Last Update 16 Jul 26

Fair value Increased 2.45%SVT: Dividend Policy And Supportive Regulation Will Shape Balanced 3,500 GBp Outlook

The analyst fair value estimate for Severn Trent has moved modestly higher to £32.47 from £31.69, as analysts factor in updated assumptions on revenue growth, profit margins and future P/E multiples, against a backdrop of mixed price target revisions and a more supportive regulatory setting for UK water utilities.

Analyst Commentary

Recent Street research on Severn Trent reflects a mix of optimism and caution, with analysts adjusting price targets around the current fair value estimate while weighing the impact of the UK water sector's changing regulatory setting.

Bullish Takeaways

- Bullish analysts point to a more supportive UK regulatory backdrop for water utilities, which they view as helpful for Severn Trent's earnings visibility and long term investment planning.

- Several recent price targets in the £31.50 to £35.00 range suggest that some analysts see scope for Severn Trent to execute against regulatory allowances and capital plans while supporting its valuation.

- Positive ratings in the research set indicate confidence that Severn Trent can deliver on operational commitments and justify P/E assumptions embedded in updated fair value work.

- Incremental target increases from some bullish analysts imply that, within their models, small adjustments to revenue or margin expectations support a slightly higher valuation range for the stock.

Bearish Takeaways

- Bearish analysts have trimmed price targets in recent updates, highlighting concerns around how much upside is left relative to current valuation levels.

- Neutral stances in several reports signal that some analysts see Severn Trent as fairly valued, with limited room for outperformance if operational delivery or regulatory outcomes fall short of expectations.

- Recent downgrades point to a more cautious view on risk and reward, suggesting that any execution slip or change in sector sentiment could pressure the valuation embedded in current targets.

- The mix of raised and lowered price targets, often within a relatively tight band, underlines that analysts are debating the balance between Severn Trent's growth plans and the returns that can be justified in their models.

What’s in the News for Severn Trent

- Severn Trent has proposed a final ordinary dividend of 75.62 pence per share for the year ended 31 March 2026, in line with its stated AMP7 policy to adjust the dividend by at least CPIH each year. (Source: Key Developments)

- The proposed final dividend brings the total ordinary dividend for the year ended 31 March 2026 to 126.02 pence per share, compared with 121.71 pence per share for 2024/25. (Source: Key Developments)

- The final ordinary dividend is scheduled to be paid on 15 July 2026 to shareholders on the register at 29 May 2026, with an ex dividend date of 28 May 2026. (Source: Key Developments)

- Severn Trent has set its Annual General Meeting for 09 July 2026, where the proposed final dividend is expected to be considered by shareholders. (Source: Key Developments)

Valuation Changes for Severn Trent

- Fair Value: The analyst fair value estimate for Severn Trent has risen slightly to £32.47 from £31.69.

- Discount Rate: The discount rate used in the analysis is unchanged at 7.38%.

- Revenue Growth: Assumed long term revenue growth has risen slightly to 9.21% from 8.77%.

- Profit Margin: Assumed net profit margin has edged lower to 17.17% from 17.53%.

- Future P/E: The future P/E multiple in the model has risen slightly to 19.11x from 18.50x.

Key Takeaways

- Severn Trent's infrastructure investments and strategy focus on reducing spills and operational efficiency, aiming to elevate net margins and enhance performance rewards.

- Proactive increases in enhancement totex and insourcing design signal a strategic approach to statutory requirements, potentially boosting revenue and RCV growth.

- Regulatory changes and performance measures present financial challenges for Severn Trent, potentially affecting capital budgets, margins, earnings, and investor confidence.

Catalysts

About Severn Trent- Provides water and waste water services in the United Kingdom.

- Severn Trent’s commitment to achieving outperformance on Outcome Delivery Incentives (ODIs) for AMP8 suggests that they expect to continue leading in customer metrics and performance rewards, which could enhance future earnings.

- Focus on reducing spills and achieving global best practice levels (8 or fewer) by investing in infrastructure improvements and innovative solutions could lead to significant capital expenditure efficiency and potentially elevate net margins.

- The planned increase in enhancement totex investment, particularly in areas like treatment works and environmental improvements, indicates a proactive approach to meeting new statutory requirements, which could enhance revenue through higher allowable expenditure and RCV growth.

- Severn Trent’s strategy to insource design and expand in-house delivery capabilities for capital projects aims to improve operational efficiency, which may positively impact cost management and net margins.

- The expectation of continued strong performance in financing, despite high inflation, suggests that Severn Trent anticipates maintaining or improving their net interest margins and delivering steady Return on Regulated Equity (RoRE) performance.

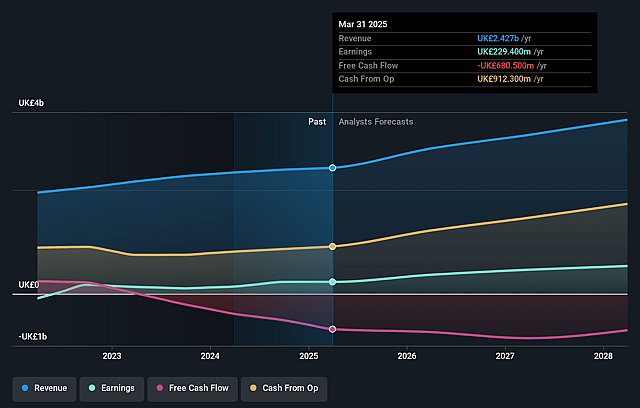

Severn Trent Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Severn Trent's revenue will grow by 9.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.1% today to 17.2% in 3 years time.

- Analysts expect earnings to reach £633.1 million (and earnings per share of £2.23) by about July 2029, up from £371.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as £786.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.1x on those 2029 earnings, down from 24.3x today. This future PE is lower than the current PE for the GB Water Utilities industry at 24.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The increased investment in enhancement totex spending, driven largely by statutory requirements like PFAS and dry weather flow standards, could pressure capital budgets and impact net margins if not adequately managed.

- Potential penalties or reduced rewards from the next AMP's ODI performance could impact Severn Trent's earnings, especially with concerns about industry-wide performance dragging them down.

- Rising employment costs, despite being partly offset by efficiency and insourcing strategies, may continue to put pressure on operating margins if not matched by sufficient gains in efficiency or revenues.

- The unpredictability of weather and its impact on spill rates poses a risk to meeting regulatory compliance and targets, which could impact operational metrics and associated financial rewards or penalties.

- Uncertainty around Ofwat's final determinations, specifically regarding cost allowances and the cost of equity, could affect future earnings predictions and financial planning, impacting overall investor confidence.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £32.47 for Severn Trent based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £36.2, and the most bearish reporting a price target of just £27.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £3.7 billion, earnings will come to £633.1 million, and it would be trading on a PE ratio of 19.1x, assuming you use a discount rate of 7.4%.

- Given the current share price of £29.8, the analyst price target of £32.47 is 8.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Severn Trent?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.