Last Update 18 Jun 26

STKS: Asset Light Expansion And Margin Outlook Will Drive Repricing Potential

Analysts have adjusted their price target for ONE Group Hospitality to $4.88. The change mainly reflects slightly refined assumptions around long term profit margins and future P/E multiples rather than a shift in the overall risk profile.

What’s in the News for ONE Group Hospitality

- ONE Group Hospitality issued earnings guidance for the second quarter ending June 28, 2026, with expected total GAAP revenue between US$202 million and US$206 million and consolidated comparable sales in a range of 1% to 2% (source: company guidance).

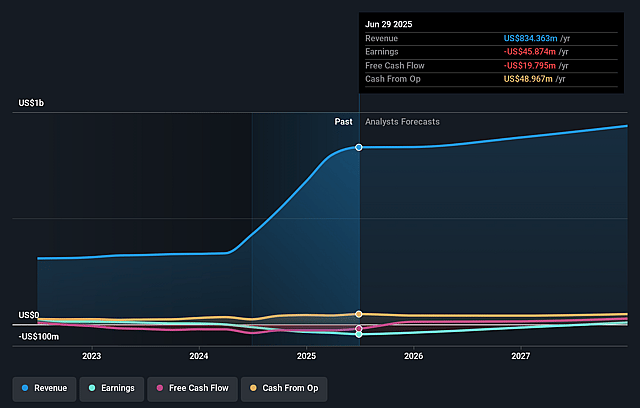

- The company reiterated full year 2026 guidance, projecting total GAAP revenue of US$840 million to US$855 million and consolidated comparable sales of 1% to 3% (source: company guidance).

- ONE Group Hospitality outlined its 2026 restaurant development pipeline, with three locations under construction, including owned STK restaurants in Phoenix, Arizona and New York, New York, and an owned Benihana restaurant in Seattle, Washington (source: company development update).

- The company reported an asset light expansion plan that includes a ten restaurant franchise development agreement for Benihana and Benihana Express in the Greater San Francisco Bay Area, California. This plan is intended to support West Coast growth while limiting capital needs (source: company development update).

- ONE Group Hospitality also disclosed a two restaurant commitment for a franchised Benihana and a licensed Benihana Express in the Florida Keys in partnership with an experienced operator, with a focus on execution quality (source: company development update).

Valuation Changes for ONE Group Hospitality

- Fair Value: The updated fair value estimate remains at $4.88 per share, indicating no change from the prior assessment.

- Discount Rate: The discount rate is unchanged at 12.46%, so the risk level used in the valuation is consistent with the earlier view.

- Revenue Growth: The long term revenue growth assumption is essentially steady at 8.34%, with only an immaterial refinement in the underlying calculation.

- Net Profit Margin: The projected net profit margin has risen slightly from 7.18% to 7.21%, reflecting a modestly stronger profitability assumption for ONE Group Hospitality.

- Future P/E: The future P/E multiple has been reduced slightly from 3.11x to 3.09x, indicating a marginally more conservative view of how much investors may be willing to pay for earnings.

Key Takeaways

- Operational redesigns, loyalty programs, and menu innovation are driving revenue growth, stronger margins, and broader customer engagement across core brands.

- Asset-light franchising and portfolio optimization are increasing high-margin, recurring revenue streams while focusing investment on scalable, high-return concepts.

- Weakening customer demand, brand concentration risk, and cost pressures combine with shifting consumer habits to threaten revenue growth, margin stability, and future investment prospects.

Catalysts

About ONE Group Hospitality- A restaurant company, owns, develops, operates, manages, licenses, and franchises restaurants and lounges worldwide.

- The integration and operational redesign of Benihana restaurants (e.g., the San Mateo prototype with higher table density and improved guest flow) is already generating above-target revenue and margins, suggesting rollout of these innovations systemwide will substantially boost future revenue and restaurant-level EBITDA margins.

- The expanded and unified loyalty program, coupled with an effective digital marketing push (leveraging a 7 million+ contact database), is likely to drive higher guest frequency and broaden the customer base-particularly as millennials and Gen Z prioritize experiential dining and digital engagement-supporting ongoing comparable sales and revenue growth.

- Fast acceleration of asset-light franchising, with Benihana (including Benihana Express) and STK seeing strong franchise interest from both new and existing partners, is set to deliver high-margin recurring revenue streams and higher returns on invested capital, paving the way for long-term growth in earnings and systemwide sales.

- Focus on menu innovation (such as the premium Wagyu program and new daypart/occasion offerings), pricing strategies, and weekday value programming positions the company to capitalize on rising disposable incomes and consumer demand for premium, differentiated, and experiential dining-fueling average check growth and improved net margins.

- Portfolio optimization (closure of underperforming or non-strategic Grill locations in favor of capital deployment toward brands with industry-leading returns) allows for improved free cash flow generation and margin expansion, as capital is increasingly directed toward scalable, high-ROIC concepts aligned with evolving dining and urbanization trends.

ONE Group Hospitality Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming ONE Group Hospitality's revenue will grow by 8.3% annually over the next 3 years.

- Analysts are not forecasting that ONE Group Hospitality will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate ONE Group Hospitality's profit margin will increase from -15.5% to the average US Hospitality industry of 7.2% in 3 years.

- If ONE Group Hospitality's profit margin were to converge on the industry average, you could expect earnings to reach $74.0 million (and earnings per share of $2.21) by about June 2029, up from -$125.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 3.1x on those 2029 earnings, up from -0.5x today. This future PE is lower than the current PE for the US Hospitality industry at 22.7x.

- Analysts expect the number of shares outstanding to grow by 1.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Declining comparable sales (down 4.1% in the quarter and projected between -3% and 1% for the year) signal that underlying customer demand is weakening, exposing revenue and earnings to ongoing consumer headwinds that could be exacerbated by secular shifts toward at-home dining and health-focused spending.

- The upscale and fine-dining focus of brands like STK and Benihana increases sensitivity to economic cycles and discretionary spending downturns; prolonged weakness or a recession could result in outsized volatility in traffic, compressing net margins and earnings.

- Heavy reliance on flagship brands, especially Benihana now representing over 55% of sales, exposes the company to concentration risk where brand fatigue, changing consumer tastes, or operational missteps could disproportionately affect revenue growth and profitability.

- The Grill Concepts segment is facing structural headwinds from changing entertainment habits (declining movie-going), seafood consumption declines, and low-cost sushi competition, making this part of the portfolio a potential drag on same-store sales and overall net margins.

- Persistently high food and labor costs, coupled with rising debt (higher interest expense), mean that inflation, commodity price shocks, or tighter labor markets could structurally compress margins and limit free cash flow, hampering future investment and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $4.88 for ONE Group Hospitality based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.25, and the most bearish reporting a price target of just $4.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.0 billion, earnings will come to $74.0 million, and it would be trading on a PE ratio of 3.1x, assuming you use a discount rate of 12.5%.

- Given the current share price of $1.85, the analyst price target of $4.88 is 62.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ONE Group Hospitality?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.