Last Update 23 Jun 26

BELF.A: Operational Reset And Defense Exposure Will Support Next Upside Phase

Bel Fuse's analyst price target has been revised to $370, as analysts point to the company's multi year operational reset, focus on accountability and pricing discipline, and expectations for future revenue growth as key reasons for the updated view.

Analyst Commentary

Recent research on Bel Fuse highlights a mix of enthusiasm about the company’s reset and some caution around execution and valuation, giving investors a more rounded view of the updated US$370 price target.

Bullish Takeaways

- Bullish analysts point to Bel Fuse’s multi year operational reset, with a focus on accountability and pricing discipline, as a key driver behind the higher price targets and the upgraded view on the stock’s potential.

- JPMorgan highlights Bel Fuse’s role in powering, protecting, and connecting electronic circuits across aerospace and defense, networking and data centers, telecom, and industrial markets, which they view as a supportive backdrop for long term demand.

- The US$370 target is framed by bullish analysts as being tied to improved operational delivery, with the view that better execution could support stronger earnings power and justify a higher valuation range over time.

- Expectations for revenue growth cited in the JPMorgan research, including projected growth figures for 2026 and 2027, are used by bullish analysts to support the case for Bel Fuse’s ability to scale its business model.

Bearish Takeaways

- Bearish analysts may view the high level of optimism around the US$370 target as leaving less room for error if Bel Fuse’s operational reset takes longer or proves harder to sustain.

- The reliance on broad end markets such as aerospace and defense, networking, telecom, and industrial can be a concern if demand in any of these areas softens, which could weigh on the company’s growth assumptions used in valuation work.

- Some cautious investors may question whether the company can consistently maintain pricing discipline as competition and customer budgets shift, which could impact margins and the earnings profile implied in recent price targets.

- The emphasis on multi year improvements sets a high execution bar, so any slip in operational delivery or delayed benefits from the reset may lead to reassessment of the upside embedded in current analyst targets for Bel Fuse.

What’s in the News for Bel Fuse

- Bel Fuse completed a follow on equity offering of 1,500,000 shares of Class B common stock, raising US$399 million at a price of US$266 per share, with a discount of US$9.975 per share.

- The company previously filed a follow on equity offering for 1,300,000 shares of Class B common stock, signaling continued use of equity markets for capital raising.

- Bel Fuse provided earnings guidance for the second quarter of 2026, projecting sales between US$195 million and US$215 million and a gross margin of 38% to 40%, supported by bookings and demand from defense, commercial air, space, and data solutions customers.

- Bel Fuse reported that between January 1, 2026 and March 31, 2026 it repurchased 0 shares for US$0, while completing a total repurchase of 262,147 shares for US$16.05 million under the buyback announced on February 21, 2024.

- The company announced a realignment of its business units into two groups: Aerospace, Defense & Rugged Solutions and Industrial Technology & Data Solutions, aimed at organizing operations by end market and broadening customer access to its full product portfolio.

Valuation Changes for Bel Fuse

- Fair Value: $322.0 is unchanged from the prior estimate of $322, indicating no adjustment to the central valuation level.

- Discount Rate: 8.99% to 8.97% has fallen slightly, reflecting a modestly lower required return in the updated assumptions.

- Revenue Growth: 11.32% to 10.54% is now set slightly lower, pointing to more conservative expectations for future revenue expansion.

- Net Profit Margin: 18.58% to 17.61% has been trimmed slightly, implying a more cautious view on Bel Fuse's future earnings as a share of sales.

- Future P/E: 27.83x to 29.95x has risen moderately, suggesting the updated framework assumes a somewhat higher earnings multiple for Bel Fuse.

Key Takeaways

- Acquiring Enercon boosts Bel Fuse's diversification, strengthening growth in aerospace and defense, while shifting manufacturing from China to India optimizes margins.

- Cost reduction initiatives and growth in AI and defense markets enhance profitability, bolstering future revenue and earnings.

- Tariffs and geopolitical tensions threaten Bel Fuse's profitability and revenue, while declining sales and margin volatility signal potential challenges in maintaining growth.

Catalysts

About Bel Fuse- Designs, manufactures, markets, and sells products that power, protect, and connect electronic circuits.

- The recent acquisition of Enercon has diversified Bel Fuse’s end markets, especially in aerospace and defense (A&D), contributing $32.4 million to Power segment sales in Q1 '25. This diversification is poised to support future growth and revenue stability amidst market challenges.

- The company is strategically reducing its exposure to tariffs by moving some manufacturing operations from China to India, which could preserve or enhance net margins by mitigating increased costs associated with tariffs.

- Bel Fuse is implementing various cost reduction and efficiency programs, which have already improved gross margins in Q1 '25 by 110 basis points compared to Q1 '24. These operational efficiencies are expected to continue enhancing profitability.

- There is a strong growth trajectory in AI, defense, and space markets, with AI contributing $4.6 million in Q1 '25 sales. This trend is expected to drive revenue growth and bolster future earnings.

- The expansion of R&D and a proactive approach to supply chain adjustments amidst tariff concerns can enhance product competitiveness and operational resilience, potentially increasing future revenues and supporting long-term earnings growth.

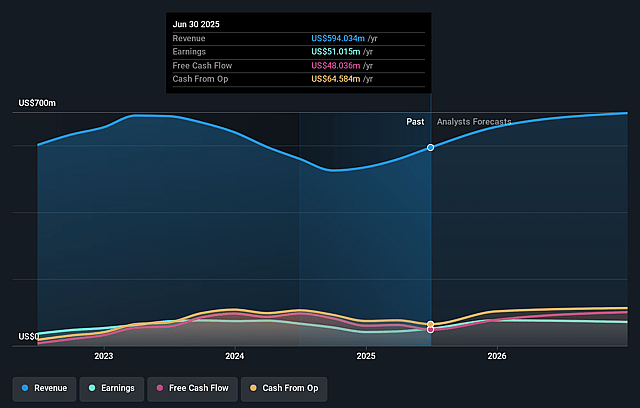

Bel Fuse Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Bel Fuse's revenue will grow by 10.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.8% today to 17.6% in 3 years time.

- Analysts expect earnings to reach $167.0 million (and earnings per share of $13.45) by about June 2029, up from $55.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.2x on those 2029 earnings, down from 69.9x today. This future PE is lower than the current PE for the US Electronic industry at 32.9x.

- Analysts expect the number of shares outstanding to grow by 0.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.97%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Global tariffs are posing new challenges for Bel Fuse, potentially affecting the cost structure and profitability due to higher import costs on approximately 25% of their consolidated sales, impacting net margins.

- The company faces a decrease in sales in their networking, consumer, rail, and e-mobility markets, possibly indicating a declining demand in those segments, which could negatively impact revenue.

- A decline in gross margins within their Power segment, largely due to the absence of nonrecurring items recorded at a 100% margin in Q1 2024, suggests potential volatility in profit margins going forward.

- Tariff-related uncertainties are leading to customer hesitance on orders and potential revenue push-outs, particularly related to products imported from China, which could impact revenue in the near term.

- Increased geopolitical tensions and trade disputes are driving an urgent need for supplier diversification and regional sourcing strategies, adding execution risk to operations and potentially affecting earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $322.0 for Bel Fuse based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $947.9 million, earnings will come to $167.0 million, and it would be trading on a PE ratio of 32.2x, assuming you use a discount rate of 9.0%.

- Given the current share price of $270.52, the analyst price target of $322.0 is 16.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bel Fuse?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.