Last Update 26 Jun 26

Fair value Decreased 0.19%A259960: Share Repurchases And Refined Profit Outlook Will Support Future Returns

Analysts have slightly adjusted their price targets on KRAFTON, reflecting small changes in fair value estimates to around ₩373,130, along with updated assumptions for the discount rate, revenue growth, profit margin and future P/E multiples.

What's in the News for KRAFTON

- KRAFTON, Inc. announces a share repurchase program of up to ₩99,999.9 million in company stock, with the stated aim of acquiring and cancelling treasury shares to support shareholder value. (Source: Key Developments)

- The Board of Directors of KRAFTON authorizes a new buyback plan on April 30, 2026, providing formal approval for the latest repurchase initiative. (Source: Key Developments)

- From February 9, 2026 to March 31, 2026, KRAFTON repurchases 826,500 shares, representing 1.85% of shares, for ₩199,289.27 million under the February 9, 2026 buyback announcement. (Source: Key Developments)

- From April 1, 2026 to April 2, 2026, KRAFTON repurchases an additional 2,723 shares, representing 0.0061% of shares, for ₩709.17 million. This completes the repurchase of 829,223 shares, or 1.86%, for ₩199,998.44 million under the February 9, 2026 program. (Source: Key Developments)

Valuation Changes

- Fair Value: The updated fair value estimate for KRAFTON shifts slightly from around ₩373,833 to about ₩373,130 per share, reflecting a small refinement in the model.

- Discount Rate: The discount rate used in the valuation framework moves marginally from 8.86% to about 8.85%, indicating a very small adjustment in the cost of capital assumption.

- Revenue Growth: The assumed long term revenue growth rate edges from roughly 14.15% to about 14.36%, signaling a modest change in expectations for KRAFTON's top line trajectory.

- Net Profit Margin: The projected net profit margin is refined from about 23.83% to around 23.50%, pointing to a slightly lower profitability assumption in the updated model.

- Future P/E: The assumed future P/E multiple is adjusted from roughly 14.59x to about 14.68x, a minor change in the valuation multiple applied to KRAFTON's earnings.

Key Takeaways

- Diversifying game portfolio, expanding internationally, and embracing community-driven models support sustained growth, user retention, and recurring revenue opportunities.

- Strategic acquisitions and AI-driven efficiencies enhance productivity, broaden market reach, and help stabilize earnings while improving profit margins.

- Heavy investment in new projects and ongoing reliance on PUBG heighten operational risks, cost pressures, and the vulnerability of sustained profitability and shareholder returns.

Catalysts

About KRAFTON- Engages in the software development and related ancillary businesses in Asia, Korea, the United States, Europe, and internationally.

- KRAFTON's expanding focus on developing and publishing new global IPs beyond PUBG-including inZOI, Subnautica 2, and Last Epoch-diversifies revenue streams, reduces concentration risk, and leverages growing consumer appetite for premium online and mobile gaming content, supporting long-term revenue and earnings growth.

- The company's robust push into emerging and international markets (such as India, Europe, and North America), combined with regionally tailored publishing strategies and frequent collaborations, positions KRAFTON to benefit from rising mobile internet access and shifting digital consumption behaviors, directly impacting topline growth and user base expansion.

- KRAFTON's deepening investment in creator-driven and community-centric publishing models (evidenced by inZOI's viral community engagement and UGC strategy, as well as actively supporting streamers and advocates) is likely to drive higher player retention, time spent, and recurring in-game monetization, supporting higher gross margins and more predictable revenues.

- Ongoing R&D in AI-powered game development and operational efficiencies (demonstrated by substantial research outputs and the adoption of new technologies in game design) are expected to enhance development productivity, reduce long-term costs, and improve net margins.

- Strategic acquisitions-such as Eleventh Hour Games (Last Epoch) and ADK Group (ad tech and animation)-expand KRAFTON's addressable market and unlock new cross-platform and cross-media revenue opportunities, helping to smooth earnings volatility and fuel sustained revenue growth.

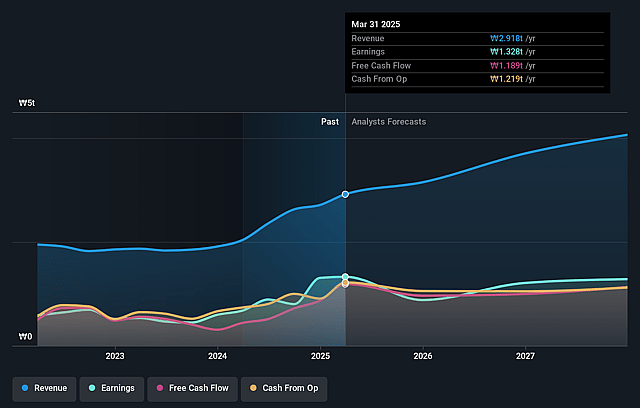

KRAFTON Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming KRAFTON's revenue will grow by 14.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 22.9% today to 23.5% in 3 years time.

- Analysts expect earnings to reach ₩1343.7 billion (and earnings per share of ₩27214.61) by about June 2029, up from ₩877.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₩1768.9 billion in earnings, and the most bearish expecting ₩976.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.9x on those 2029 earnings, up from 10.4x today. This future PE is greater than the current PE for the KR Entertainment industry at 10.4x.

- Analysts expect the number of shares outstanding to decline by 1.75% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.85%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- KRAFTON's aggressive investment in new IPs, global studios, and diversified publishing models increases capital expenditures and operational complexity, raising the risk that costly projects may not achieve commercial success, which could pressure future revenues and net margins.

- The postponement and legal dispute surrounding Subnautica 2 reveal execution risks and potential challenges in managing an expanded development pipeline, indicating possible future delays or underperformance that may negatively affect earnings and investor confidence.

- Overreliance on the PUBG franchise persists, with the majority of current revenue still concentrated in this IP, making the company vulnerable to shifts in gamer preferences, franchise fatigue, or competitive threats, which could cause long-term revenue and earnings volatility.

- Sustained increases in operating expenses, including higher labor costs, third-party development fees, and marketing expenditure, amidst slowing or uneven revenue growth across platforms, can erode net margins and limit long-term profitability improvements.

- Lack of clear and enduring shareholder return policies after the expiration of the 3-year plan, combined with ongoing high investment outflows and uncertainty about future dividends or buybacks, may reduce shareholder value and limit earnings per share growth over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₩373130.43 for KRAFTON based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₩500000.0, and the most bearish reporting a price target of just ₩297000.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₩5718.7 billion, earnings will come to ₩1343.7 billion, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 8.8%.

- Given the current share price of ₩208000.0, the analyst price target of ₩373130.43 is 44.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on KRAFTON?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.