Last Update 23 May 26

Fair value Increased 0.095%OGDC: New Gas Wells And Dividend Will Support Future Earnings

Analysts have adjusted their PKR price target slightly from PKR 394.13 to PKR 394.50 for the oil and gas development stock. This reflects updated views on revenue growth, profit margins, and a modestly higher discount rate and future P/E assumptions.

What's in the News

- A board meeting is scheduled for April 29, 2026 to review the nine-month accounts to March 31, 2026 and consider any potential entitlement for shareholders (company announcement).

- An interim cash dividend of PKR 3.25 per share has been approved for the quarter ended March 31, 2026, in addition to PKR 7.75 per share already paid, with book closure from May 12 to May 13, 2026 (company announcement).

- Gas production from the Jand-1 well in Attock has been revived, with output reported at over 21 MMSCFD after recompletion and stimulation work, using corrosion-resistant tubing for sour service (company announcement).

- The Baragzai X-1 well in the Nashpa block has been brought into production, with reported output of about 5,300 BPD of oil, 17 MMSCFD of gas and 15 metric tons of LPG, supported by a new 8" x 8.1 km flowline to the Mela facility (company announcement).

- The Spinwam-1 discovery in the Waziristan Block has moved into extended well testing, with current reported production of around 40 MMSCFD of gas and 200 BBL/D of condensate, feeding early production facilities at Shewa (company announcement).

Valuation Changes

- Fair Value: PKR 394.50, slightly higher than the earlier PKR 394.13 estimate.

- Discount Rate: revised modestly higher from 23.91% to 24.02%.

- Revenue Growth: updated PKR revenue growth assumption has moved from 16.42% to 17.82%.

- Net Profit Margin: refined lower from 40.80% to 39.36%.

- Future P/E: forward valuation multiple is now 12.88x, compared with the prior 12.84x.

Key Takeaways

- Extensive exploration portfolio and discoveries could drive future growth by increasing revenue when developed and online.

- Optimized production techniques and new exploratory wells improve production efficiency, enhancing net margins through reduced operational costs.

- Production curtailment and increased exploration costs are challenging OGDCL, while exchange rate and circular debt issues threaten financial stability and earnings.

Catalysts

About Oil and Gas Development- Explores for, develops, produces, and sells oil and gas resources in Pakistan.

- OGDCL's extensive exploration portfolio and recent gas condensate discoveries could drive future growth, potentially increasing revenue as these discoveries are developed and brought online.

- Implementation of state-of-the-art production optimization techniques and rapid integration of new exploratory wells is expected to enhance production efficiency, likely improving net margins by reducing operational costs.

- Ongoing development projects, such as the Jhal Magsi development project and various compression projects, when completed, are anticipated to boost production capacity and revenue streams.

- Strategic efforts to sustain and maximize hydrocarbon output, including workover jobs and the installation of electrical submersible pumps, are aimed at mitigating production decline in mature fields, which should maintain or increase earnings.

- Participation in offshore blocks and potential involvement in projects like Reko Diq indicate long-term growth prospects, possibly enhancing future revenues and increasing the company's asset base.

Oil and Gas Development Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

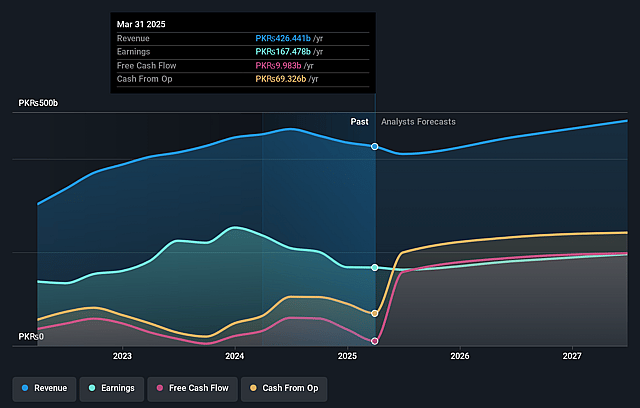

- Analysts are assuming Oil and Gas Development's revenue will grow by 17.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 39.8% today to 39.4% in 3 years time.

- Analysts expect earnings to reach PKR 251.3 billion (and earnings per share of PKR 60.52) by about May 2029, up from PKR 155.6 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.9x on those 2029 earnings, up from 8.9x today. This future PE is greater than the current PE for the GB Oil and Gas industry at 6.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 24.02%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- OGDCL's sales revenue has decreased by approximately PKR 29 billion due to forced production curtailment, impacting revenue negatively.

- The company faced challenges due to a dip in realized oil prices and strengthened PKR against USD, which negatively affected earnings.

- Exploration and prospecting expenditures increased by 57% due to dry holes, consuming financial resources with no short-term revenue return.

- The company experienced significant forced curtailment due to LNG influx and reduced gas demand, leading to reduced production and lower revenue potential.

- Potential circular debt issues and its impact on the company's cash flow and recovery rates could affect net margins and future financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of PKR394.5 for Oil and Gas Development based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of PKR522.0, and the most bearish reporting a price target of just PKR330.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be PKR638.6 billion, earnings will come to PKR251.3 billion, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 24.0%.

- Given the current share price of PKR323.51, the analyst price target of PKR394.5 is 18.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Oil and Gas Development?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.