Last Update 25 Jun 26

JDG: Auditor Switch And Dividend Policy Will Support Future Upside Potential

Analysts have maintained their fair value estimate for Judges Scientific at £64.50. This reflects a slightly lower discount rate and a broadly unchanged forward P/E assumption, which together support a stable price target view.

What’s in the News for Judges Scientific

- Judges Scientific plc appointed RSM UK Audit LLP as external auditor for the financial year ending 31 December 2026, following an extensive tender process. This appointment replaces BDO UK LLP, which has resigned as auditor. Source: Company key developments.

- Shareholders at the Annual General Meeting on 20 May 2026 approved a final dividend of 82.3 pence per ordinary share. Source: Company key developments.

Valuation Changes

- Fair Value: The fair value estimate for Judges Scientific remains unchanged at £64.50 per share.

- Discount Rate: The discount rate has fallen slightly from 9.48% to 9.40%, reflecting a modest adjustment to the risk assumptions used in the valuation model.

- Revenue Growth: The long term revenue growth input continues to reflect a decline of around 1.16%, with no change from the previous assumption.

- Net Profit Margin: The net profit margin assumption remains steady at about 12.22%, indicating no update to profitability expectations in the model.

- Future P/E: The future P/E multiple has edged down slightly from 29.53x to 29.46x, a small reduction in the valuation multiple applied to Judges Scientific.

Key Takeaways

- Robust acquisition strategy and increased banking facilities support growth in revenue and earnings through strategic alignments.

- Focus on converting EBIT into cash increases financial flexibility, positively impacting net margins and debt repayment.

- Dependence on coring expeditions and geopolitical risks in China, alongside acquisition and economic challenges, threaten revenue, margins, and dividend sustainability.

Catalysts

About Judges Scientific- Designs, manufactures, and sells scientific instruments.

- Judges Scientific has a robust buy-and-build strategy focusing on acquiring manufacturers of scientific instruments, with a large pool of potential deals that could lead to significant revenue growth and improved earnings.

- The company is committed to converting EBIT into cash, enabling it to efficiently repay bank debts and increase its financial flexibility, likely impacting net margins positively.

- Recent strategic acquisitions, including Luciol, Rockwash, and Teer Coatings, enhance the company’s capabilities and synergies, positioning Judges Scientific for future revenue and earnings growth.

- Organic growth strategies and strong leadership teams driving operational excellence are expected to capitalize on market opportunities, positively impacting revenue and net margins.

- Increasing banking facilities provide greater acquisition firepower, supporting expansion and potentially driving up earnings through strategically aligned acquisitions.

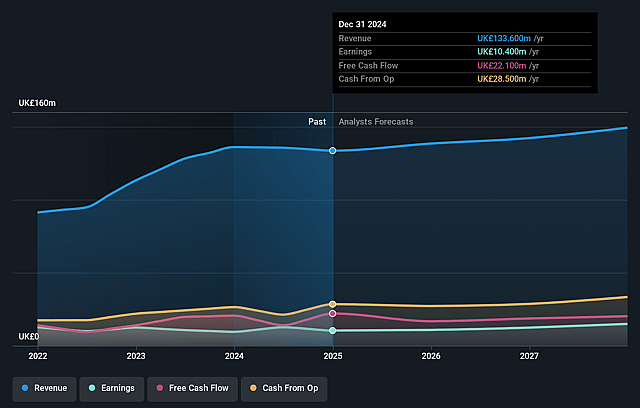

Judges Scientific Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Judges Scientific's revenue will decrease by 1.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.8% today to 12.2% in 3 years time.

- Analysts expect earnings to reach £17.2 million (and earnings per share of £1.33) by about June 2029, up from £5.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting £26.9 million in earnings, and the most bearish expecting £13.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.7x on those 2029 earnings, down from 56.6x today. This future PE is greater than the current PE for the GB Machinery industry at 23.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.4%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's dependence on coring expeditions for revenue growth poses a risk; missing an expedition year, as happened in 2024, can significantly impact revenues and overall financial performance.

- The decline in order intake and sales in China, a key market for Judges Scientific, highlights geopolitical risks and reliance on this region, potentially affecting future revenues and earnings.

- The company's financial performance is highly sensitive to its ability to find and integrate acquisitions successfully. A failure in M&A strategy could result in stagnant or declining profitability.

- Increased taxes and wage costs, particularly in the U.K., could squeeze net margins, impacting the company’s ability to maintain its promised yearly dividend increases, despite a focus on shareholder value.

- Fluctuations in global macroeconomic and political environments, including potential tariffs and research budget cuts in major markets like the U.S., present ongoing uncertainty that could affect future revenue and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £64.5 for Judges Scientific based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £72.0, and the most bearish reporting a price target of just £56.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £140.8 million, earnings will come to £17.2 million, and it would be trading on a PE ratio of 32.7x, assuming you use a discount rate of 9.4%.

- Given the current share price of £46.75, the analyst price target of £64.5 is 27.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Judges Scientific?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.