such as the reduction of Royal Gold’s ownership in the Hod Maden project from 30% to 15%, are viewed by some bearish analysts as a headwind for longer term growth optionality. This in turn informs their lower valuation targets.

What’s in the News for Royal Gold

- Royal Gold authorized a share repurchase program on May 4, 2026, with Board approval for the company to buy back up to US$500 million of its common stock. (Source: Key Developments)

- Between May 4, 2026 and June 30, 2026, Royal Gold repurchased 147,205 shares, representing 0.17% of shares, for a total of US$30 million, completing this tranche of the buyback announced on May 6, 2026. (Source: Key Developments)

- Royal Gold was removed from the Russell 1000 Defensive Index. (Source: Key Developments)

- Royal Gold was also removed from the Russell 1000 Value-Defensive Index. (Source: Key Developments)

Valuation Changes for Royal Gold

- Fair Value: Trimmed from $327.50 to $305.67, a reduction of about 7% in the modeled estimate.

- Discount Rate: Adjusted slightly higher from 8.58% to 8.66%, indicating a modestly higher required return in the valuation work.

- Revenue Growth: Revised from 18.47% to 23.95%, reflecting a higher assumed growth rate for revenue in dollar terms.

- Net Profit Margin: Moved from 54.99% to 52.37%, pointing to slightly lower modeled profitability on earnings in dollar terms over the forecast period.

- Future P/E: Reduced from 36.44x to 31.25x, implying a lower valuation multiple applied to Royal Gold’s expected earnings.

Key Takeaways

- Strategic acquisitions and project investments diversify assets, reduce risk, and enhance exposure to gold and copper, supporting stable, long-term growth and margins.

- Increased scale and diversification attract broader investors, reinforce robust cash flows, and underpin consistent dividend growth and valuation strength.

- Heavy reliance on gold, operational setbacks at key mines, rising debt from acquisitions, premium deal competition, and geopolitical risks threaten profitability and revenue stability.

Catalysts

About Royal Gold- Acquires and manages precious metal streams, royalties, and related interests.

- The strategic acquisitions of Sandstorm Gold and Horizon Copper will significantly diversify Royal Gold's asset base, reducing single-asset risk and increasing exposure to long-term growth projects, which should drive more stable and growing revenue streams and improve net margins.

- Recent investments in projects like the Kansanshi gold stream (with a multi-decade production profile) and the Warintza copper-gold-moly project (large-scale development potential in the early 2030s) position Royal Gold to benefit from increasing demand for gold (as a hedge against inflation and geopolitical risk) and copper (driven by electrification and renewable energy adoption), supporting higher long-term revenue and earnings growth.

- The combination with Sandstorm and Horizon portfolios will make Royal Gold more attractive to passive and generalist investors due to greater scale and diversification; this could drive a larger investor base and valuation re-rating, positively impacting share price and EPS growth.

- Continued consistent reinvestment of robust free cash flows into new royalty and stream acquisitions, along with sector-leading geographic and asset diversification, supports stable or growing net margins and underpins the ability to raise dividends over time.

- Royal Gold's business model, with no direct operational exposure and a debt-free balance sheet (pre-acquisitions), enables strong cash flow resilience even through inflationary or cost pressures facing miners, supporting reliable earnings and dividend growth.

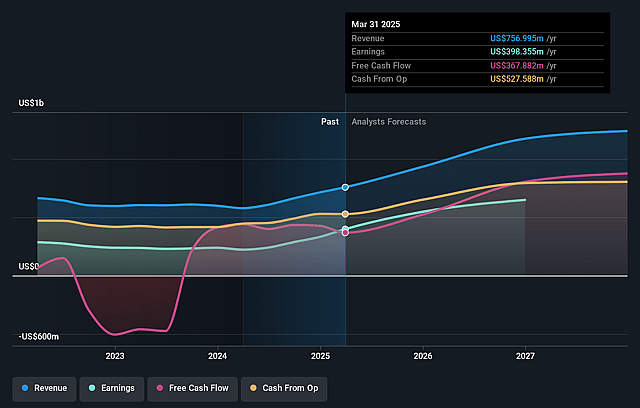

Royal Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Royal Gold's revenue will grow by 24.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 48.9% today to 52.4% in 3 years time.

- Analysts expect earnings to reach $1.3 billion (and earnings per share of $12.78) by about July 2029, up from $633.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 31.5x on those 2029 earnings, up from 26.9x today. This future PE is greater than the current PE for the US Metals and Mining industry at 17.3x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.66%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Royal Gold's revenue and margin growth is heavily reliant on gold, which represented 78% of total revenue this quarter; a long-term decline in global investment demand for gold or lower gold prices-potentially driven by a shift toward digital assets or global decarbonization reducing gold's appeal as a hedge-could significantly impair both topline and earnings.

- Multiple key assets, including Mount Milligan, Andacollo, and Xavantina, are experiencing production underperformance or reductions in guidance, and while management cites portfolio diversification, persistent operational or regulatory setbacks at a handful of large mines could materially reduce royalty revenue and earnings consistency.

- The planned Sandstorm Gold and Horizon Copper acquisitions will require the use of Royal Gold's revolving credit facility, increasing leverage to at least $1.2 billion; if integration benefits are delayed or anticipated cost and revenue synergies do not materialize, higher interest costs and debt could negatively impact net margins and constrain future dividend growth.

- Intensifying competition for high-quality royalty and streaming deals, as evidenced by recent portfolio actions, may force Royal Gold to pay premium pricing for new transactions, compressing future deal returns and threatening long-term profitability.

- Expanding exposure to African jurisdictions, such as Zambia and Botswana, adds heightened geopolitical and regulatory risk; increased political volatility or policy changes could disrupt local mine operations, reduce or delay royalty streams, and ultimately impact revenue predictability and bottom-line results.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $305.67 for Royal Gold based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $375.0, and the most bearish reporting a price target of just $209.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.5 billion, earnings will come to $1.3 billion, and it would be trading on a PE ratio of 31.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $201.26, the analyst price target of $305.67 is 34.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Royal Gold?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.