Last Update 02 Jul 26

Fair value Increased 3.84%KYMR: Earlier Trial Completion And Oral Degrader Data Will Shape Balanced Outlook

Kymera Therapeutics’ fair value estimate increased from $119.19 to $123.76 as analysts lifted price targets into a $125 to $155 range, citing earlier than expected BROADEN2 trial enrollment completion for KT-621 in atopic dermatitis, accelerated timelines for key readouts and launch planning, and large modeled peak sales potential of $6 billion for the lead asset.

Analyst Commentary

Recent Street research around Kymera Therapeutics centers on how the BROADEN2 timeline shift and KT-621 opportunity could affect both valuation and execution risk. Analysts are reacting to earlier enrollment completion, updated readout expectations, and modeled revenue potential, while also weighing what has not yet been de-risked in the story.

Bullish Takeaways

- Bullish analysts see the earlier completion of the phase 2b BROADEN2 trial in atopic dermatitis as a sign that Kymera Therapeutics is executing ahead of prior internal timelines. They link this directly to higher target prices in the US$125 to US$155 range.

- The shift of the KT-621 readout to late 2026 from mid 2027 and the plan to start phase 3 in mid 2027 are viewed as pulling a key value catalyst closer. Bullish analysts argue this supports a higher equity value today.

- Modeled nominal peak sales of US$6b for KT-621 in atopic dermatitis are a core part of the more constructive valuation work. Some bullish analysts effectively treat KT-621 as Kymera Therapeutics' central long term growth driver.

- Some research notes point to strong clinician interest in an oral therapy with Dupixent like efficacy and enthusiasm among dermatology key opinion leaders. This is cited as supporting demand assumptions embedded in higher fair value estimates.

Bearish Takeaways

- Not all research is uniformly positive, with at least one update referencing a lowered price target. This signals ongoing debate about execution risk and how much of the KT-621 opportunity should be reflected in Kymera Therapeutics' valuation today.

- The investment case still leans heavily on a single lead asset, KT-621, which could concentrate risk if future trial data, regulatory feedback, or competitive dynamics do not match optimistic modeled outcomes.

- Timeline acceleration, while encouraging, also compresses the window for Kymera Therapeutics to address any development, manufacturing, or commercial readiness gaps before phase 3 and potential launch. Some cautious analysts may factor this into their risk adjustments.

- References to sector read through from transactions such as AbbVie’s planned takeover of Apogee Therapeutics highlight that part of the current enthusiasm for Kymera Therapeutics may be tied to broader inflammation and immunology sentiment. This can change if deal activity or sector appetite cools.

What’s in the News for Kymera Therapeutics

- Kymera Therapeutics completed enrollment in the global Phase 2b BROADEN2 trial of KT-621 for moderate to severe atopic dermatitis around six months ahead of schedule, bringing the expected topline data timing forward to year end 2026 from mid 2027 and contributing to a 16.6% move up in the stock on higher trading volume (source: recent news stories, company announcement).

- Director Bruce Booth and affiliated Atlas Venture funds sold more than 478,000 Kymera shares in open market transactions between April and June 2026, including sales under Rule 10b5-1 trading plans, while still retaining meaningful holdings. This came alongside a disclosed US$20m milestone payment from Sanofi tied to the start of a Phase 1 trial for KT-485, an oral IRAK4 degrader (source: recent news stories, SEC and company filings).

- Kymera shared additional Phase 1 data for KT-621, showing deep STAT6 degradation, clinical improvements and a favorable tolerance profile across multiple studies, and presented results in healthy Japanese adults that regulators can use to support participation in global Phase 2b programs (source: company conference presentations and press releases).

- Gilead Sciences exercised its option to exclusively license KT-200, an oral CDK2 molecular glue degrader, triggering a US$45m milestone payment to Kymera under their collaboration and taking total payments received so far to US$85m. Kymera is also eligible for up to US$750m in potential future payments and tiered royalties on any net sales (source: company collaboration announcement).

- KT-579, Kymera’s oral IRF5 degrader, generated additional preclinical data in lupus and inflammatory bowel disease models that the company reports as disease modifying and comparable or superior to existing therapies in those models, with a Phase 1 healthy volunteer trial ongoing and data planned for release in the second half of 2026 (source: EULAR, FOCIS and DDW conference presentations).

Valuation Changes for Kymera Therapeutics

- Fair Value: The updated fair value estimate has risen slightly from $119.19 to $123.76.

- Discount Rate: The discount rate has moved up marginally from 7.13% to 7.22%.

- Revenue Growth: The long-term revenue growth assumption has become less negative, shifting from a 7.35% decline to a 4.61% decline.

- Net Profit Margin: The assumed net profit margin is essentially unchanged, easing from 18.98% to 18.92%.

- Future P/E: The implied future P/E multiple remains very large, moving slightly lower from about 1,885.69x to 1,804.72x.

Key Takeaways

- Advancing clinical programs and strategic partnerships could increase market share and positively impact future revenue and earnings.

- Solid cash runway supports focused R&D investments, potentially boosting long-term growth without immediate financing pressures.

- High R&D expenses and reliance on partnerships pose risks to Kymera's long-term financial health and ability to maintain a leadership position in their sector.

Catalysts

About Kymera Therapeutics- Together with its subsidiary, a clinical-stage biopharmaceutical company, focuses on discovering and developing small molecule therapeutics that selectively degrade disease-causing proteins by harnessing the body’s own natural protein degradation system.

- Kymera Therapeutics plans to advance its STAT6 and TYK2 programs into several clinical stages, which could potentially increase future revenue due to the expansion into new treatment markets and therapeutic areas.

- The anticipated Phase II and III trials for their immunology pipeline aim to deliver biologics-like efficacy in oral form, which could enhance net margins by reducing manufacturing costs associated with biologics and potentially capturing a larger market share.

- The collaboration with Sanofi on the IRAK4 program, with expanded Phase II trials, positions Kymera to fast-track toward pivotal trials, potentially accelerating time-to-market and impacting future earnings positively.

- The company's strategy to introduce at least one new IND per year could expand their pipeline steadily, offering opportunities for revenue growth from licensing deals or partnerships.

- With a significant cash runway extending into mid-2027, Kymera can support its R&D activities without immediate pressure for additional financing, allowing focused investment in high-potential programs that could drive long-term earnings growth.

Kymera Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Kymera Therapeutics's revenue will decrease by 4.6% annually over the next 3 years.

- Analysts are not forecasting that Kymera Therapeutics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Kymera Therapeutics's profit margin will increase from -611.9% to the average US Biotechs industry of 18.9% in 3 years.

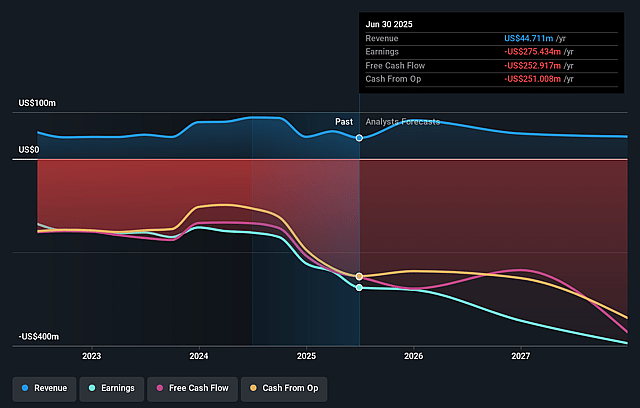

- If Kymera Therapeutics's profit margin were to converge on the industry average, you could expect earnings to reach $8.5 million (and earnings per share of $0.08) by about July 2029, up from -$315.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 1818.6x on those 2029 earnings, up from -29.8x today. This future PE is greater than the current PE for the US Biotechs industry at 16.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The transition to a video format for financial updates may not significantly impact investor perception or the company’s market value, and does not directly address any operational or financial performance issues.

- Competition in the STAT6 space has increased, which may impact Kymera's ability to maintain its leadership position and could affect future revenue streams.

- Although significant progress is being made with partners like Sanofi, reliance on partnerships exposes Kymera to risks if partners face challenges in advancing clinical trials, potentially impacting future earnings.

- The financial performance shows high R&D expenses with $71.8 million spent in the fourth quarter alone, which could strain resources and impact net margins if new drugs don't reach successful commercialization.

- Despite a significant cash balance, the projected cash runway into mid-2027 suggests that sustained high operational costs could pose a risk to long-term financial health if projected clinical milestones or revenue targets are not met.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $123.76 for Kymera Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $155.0, and the most bearish reporting a price target of just $97.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $44.7 million, earnings will come to $8.5 million, and it would be trading on a PE ratio of 1818.6x, assuming you use a discount rate of 7.2%.

- Given the current share price of $114.2, the analyst price target of $123.76 is 7.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kymera Therapeutics?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.