Last Update 16 Jun 26

Fair value Decreased 0.078%QTWO: Best Of Breed AI Adoption Will Support Digital Banking Upside

Analysts have made a modest adjustment to their outlook on Q2 Holdings, trimming the average price target by about $0.06 to reflect slightly higher discount rate assumptions and a small shift in expected profitability, while still pointing to the company’s focused digital banking model and recent inclusion on a "Best-of-Breed" list as key supports for the thesis.

Analyst Commentary

Recent research on Q2 Holdings highlights a mix of optimism around the company’s digital banking focus and execution, alongside some caution reflected in recalibrated price targets and assumptions.

Bullish Takeaways

- Bullish analysts view Q2 Holdings as a focused digital banking and lending platform serving mid sized and large US financial institutions, which they see as supporting the company’s positioning and long term growth agenda.

- The inclusion of Q2 Holdings on a "Best of Breed" list reflects a view that the business opportunity, competitive moat, financial profile, and risk reward setup remain attractive at current levels.

- Analysts pointing to an "impressive string of strong quarterly bookings" and an uptick in new bookings activity see this as evidence that demand for Q2 Holdings’ solutions is translating into signed business, which can support future revenue visibility and execution.

- Some bulls maintain relatively higher price targets, indicating they still see upside potential if Q2 Holdings continues to execute on its digital banking strategy and converts bookings into sustained revenue and profit improvement.

Bearish Takeaways

- Bearish analysts have reduced their price targets, indicating a more cautious stance on how current assumptions around discount rates, profitability, or execution risk should factor into valuation for Q2 Holdings stock.

- Target cuts suggest some concern that prior expectations may have been too optimistic, especially around the timing or magnitude of profitability as Q2 Holdings continues to invest in its platform and growth plan.

- Revisions lower from several firms in close succession point to a view that the risk reward profile has become more balanced, with less room for error if growth in bookings or revenue does not track earlier expectations.

- These cautious views highlight sensitivity to macro and sector level factors that could affect bank technology budgets, which in turn may influence how quickly Q2 Holdings can translate its digital banking opportunity into earnings power.

What’s in the News for Q2 Holdings

- Q2 Holdings launched Q2 Assistant, an AI powered, context aware conversational interface embedded in its digital banking platforms to help bank and credit union staff resolve digital issues faster, with early adopters reporting measurable productivity and speed gains. Source: company product announcement.

- The company reported first quarter results that included steady subscription annual run rate, record new subscription bookings, and wider profit margins after its cloud migration. It also raised its 2026 revenue and EBITDA outlook above consensus, while Q2 Holdings stock fell about 7% on concerns around revenue growth trends and margin pressures. Source: Q1 earnings coverage.

- Q2 Holdings shares declined roughly 7% during a broad software sector selloff that investors linked to concerns about AI’s impact on traditional SaaS licensing models and softer trading volumes, even as the company continued to roll out AI focused products such as Q2 Assistant. Source: sector trading commentary.

- The company issued guidance for Q2 2026, stating expected total revenue of US$214.0m to US$218.0m, and for full year 2026, expected total revenue of US$875.0m to US$882.0m. Both ranges were described as implying 10% to 12% year over year growth. Source: company guidance.

- Q2 Holdings repurchased 1,764,582 shares for US$97.12m between January 1 and March 31, 2026, completing a total of 1,833,511 shares repurchased for US$102.12m under the buyback program announced on November 5, 2025. Source: buyback update.

Valuation Changes for Q2 Holdings stock

- Fair Value: Trimmed slightly from $74.31 to $74.25, reflecting a modest recalibration of underlying assumptions for Q2 Holdings.

- Discount Rate: Risen slightly from 8.82% to 8.91%, indicating a small adjustment to the required return used in the valuation framework.

- Revenue Growth: Kept broadly steady, with the long run rate remaining at 9.85%.

- Profit Margin: Reduced slightly from 16.07% to 15.84%, implying somewhat lower long term profitability assumptions for Q2 Holdings.

- Future P/E: Increased from 34.48x to 35.04x, suggesting a small uplift in the valuation multiple applied to forecast earnings.

Key Takeaways

- Accelerating digital transformation and demand for unified, mobile-first banking solutions are driving customer adoption and revenue growth for Q2's platform.

- Regulatory changes, bank consolidation, and operational efficiencies position Q2 for improved margins, increased cross-sell, and strong long-term retention.

- Customer base vulnerabilities, increased competition, and sluggish services growth could constrain revenue, while cloud migration offers long-term potential but carries near-term risks.

Catalysts

About Q2 Holdings- Provides digital solutions to financial institutions, financial technology companies, FinTechs, and alternative finance companies (Alt-FIs) in the United States.

- The increasing focus by financial institutions on digital transformation, evidenced by strong engagement and expanded investments in mission-critical digital banking, fraud prevention, and AI solutions, is likely to drive robust subscription revenue growth and improve retention for Q2 over the longer term.

- Heightened demand for integrated, omni-channel, and mobile-first banking experiences is accelerating adoption of Q2's unified platform across both new and existing customers, expanding the addressable market and supporting higher average revenue per user (ARPU) and overall revenue growth.

- The rise of regulatory initiatives around open banking, demands for data interoperability, and the growing complexity of managing multiple vendors is positioning Q2 as a preferred, scalable solution-particularly through the Innovation Studio platform-which should enable incremental cross-sell, increased customer stickiness, and margin expansion.

- Ongoing bank consolidation and sustained competition from fintechs is creating urgency among small and mid-sized financial institutions to modernize, with Q2 repeatedly cited as the platform of choice during M&A events; this dynamic supports continued recurring revenue growth and buffers against client attrition.

- Continued cloud migration initiatives and operational efficiencies are forecast to deliver higher gross margins and EBITDA, with additional opportunities for margin expansion once the data center transition completes in 2026, directly benefitting net earnings over time.

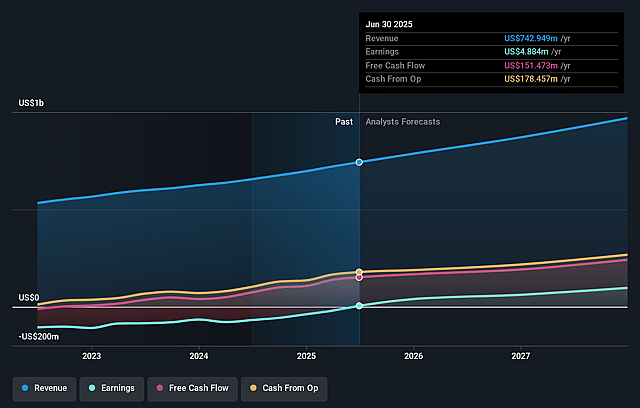

Q2 Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Q2 Holdings's revenue will grow by 9.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.0% today to 15.8% in 3 years time.

- Analysts expect earnings to reach $172.5 million (and earnings per share of $3.14) by about June 2029, up from $73.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 35.1x on those 2029 earnings, down from 37.3x today. This future PE is greater than the current PE for the US Software industry at 26.4x.

- Analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.91%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Continued consolidation among mid-sized banks and credit unions-a core Q2 customer segment-could further reduce its customer base and drive increased churn, potentially pressuring long-term revenue growth and overall ARR expansion.

- Higher-than-normal churn observed in the second quarter, in part due to M&A-related customer loss, indicates possible ongoing vulnerability to customer attrition, which could negatively impact subscription revenues and future earnings.

- The proliferation of point solution vendors in fraud and risk management introduces increased competitive risk, raising the threat of pricing pressure, potential customer defection, and margin compression over time.

- Flat or declining services and professional services revenue, as projected for 2025 and anticipated into 2026, may indicate limited growth opportunities in these segments, which could constrain total revenue growth if subscription momentum falters.

- Q2's continued migration to the cloud, while offering some margin benefit, involves transitional costs and operational risks, and any delay or unforeseen complications could impact near-term gross margins as well as long-term cost optimization and EBITDA growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $74.25 for Q2 Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $82.0, and the most bearish reporting a price target of just $63.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $172.5 million, and it would be trading on a PE ratio of 35.1x, assuming you use a discount rate of 8.9%.

- Given the current share price of $44.05, the analyst price target of $74.25 is 40.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Q2 Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.