Last Update 24 Apr 26

Fair value Increased 35%VICR: Higher P/E Assumptions And Index Shift Will Shape Balanced Outlook

Analysts have raised their price target for Vicor from $208.75 to $282.50, citing updated assumptions for revenue growth, profitability, and long-term P/E multiples that are consistent with the latest Street research.

Analyst Commentary

Recent Street research includes a reported US$40 increase in the Vicor price target, which reflects updated assumptions around revenue growth, profitability, and long term P/E multiples. Analysts are using these revised assumptions to frame both upside potential and key execution risks.

Bullish Takeaways

- Bullish analysts view the higher price target as better aligning Vicor's valuation with peers that trade on premium long term P/E multiples tied to expected growth in core end markets.

- The updated assumptions for revenue growth and profitability suggest confidence that Vicor can scale its model over time, which supports the case for higher earnings power than previously built into forecasts.

- Some bullish analysts see the reset in valuation assumptions as helpful for reducing the gap between prior targets and current consensus expectations, which may provide clearer benchmarks for future execution.

- The price target increase is framed as consistent with recent Street work, which bullish analysts take as a sign that research views on Vicor are becoming more aligned around a constructive long term outlook.

Bearish Takeaways

- Bearish analysts point out that the higher price target relies on updated long term P/E multiples, which may be difficult to justify if revenue growth or margin expansion assumptions are not met.

- There is caution that the revised targets embed a meaningful amount of execution success, leaving less room for disappointment if product ramps, customer adoption, or cost controls fall short of current models.

- Some bearish analysts are wary that the valuation reset could raise expectations around future results, which might increase share price sensitivity to any miss versus Street assumptions.

- The dependency on long dated profitability and growth assumptions means that any shift in industry demand or competitive dynamics could require another round of estimate and target revisions.

What's in the News

- Vicor Corporation (NasdaqGS: VICR) was added to the S&P 400 index, reflecting a move into the mid cap benchmark (Key Developments).

- Vicor was added to the S&P 400 Industrials sector index, aligning the company with other industrial names in that benchmark (Key Developments).

- Vicor was dropped from the S&P 600 index as part of index changes that shifted the company out of the small cap benchmark (Key Developments).

- Vicor was dropped from the S&P 600 Industrials sector index following its move to the S&P 400 Industrials index (Key Developments).

- From October 1, 2025 to December 31, 2025, Vicor repurchased 42,800 shares for US$2.11 million, completing a total of 805,324 shares repurchased for US$35.92 million under the buyback announced on July 31, 2024, representing 1.79% of shares (Key Developments).

Valuation Changes

- Fair Value: price target moved from $208.75 to $282.50, representing a sizeable step up in the implied valuation level.

- Discount Rate: increased slightly from 8.99% to 9.11%, indicating a modestly higher required return in the updated model.

- Revenue Growth: revised from 26.48% to 40.93%, reflecting a higher assumed revenue growth rate in future projections.

- Profit Margin: adjusted from 31.78% to 30.17%, indicating a slightly lower projected net profit margin over time.

- Future P/E: edged up from 46.38x to 46.84x, implying a small increase in the multiple applied to projected earnings.

Key Takeaways

- Advanced power delivery products and automotive modules position Vicor to benefit from AI computing, electric vehicle trends, and expanded customer engagements in critical markets.

- Manufacturing investments, IP enforcement, and sector diversification underpin operational efficiency, premium margins, and stable long-term growth across multiple industries.

- Unpredictable demand, reliance on volatile licensing income, high fixed and legal costs, and slow diversification efforts create persistent revenue and earnings uncertainty.

Catalysts

About Vicor- Designs, develops, manufactures, and markets modular power components and power systems for converting electrical power for use in electrically-powered devices.

- The accelerated adoption of high-power, high-density AI computing in data centers is driving demand for advanced power delivery solutions-Vicor's Gen 5 vertical power delivery products and 800V-to-48V converters target this need, with customer engagements and sampling set to expand in Q3 and Q4. These next-gen products enable Vicor to address a market expected to exceed $5 billion by 2027, supporting long-term revenue growth and eventual margin expansion as manufacturing scales.

- The ongoing transition to electric vehicles-particularly the emergence of 48V zonal architectures and 800V-to-48V power conversion in automotive-presents a significant growth opportunity. Vicor's unique, high-efficiency automotive modules are gaining traction, with successful audits and new OEM engagements in Europe and Asia anticipated to drive share gains and topline growth through the decade.

- Persistent product innovation and strong IP enforcement-evidenced by recent litigation wins, ongoing licensing actions, and expansion of royalty streams-enable Vicor to defend premium pricing and realize incremental high-margin revenue from both settlements and ongoing royalties, enhancing net margin and earnings stability as the licensing base diversifies.

- Expanding manufacturing capacity and operational efficiency, with ongoing investments in U.S.-based production and automation, will eventually improve fab utilization and drive operating leverage-reducing unit costs and boosting gross margin as new product volumes ramp and addressable markets expand in data center, automotive, and industrial segments.

- Diversification into aerospace, defense, and industrial sectors alongside automotive and data centers reduces customer concentration risk; healthy pipelines and product introductions in these segments are expected to put these businesses on trajectories to double in size over 4–6 years, providing more predictable, less volatile revenue and earnings streams over time.

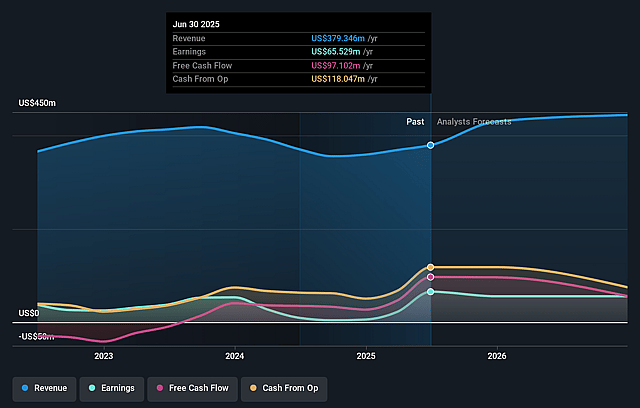

Vicor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Vicor's revenue will grow by 40.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 32.0% today to 30.2% in 3 years time.

- Analysts expect earnings to reach $360.4 million (and earnings per share of $5.95) by about April 2029, up from $136.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 47.1x on those 2029 earnings, down from 85.0x today. This future PE is greater than the current PE for the US Electrical industry at 34.1x.

- Analysts expect the number of shares outstanding to grow by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Book-to-bill ratio below 1 and a 9.6% sequential decrease in 1-year backlog suggest near-term demand weakness and order instability, particularly exacerbated by order cancellations in China and hesitancy around tariffs-risks that may persist and result in unpredictable or declining product revenue in the longer term.

- Significant reliance on licensing and patent litigation settlements for outsized quarterly financial performance adds volatility and uncertainty; management notes large quarterly swings and an inability to provide guidance, which may lead to unpredictable earnings and net margins if licensing outcomes falter or industry practices adapt to circumvent Vicor's IP.

- Vicor's ongoing underutilization of its newly constructed fab and slow capacity ramp in new product lines indicate that fixed costs may weigh on gross margins if product sales growth does not materialize swiftly enough to support full operating leverage.

- Heavy operational expenditure from litigation and ongoing enforcement of intellectual property, including contingency legal fees and variable legal costs, injects lumpiness into operating costs and could compress net earnings if settlement income becomes less frequent or costly enforcement persists as a core aspect of the business.

- Slow traction and lengthy qualification cycles in high-growth end markets such as automotive-where material revenue contributions are not expected until 2029–2030-raise the risk that growth from diversification initiatives may lag, raising future revenue uncertainty and exposing Vicor to ongoing volatility from customer concentration in current core markets.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $282.5 for Vicor based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $325.0, and the most bearish reporting a price target of just $260.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $360.4 million, and it would be trading on a PE ratio of 47.1x, assuming you use a discount rate of 9.1%.

- Given the current share price of $260.13, the analyst price target of $282.5 is 7.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vicor?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.