Last Update 18 Jun 26

SDHC: Future Returns Will Rely On Order Recovery And Ongoing Buybacks

Analysts have kept the Smith Douglas Homes fair value estimate steady at $13.13 while making only marginal tweaks to the discount rate, long term revenue growth, profit margin, and future P/E assumptions, supported by recent neutral initiations from multiple research firms.

Analyst Commentary

Recent coverage on Smith Douglas Homes has centered on neutral ratings, with analysts focusing on how current execution and growth expectations line up with the fair value estimate of $13.13. For you as an investor, the commentary highlights both what could support that valuation over time and what might limit upside if execution or market conditions do not cooperate.

Bullish Takeaways

- Bullish analysts see Smith Douglas Homes as reasonably aligned with current assumptions on revenue growth and profitability, which they view as consistent with the reaffirmed $13.13 fair value estimate.

- The neutral initiations are viewed by some as a constructive starting point, suggesting that the stock does not require aggressive revisions to discount rate or P/E inputs to justify current expectations.

- Coverage initiation itself is seen as a positive, giving Smith Douglas Homes more visibility and potentially tighter consensus around key valuation drivers such as margins and earnings power.

- Bullish analysts highlight that only marginal adjustments were needed to long term growth and profit margin assumptions, which they see as a sign that existing forecasts are reasonably calibrated rather than volatile.

Bearish Takeaways

- Bearish analysts view the neutral stance as a signal that upside, relative to the $13.13 fair value estimate, may be limited unless Smith Douglas Homes delivers stronger than modeled execution on growth or margins.

- There is caution that the modest tweaks to discount rate and future P/E assumptions leave less room for error if company performance or market conditions turn out weaker than embedded in current estimates.

- Some see the alignment of multiple neutral views as a sign that Smith Douglas Homes may already reflect a fair balance of risks and rewards, which can constrain re-rating potential without a clear new catalyst.

- Bearish analysts flag that with only marginal changes to long term revenue and margin assumptions, any disappointment versus these expectations could pressure both earnings forecasts and the supported valuation range.

What’s in the News for Smith Douglas Homes

- Smith Douglas Homes completed a share repurchase of 449,604 shares, representing 4.99% of its shares, for $5.7 million under the buyback program announced on May 28, 2025.

- The repurchase activity took place from January 1, 2026 to March 31, 2026, according to the company’s buyback tranche update.

- Investors now have an updated reference point for Smith Douglas Homes’ capital return activity and share count following completion of this buyback tranche. Source: Key Developments

Valuation Changes for Smith Douglas Homes

- Fair Value: The $13.13 fair value estimate is unchanged, reflecting a steady view on Smith Douglas Homes stock.

- Discount Rate: Discount rate assumptions have fallen slightly, from 8.66% to about 8.55%, implying a modestly lower required return in the model.

- Revenue Growth: Long term revenue growth is effectively unchanged at about 9.24%, indicating stable expectations for revenue expansion in the forecast.

- Net Profit Margin: Net profit margin assumptions are essentially flat at about 23.93%, suggesting no meaningful shift in modeled profitability for Smith Douglas Homes.

- Future P/E: The forward P/E multiple used in the valuation has edged down slightly, from roughly 33.99x to 33.89x, a small adjustment to how future earnings are being valued.

Key Takeaways

- Growing reliance on buyer incentives and increased operating spend are compressing margins and delaying profitability amidst persistent market affordability challenges.

- Regional concentration and industry-wide cost inflation heighten revenue volatility and limit margin expansion despite ongoing inventory and geographic growth efforts.

- Strategic expansion, operational efficiency, and focus on affordable housing drive growth and resilience, supported by strong financial flexibility and disciplined balance sheet management.

Catalysts

About Smith Douglas Homes- Designs, constructs, and sale of single-family homes in the southeastern United States.

- The persistent affordability crisis, marked by rising home prices outpacing wage growth and stricter mortgage qualification standards, is leading Smith Douglas Homes to increase reliance on incentives (e.g., significant rate buy-downs and closing cost assistance) to stimulate demand, resulting in compression of gross margins and likely sustained downward pressure on earnings.

- Expectations of a structurally higher interest rate environment due to macroeconomic volatility and government debt concerns are compounding affordability issues for entry-level buyers-Smith Douglas Homes' core segment-potentially reducing future sales volumes and top-line revenue growth despite current inventory build-up and community expansion.

- Heavy concentration in the Southeast and Sun Belt regions exposes the company to elevated risk from localized economic downturns, housing oversupply (notably in new markets like Dallas-Fort Worth), or climate-related disruptions, increasing revenue volatility and risk to consistent earnings growth.

- The ongoing need to dedicate incremental SG&A spend to support geographic expansion (such as new greenfield entries in DFW and Gulf Coast) is likely to erode near-term operating leverage, delaying contributions to net margins and overall profitability, especially as new divisions run below optimal scale for several years.

- Industry-wide cost pressures from material input inflation, scarcity of affordable lots, and rising competition from institutional land buyers are expected to elevate build costs and constrain inventory turnover, creating further headwinds to margin expansion and dampening long-term ROE targets.

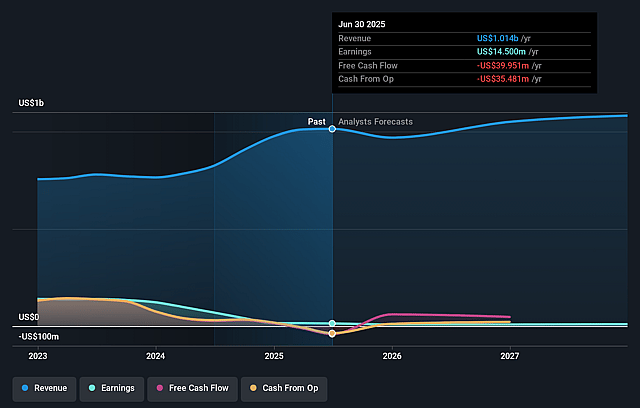

Smith Douglas Homes Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Smith Douglas Homes's revenue will grow by 9.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 0.9% today to 0.2% in 3 years time.

- Analysts expect earnings to reach $3.0 million (and earnings per share of $0.31) by about June 2029, down from $8.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 37.9x on those 2029 earnings, up from 12.9x today. This future PE is greater than the current PE for the US Consumer Durables industry at 13.3x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.55%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing geographic expansion and increases in active community count-including new entries into high-growth markets like Dallas-Fort Worth and the Gulf Coast-position Smith Douglas Homes to capture incremental revenue growth and market share, countering potential long-term sales declines.

- The company's "asset-light" and efficient land acquisition strategy (with 96% of unstarted lots optioned) provides significant operational and financial flexibility, which can mitigate downside risk and support healthy ROE and margins over the long term.

- Smith Douglas Homes' focus on entry-level and affordable homes aligns with the persistent, structural undersupply of attainable housing and expected continued demand from Millennial and Gen Z household formation, supporting robust revenue and volume growth prospects.

- Reduction in build cycle times and continued improvements in construction efficiency allow for faster inventory turnover, lower carrying costs, and stronger profitability-potentially insulating earnings even in a muted macro environment.

- The company maintains a conservative balance sheet, low net debt, expanded credit facilities, and authorized share repurchases, all of which enhance liquidity and financial flexibility, supporting potential EPS growth and decreasing the risk to net margins and cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $13.12 for Smith Douglas Homes based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $11.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $3.0 million, and it would be trading on a PE ratio of 37.9x, assuming you use a discount rate of 8.6%.

- Given the current share price of $13.25, the analyst price target of $13.12 is 1.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Smith Douglas Homes?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.