Catalysts

About Donaldson Company

Donaldson Company focuses on filtration solutions across Mobile, Industrial and Life Sciences applications, using a recurring “razor to sell razorblades” model built around replacement parts.

What are the underlying business or industry changes driving this perspective?

- Power generation demand tied to electricity needs for data centers and AI infrastructure is filling Donaldson's power generation order books through the current fiscal year. This can support higher Industrial Solutions revenue and better fixed cost absorption over time, aiding operating margins.

- Growth in data creation and cloud storage is driving higher Disk Drive filtration needs, with Donaldson investing in new HAMR related technologies. This can support Life Sciences revenue growth and a mix shift toward higher margin products that benefit segment earnings.

- Food and beverage filtration is gaining share with OEMs and channel partners, with more first fit wins today laying groundwork for future replacement part demand. This can support recurring revenue and potentially steadier segment level margins.

- Expansion in Mobile Aftermarket, including double digit growth in the independent channel and deeper partnerships such as NAPA, increases Donaldson's installed base and replacement pull through. This can support Mobile Solutions revenue and help sustain pretax margins around current levels.

- Footprint and cost optimization initiatives, including plant consolidation and region for region manufacturing, are reducing structural costs and tariff exposure. This can support gross margin expansion and higher company wide operating margins as projects complete.

Assumptions

This narrative explores a more optimistic perspective on Donaldson Company compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

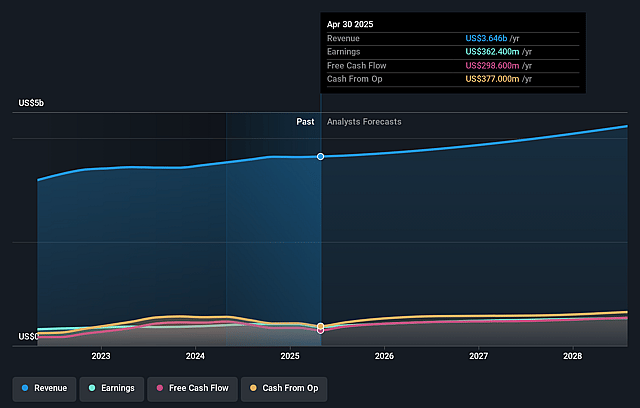

- The bullish analysts are assuming Donaldson Company's revenue will grow by 5.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 10.2% today to 13.0% in 3 years time.

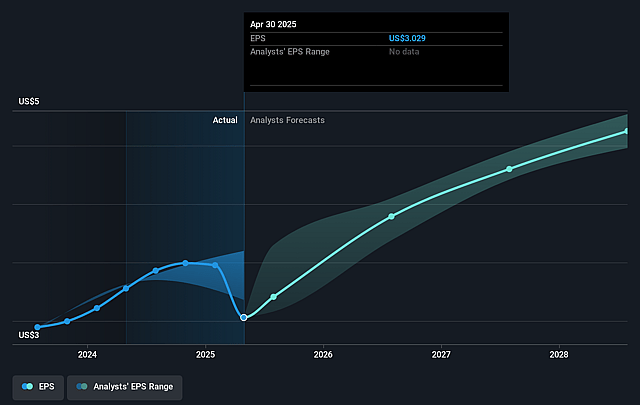

- The bullish analysts expect earnings to reach $564.3 million (and earnings per share of $4.98) by about January 2029, up from $381.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 28.1x on those 2029 earnings, down from 30.4x today. This future PE is greater than the current PE for the US Machinery industry at 27.1x.

- The bullish analysts expect the number of shares outstanding to decline by 3.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.45%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Power generation order books are full only through the current fiscal year, and the company highlights that project timing can be lumpy and dependent on customer site readiness. Any slowdown or delay in data center and AI related projects could soften Industrial Solutions growth and limit the expected lift to revenue and operating margin.

- Disk Drive filtration is currently growing at over 20% on the back of HAMR related technology and cloud storage demand, yet management already expects that trend to moderate in coming years. If demand for traditional disk based storage slows faster than anticipated, Life Sciences revenue and segment margins could come under pressure.

- The company is in the heavy lift phase of footprint optimization, with structural cost benefits still limited and most efficiencies expected in the back half of fiscal 2026. Execution issues, start up challenges in new facilities or delays in project completion could cap gross margin expansion and keep operating margins below current expectations.

- Several end markets are described as cyclical or at trough or near trough levels, and regions like Latin America and China are being approached cautiously. A weaker or slower than expected recovery in these geographies and sectors could restrain Mobile Solutions and Industrial Solutions sales growth and weigh on earnings.

- Tariffs are still estimated to be a US$25 million annual headwind and pricing has normalized to pre COVID type conditions. If further tariff changes occur or customers resist additional pricing actions, that could squeeze gross margin and limit the improvement in net margins that bullish expectations rely on.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Donaldson Company is $120.0, which represents up to two standard deviations above the consensus price target of $97.2. This valuation is based on what can be assumed as the expectations of Donaldson Company's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $120.0, and the most bearish reporting a price target of just $77.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $4.3 billion, earnings will come to $564.3 million, and it would be trading on a PE ratio of 28.1x, assuming you use a discount rate of 8.4%.

- Given the current share price of $100.62, the analyst price target of $120.0 is 16.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Donaldson Company?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.