Catalysts

About Tri Pointe Homes

Tri Pointe Homes is a U.S. homebuilder focused on premium move up communities in key growth markets across the West, Central and East regions.

What are the underlying business or industry changes driving this perspective?

- Expansion into Utah, Florida and the Coastal Carolinas, supported by local leadership teams and over 32,000 owned or controlled lots, gives Tri Pointe a long runway to increase community count, which can support higher home sales revenue as these divisions scale and start contributing more meaningfully.

- Management is targeting an ending community count of about 155 communities in 2025 and a further 10% to 15% increase by the end of 2026, which, even under similar conditions to today, provides a volume growth engine that can help drive order growth and support earnings.

- The focus on premium move up buyers with average household income of about $220,000, FICO scores of 752 and 78% loan to value creates a financially resilient customer base, which can support pricing power and help protect gross margin and net margins.

- Strong liquidity of around US$1.6b, including US$792 million in cash and a homebuilding net debt to net capital ratio of 8.7%, alongside a US$450 million term loan that can extend to 2029, gives Tri Pointe flexibility to fund land investment and community openings, supporting future revenue and potential earnings growth.

- The company’s emphasis on well located communities near employment centers, top schools and amenities, combined with a premium brand and design driven product, positions it to capture persistent homeownership demand from needs based buyers, which can support absorption rates, sustain home sales revenue and help maintain gross margins over time.

Assumptions

This narrative explores a more optimistic perspective on Tri Pointe Homes compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming Tri Pointe Homes's revenue will decrease by 3.7% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 8.3% today to 5.8% in 3 years time.

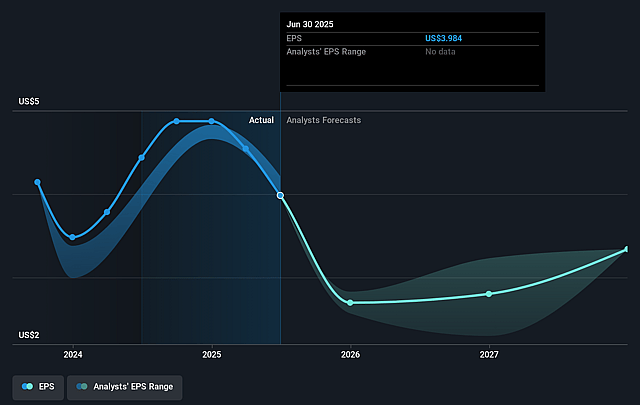

- The bullish analysts expect earnings to reach $194.9 million (and earnings per share of $2.76) by about January 2029, down from $310.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $165.2 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 21.8x on those 2029 earnings, up from 9.8x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.7x.

- The bullish analysts expect the number of shares outstanding to decline by 6.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.61%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Soft housing market conditions, with homebuyer interest described as muted and confidence weighed down by slow job growth and broader economic uncertainty, could persist and limit absorptions around the recent 2.2 homes per community per month pace. This would pressure home sales revenue and constrain earnings.

- The company relies heavily on premium move up buyers with an average household income of US$220,000 and a 78% loan to value ratio. Any long term pressure on higher income employment or tighter credit standards for this segment could reduce this pool of buyers and weigh on pricing power, which would directly affect gross margin and net margins.

- Tri Pointe plans to grow community count, including expansions in Utah, Florida and the Coastal Carolinas, supported by over 32,000 owned or controlled lots. If demand in these newer or lower average selling price regions remains soft, the company may need higher incentives or slower starts, which would drag on gross margin and earnings.

- The business is leaning on spec inventory to support near term deliveries, with about three quarters of orders currently from specs and higher incentives on these units at 8.2% of revenue. If the company struggles to rebalance toward more to be built homes, ongoing discounting could erode homebuilding gross margin and reduce net income.

- Although liquidity is high at about US$1.6b and the term loan has been increased to US$450 million, a long period of softer demand, elevated incentives and underutilized land and lot positions could reduce returns on capital and limit flexibility to keep repurchasing shares at historical levels. This would weigh on earnings per share and overall shareholder returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Tri Pointe Homes is $46.0, which represents up to two standard deviations above the consensus price target of $38.2. This valuation is based on what can be assumed as the expectations of Tri Pointe Homes's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $46.0, and the most bearish reporting a price target of just $31.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $3.3 billion, earnings will come to $194.9 million, and it would be trading on a PE ratio of 21.8x, assuming you use a discount rate of 9.6%.

- Given the current share price of $35.42, the analyst price target of $46.0 is 23.0% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Tri Pointe Homes?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.