Catalysts

About Nova

Nova supplies process control and metrology tools that help semiconductor manufacturers improve yields in advanced logic, memory and packaging.

What are the underlying business or industry changes driving this perspective?

- Rising demand for AI and high bandwidth memory is pushing chipmakers to add DRAM and HBM capacity, and Nova is already winning tool of record positions and new memory customers. This can support continued product revenue and service revenue growth as those lines run harder.

- The industry shift to gate all around transistors at advanced nodes is creating more complex metrology needs, and Nova’s ELIPSON and METRION platforms are being adopted at multiple leading foundries. This can support product revenue and mix that is aligned with the company’s current gross margin range.

- Advanced packaging is becoming more critical as 2.5D, 3D and hybrid bonding architectures spread, and Nova’s growing suite of packaging tools, including WMC, PRISM and Ancolyzer, is already seeing broader use. This can increase the share of revenue from this area and support operating margins close to the current model.

- The new Mannheim production facility, which triples capacity for advanced packaging optical metrology, gives Nova room to ship more tools without a similar increase in fixed costs. This can help sustain free cash flow generation and support operating margin efficiency.

- A strong balance sheet with US$1.6b in cash and securities and a 0% US$750m convertible note gives Nova flexibility to invest in R&D and potential M&A in process control. This can add incremental revenue streams and support earnings per share over time.

Assumptions

This narrative explores a more optimistic perspective on Nova compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

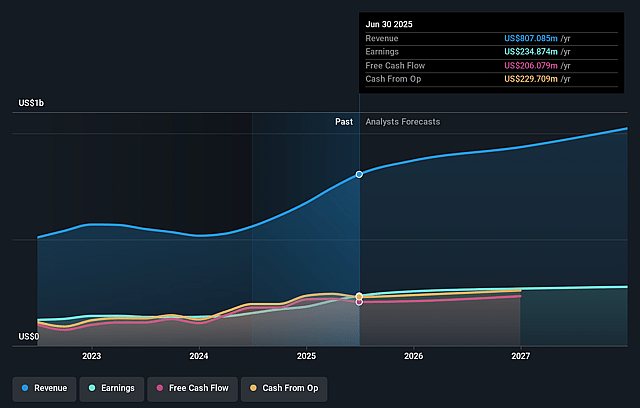

- The bullish analysts are assuming Nova's revenue will grow by 16.4% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 28.7% today to 30.9% in 3 years time.

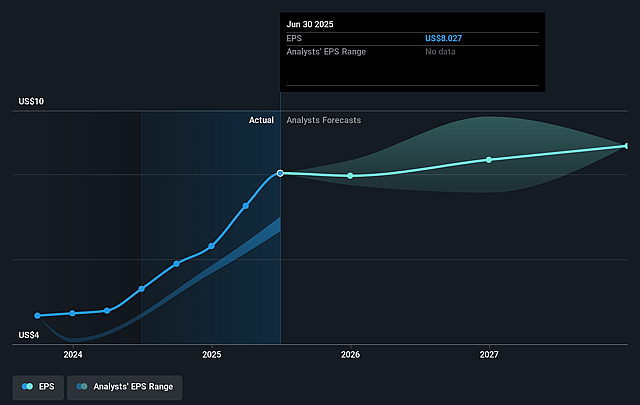

- The bullish analysts expect earnings to reach $416.0 million (and earnings per share of $12.21) by about February 2029, up from $245.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 56.9x on those 2029 earnings, up from 53.9x today. This future PE is greater than the current PE for the US Semiconductor industry at 42.2x.

- The bullish analysts expect the number of shares outstanding to grow by 2.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.95%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- AI related demand, DRAM, HBM and gate all around activity are key drivers in Nova's current story, so if wafer fab equipment spending for these nodes settles at lower levels over time than management currently expects, orders for ELIPSON, METRION, PRISM, WMC and related platforms could soften, which would put pressure on revenue growth and limit operating leverage in the long run, affecting earnings.

- The company is leaning into capacity expansions and higher operating expenses, including the new Mannheim facility and increased R&D. If industry growth slows or mix shifts away from Nova's stronger product lines, this added cost base could be harder to absorb, which would squeeze operating margins and reduce free cash flow over time.

- NOVA is increasing exposure to advanced packaging and gate all around at a small group of leading customers. If any of these chipmakers delay nodes, adjust tool choices or bring in competing metrology solutions, Nova's concentration could translate into lumpier demand, which would pressure product revenue and create volatility in earnings.

- China currently represents a meaningful but moderating share of business. Although management does not see a significant impact from restrictions today, tighter export controls, local substitution or policy changes over several years could cap Nova's long term opportunity in that region, which would act as a drag on overall revenue and limit gross margin upside if mix shifts toward lower margin geographies or products.

- The 0% US$750m convertible note and stated interest in M&A increase financial flexibility. If acquired assets underperform or require heavier investment than anticipated, shareholders could face both earnings dilution from higher share count and weaker return on capital, which would weigh on earnings per share and constrain future margin expansion.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Nova is $500.0, which represents up to two standard deviations above the consensus price target of $393.75. This valuation is based on what can be assumed as the expectations of Nova's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $500.0, and the most bearish reporting a price target of just $335.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.3 billion, earnings will come to $416.0 million, and it would be trading on a PE ratio of 56.9x, assuming you use a discount rate of 13.9%.

- Given the current share price of $445.66, the analyst price target of $500.0 is 10.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nova?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.