Last Update 26 Jun 26

Fair value Decreased 12%IPH: 2026 Lung Cancer Trial Data Will Support Higher Future Multiple

Analysts have trimmed their fair value estimate for Innate Pharma from €6.10 to €5.35, citing updated assumptions that combine higher revenue growth expectations with a much lower profit margin outlook and a substantially higher future P/E multiple.

What’s in the News for Innate Pharma

- Innate Pharma plans to present interim results from the Phase 2 MATISSE trial of IPH5201 in combination with durvalumab and platinum-based chemotherapy in resectable non small cell lung cancer at the AACR Annual Meeting 2026 in San Diego, California, during a Clinical Trials Plenary Session.

- The interim analysis on 40 patients in the MATISSE study reports pathological complete response rates of 35.7% in tumors with PD L1 expression of at least 1% and 50% in tumors with PD L1 expression of at least 50%, compared with a benchmark of durvalumab plus chemotherapy alone. (Source: company key developments)

- Based on the interim MATISSE data, patient recruitment is continuing for individuals with tumors expressing PD L1 of at least 1%. (Source: company key developments)

- IPH5201, described as a first in class monoclonal antibody targeting CD39 in the adenosine pathway, is being co developed with AstraZeneca and is currently evaluated in the multicenter Phase 2 MATISSE trial in perioperative treatment for resectable non small cell lung cancer. (Source: company key developments)

- Innate Pharma has scheduled a Special or Extraordinary Shareholders Meeting for May 21, 2026, at its Marseille headquarters at 117 avenue de Luminy, France. (Source: company key developments)

Valuation Changes for Innate Pharma

- Fair Value: trimmed from €6.10 to €5.35, reflecting updated assumptions in the Innate Pharma model.

- Discount Rate: kept broadly stable, moving slightly from 6.81% to 6.81%.

- Revenue Growth: revised upward from 50.46% to 65.92%, indicating a higher projected top line trajectory for Innate Pharma in the model.

- Net Profit Margin: reduced significantly from 35.40% to 6.59%, pointing to a much more conservative profitability assumption.

- Future P/E: raised sharply from 44.88x to 235.48x, implying a much higher valuation multiple embedded in the updated assumptions.

Key Takeaways

- A robust pipeline of innovative oncology therapeutics and drug candidates highlights strong R&D productivity potentially leading to substantial future earnings.

- Strategic partnerships, breakthrough therapy designations, and clinical trial progression indicate potential accelerated market entry and revenue growth in oncology treatments.

- Innate Pharma faces challenges in crowded markets, strategic partner dependencies, potential inefficacy concerns, and reliance on collaborations, affecting future revenue and profitability.

Catalysts

About Innate Pharma- A biotechnology company, develops immunotherapies for cancer patients in France and internationally.

- The recruitment of first patients into the Phase I dose-finding trial for IPH65 and the anticipated progression through dosing cohorts with data expected soon, reflects a potential increase in future revenue from oncology therapeutics targeting unmet needs.

- The initiation of patient dosing for the Nectin-4 targeted ADC, IPH45, and the planned escalation in clinical trials indicate a pipeline that could drive future revenues as these programs advance.

- The breakthrough therapy designation for lacutamab by the FDA, progressing partnership discussions, and preparation for Phase III trial align with potential accelerated approval, thus potentially impacting revenue growth through faster market entry.

- The expansion of Innate Pharma’s ANKET platform, including Fast Track designations and ongoing partnerships with entities like Sanofi, signifies an enhanced strategy for growing revenue streams from novel oncology and potentially autoimmune therapies.

- The robust pipeline consisting of late-stage assets and innovative drug candidates, such as the antibody-drug conjugates and NK cell engagers, indicates strong R&D productivity that could lead to substantial future earnings as these assets reach commercialization.

Innate Pharma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

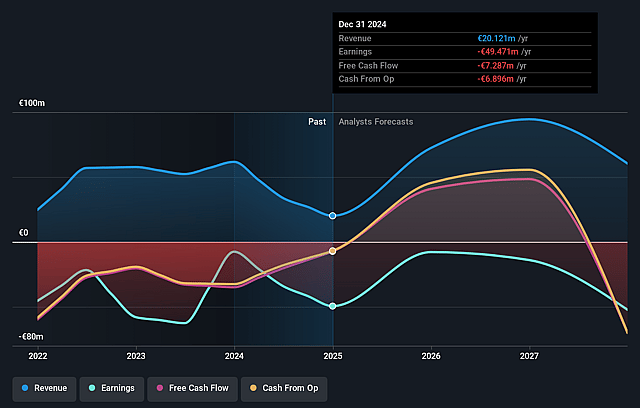

- Analysts are assuming Innate Pharma's revenue will grow by 65.9% annually over the next 3 years.

- Analysts are not forecasting that Innate Pharma will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Innate Pharma's profit margin will increase from -546.1% to the average GB Biotechs industry of 6.6% in 3 years.

- If Innate Pharma's profit margin were to converge on the industry average, you could expect earnings to reach €2.7 million (and earnings per share of €0.03) by about June 2029, up from -€49.2 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 237.6x on those 2029 earnings, up from -3.0x today. This future PE is greater than the current PE for the GB Biotechs industry at 16.9x.

- Analysts expect the number of shares outstanding to grow by 1.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.81%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The competitive landscape for non-Hodgkin lymphoma is crowded, which could impact the market potential and revenue from IPH6501 unless it proves to be significantly more effective or safer than existing therapies.

- Innate Pharma is relying on progressing strategic partnership discussions for the commercialization of its late-stage asset, lacutamab, which poses a risk if favorable partnerships are not secured, potentially impacting revenue and future earnings.

- The reallocation of IPH6401 from multiple myeloma to autoimmune diseases by Sanofi could be seen as a strategic uncertainty, as this new direction in an unproven field might impact future revenue streams negatively if the new indications do not demonstrate strong efficacy.

- The termination of the Phase I/II study for IPH6401 in multiple myeloma due to refocusing efforts may indicate inefficacy concerns, which can cast doubt on Innate Pharma's ability to generate returns from this asset, impacting expected future cash flows.

- The financial position shows a heavy reliance on research tax credits and collaborations for revenue, with operating expenses continuing to outpace this, which may affect profitability and cash management if new revenue streams fail to materialize in the mid-term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €5.35 for Innate Pharma based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €6.2, and the most bearish reporting a price target of just €4.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €41.1 million, earnings will come to €2.7 million, and it would be trading on a PE ratio of 237.6x, assuming you use a discount rate of 6.8%.

- Given the current share price of €1.59, the analyst price target of €5.35 is 70.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Innate Pharma?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.