Last Update 25 Jun 26

TTC: Raised 2026 Guidance And Productivity Gains Will Drive Further Upside

Analysts have reduced their price target for Toro to $100 from $105, citing updated models following Q2 results that showed slightly better demand across the business, even as valuation assumptions, including the future P/E multiple, were refined.

What’s in the News for Toro

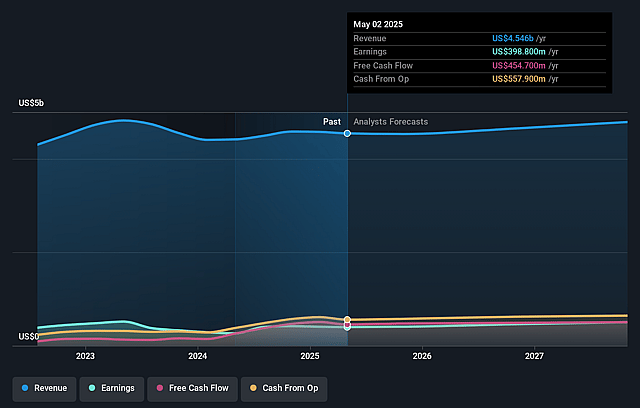

- Toro reported Q2 2026 revenue of about US$1.42b and adjusted EPS of US$1.60, with broad demand across residential and professional segments, according to recent earnings coverage.

- The Professional segment recorded 9.1% sales growth and margins of 20.3% in Q2 2026, helped by golf, grounds maintenance, landscape contracting, and underground construction, as reported in the Q2 2026 results.

- Integration of the Tornado acquisition contributed over 2 percentage points to Q2 2026 sales and was paired with new underground and specialty construction equipment, based on recent news reports.

- Toro’s AMP productivity program supported margin expansion and stronger cash flow in both Q1 and Q2 2026, and the company raised full-year adjusted EPS guidance to a midpoint of US$4.56, according to earnings summaries.

- The company increased its full-year 2026 total net sales growth guidance range to 4.0% to 6.5%, and declared a quarterly dividend of US$0.39 per share payable in July 2026, based on company guidance disclosures and Q2 2026 news coverage.

Valuation Changes

- Fair Value: Estimated fair value for Toro is unchanged at $109.25 per share.

- Discount Rate: The discount rate has risen slightly from 8.66% to about 8.68%, indicating a modestly higher required return in the updated model.

- Revenue Growth: Assumed long term revenue growth is effectively unchanged at about 3.77%.

- Net Profit Margin: Assumed net profit margin is effectively unchanged at about 10.51%.

- Future P/E: The future P/E multiple has risen slightly from about 21.78x to about 22.31x, reflecting a modestly higher valuation assumption for Toro.

Key Takeaways

- Strategic investment in automation, electrification, and productivity initiatives positions Toro for long-term premium growth, margin expansion, and improved profitability across core segments.

- Stabilized professional and recovering residential demand, alongside focus on sustainability and operational streamlining, underpin robust future revenue and earnings potential.

- Toro faces ongoing margin and earnings risks from weak residential demand, weather and macro volatility, cost pressures, rising competition, and limited international diversification.

Catalysts

About Toro- Designs, manufactures, markets, and sells professional turf maintenance equipment and services.

- Ongoing investments and recent product launches in smart, connected, and autonomous turf and irrigation solutions (e.g., GeoLink Mow Autonomous Fairway Mower, TurfRad moisture sensing) directly position Toro to benefit from increasing automation in landscaping and heightened focus on water conservation, supporting future premium product revenue growth and higher net margins.

- Professional segment momentum, driven by record golf participation and sustained infrastructure investment cycles, is providing multi-year order visibility and stable demand for advanced turf, grounds, and underground construction products, setting up for rising revenues and sustained earnings growth as markets recover.

- Acceleration of the AMP productivity program, with $75 million in run-rate cost savings and a longer-term target of $100 million+, is enhancing operating leverage and margins, while ongoing portfolio optimization and selective divestitures streamline core operations for improved future profitability.

- Channel inventory normalization and right-sizing in the residential segment, combined with maintained market share at key retailers, position Toro for a recovery in residential revenue and segment margins approaching historic 8–10% levels once consumer sentiment improves.

- Regulatory and customer shifts toward electrification and sustainability are catalyzing further adoption of Toro's battery-powered and electric equipment lines, leveraging R&D investments to capture market share and drive high-margin growth as emission standards tighten across the industry.

Toro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Toro's revenue will grow by 3.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.3% today to 10.5% in 3 years time.

- Analysts expect earnings to reach $546.9 million (and earnings per share of $5.76) by about June 2029, up from $339.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 22.5x on those 2029 earnings, down from 26.6x today. This future PE is lower than the current PE for the US Machinery industry at 27.5x.

- Analysts expect the number of shares outstanding to decline by 2.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.68%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistently weak demand in the residential segment, driven by homeowner caution on big-ticket purchases, prolonged low consumer confidence, and dealer hesitancy to restock, creates an ongoing drag on residential revenues and erodes residential margins, as reflected in significant year-over-year declines and the Spartan impairment charge.

- Heavy exposure to macroeconomic cycles and weather volatility, particularly with two consecutive years of low snowfall affecting both residential and BOSS business segments, increases unpredictability in revenue and inventory management, with potential negative impacts on future earnings if weather patterns or housing weakness persist.

- Elevated input costs (materials, manufacturing) and ongoing tariffs (especially on steel and China-sourced products) threaten net margins; despite current productivity and pricing mitigation strategies, future margin improvement could stall or reverse if inflation or new tariffs escalate.

- Rising competition and technological disruption in landscaping equipment (e.g., electrification, automation, smart connected products) requires continuous heavy R&D and capital investment; if competitors innovate more rapidly or Toro's adoption lags, it could result in long-term market share loss and muted earnings growth.

- Continued geographic concentration in North America and limited progress on expanding international professional/municipal markets leaves Toro vulnerable to regional economic slowdowns, shifts in infrastructure investment cycles, or changing regulatory/emissions standards, risking revenue concentration and increased earnings volatility.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $109.25 for Toro based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $5.2 billion, earnings will come to $546.9 million, and it would be trading on a PE ratio of 22.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $94.78, the analyst price target of $109.25 is 13.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Toro?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.