Catalysts

About Nextdoor Holdings

Nextdoor Holdings operates a neighborhood focused digital platform that connects local residents, businesses and organizations.

What are the underlying business or industry changes driving this perspective?

- Rapid growth in self serve advertising, with Q3 self serve revenue up 33% year over year and now about 60% of total revenue, points to a scalable, higher margin channel that can lift total revenue and adjusted EBITDA as more local and mid market advertisers adopt the Nextdoor Ads platform.

- Completed programmatic supply integrations and the off platform deal with Yahoo give advertisers easier access to Nextdoor audiences, which can expand demand for ad inventory and support higher monetization and revenue per impression over time.

- Deeper focus on high quality local content, including more than 4,000 local publishers and growing use of alerts and recommendations, positions the platform as a daily utility for neighborhoods and can support higher ARPU and stronger earnings power as engagement deepens.

- Planned reinvention of the neighbor recommendations ecosystem, using authentic word of mouth and AI to surface trusted local businesses, can create more valuable ad and commerce formats that support higher revenue density and improved net margins.

- Disciplined cost management, reflected in positive Q3 adjusted EBITDA, workforce reduction savings and revenue per employee up 21% year to date, combined with US$403 million of cash and no debt, provides financial flexibility to invest in growth initiatives while working toward breakeven earnings in 2026.

Assumptions

This narrative explores a more optimistic perspective on Nextdoor Holdings compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming Nextdoor Holdings's revenue will grow by 9.5% annually over the next 3 years.

- The bullish analysts are not forecasting that Nextdoor Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Nextdoor Holdings's profit margin will increase from -24.6% to the average US Interactive Media and Services industry of 9.8% in 3 years.

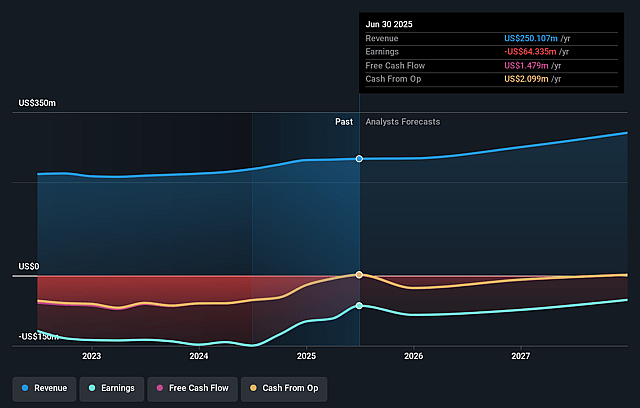

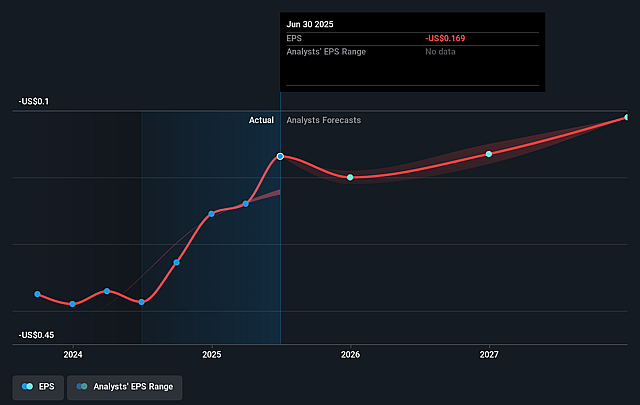

- If Nextdoor Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $32.5 million (and earnings per share of $0.08) by about January 2029, up from $-62.3 million today.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 64.1x on those 2029 earnings, up from -13.2x today. This future PE is greater than the current PE for the US Interactive Media and Services industry at 15.2x.

- The bullish analysts expect the number of shares outstanding to grow by 1.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.37%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Revenue growth in Q3 was 5% year over year and full year 2025 guidance is for 3% to 4% revenue growth, which is modest for a digital platform that still reports a GAAP net loss of $13 million. If demand for Nextdoor Ads and new ad formats does not accelerate meaningfully over time, the thesis that higher self serve adoption will materially lift revenue and earnings could be challenged, affecting long term revenue and earnings.

- Management is intentionally reducing notification and e mail volumes and expects Platform WAU to fluctuate, and is also pulling back on new user acquisition until the cold start experience is improved. If these choices do not translate into stronger engagement and a larger, more active user base, ARPU gains may not offset weaker usage trends, which would weigh on revenue and limit improvement in net margins.

- The plan to dramatically increase high quality content and rely more on user generated posts and neighbor recommendations comes after management acknowledged that content relevance had weakened in prior years. If efforts to scale content and recommendations do not materially change user behaviour or advertiser demand, the long term ambition to build a vibrant local ecosystem may fall short, constraining revenue growth and keeping earnings under pressure.

- The company is guiding to full year 2026 adjusted EBITDA breakeven after reporting a Q3 GAAP net loss and an expected full year 2025 adjusted EBITDA loss of about $3 million. This means the path to sustainable profitability still depends on continued cost discipline and operating leverage, and any need to re accelerate investment in product, content or user acquisition could delay or reverse margin progress, impacting net margins and earnings.

- Nextdoor is leaning into programmatic integrations and an off platform deal with Yahoo to give advertisers easier access to its audiences, but programmatic channels often exert pricing pressure on ad inventory over time. If higher volume through these integrations comes with weaker pricing or lower revenue per impression, overall monetization may not improve as expected, weighing on revenue and limiting expansion in adjusted EBITDA margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Nextdoor Holdings is $4.0, which represents up to two standard deviations above the consensus price target of $2.34. This valuation is based on what can be assumed as the expectations of Nextdoor Holdings's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $4.0, and the most bearish reporting a price target of just $1.1.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $332.9 million, earnings will come to $32.5 million, and it would be trading on a PE ratio of 64.1x, assuming you use a discount rate of 8.4%.

- Given the current share price of $2.1, the analyst price target of $4.0 is 47.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nextdoor Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.