Last Update 23 Jun 26

IRT: Dividend Hike And Buybacks Will Support Future Upside Potential

Analysts have maintained their price target for Independence Realty Trust at $19.14, reflecting only minor adjustments to assumptions regarding the discount rate, revenue growth, profit margins and future P/E ratio that did not materially change their overall valuation view.

What’s in the News for Independence Realty Trust

- Independence Realty Trust completed a follow on equity offering totaling $106.8 million in common stock across several tranches. These included 1,500,000 shares at an average price of about $19.73, 998,300 shares at about $21.04, and 2,681,600 shares at $20.96 with a $0.3144 per share discount, as part of an at the market offering.

- The company’s board approved a quarterly dividend of $0.18 per share of common stock, a 5.9% increase from the prior $0.17 per share rate. The second quarter 2026 dividend is payable on July 17, 2026 to shareholders of record on June 26, 2026.

- Independence Realty Trust reported that from January 1, 2026 to March 31, 2026 it repurchased 1,839,460 shares for $30.65 million. This brought total repurchases under the May 18, 2022 buyback authorization to 3,712,144 shares for $60.61 million.

- The company affirmed its full year 2026 earnings guidance, indicating an expected earnings per share range of $0.21 to $0.28.

Valuation Changes for Independence Realty Trust

- Fair Value: The assessed fair value remains unchanged at $19.14 per share, indicating no material shift in the core valuation estimate for Independence Realty Trust.

- Discount Rate: The discount rate has risen slightly from 7.65% to about 7.66%, reflecting a very small adjustment to the required rate of return used in the valuation model.

- Revenue Growth: Assumed long term revenue growth has edged down slightly from about 2.11% to about 2.09%, a marginal change in the projected growth profile.

- Net Profit Margin: The projected profit margin has eased slightly from about 4.06% to about 4.05%, indicating a very small adjustment in expected profitability.

- Future P/E: The future P/E assumption has risen slightly from about 197.0x to about 197.7x, suggesting only a minimal change in the multiple applied to Independence Realty Trust’s projected earnings.

Key Takeaways

- Strong Sun Belt demand, technology adoption, and strategic asset recycling support higher occupancy, improved margins, and resilient revenue growth in multifamily rentals.

- Elevated homeownership barriers extend renter tenure, reinforcing long-term pricing power, stable cash flows, and enhanced earnings potential.

- Persistent oversupply, competitive pressures, and reliance on asset sales create uncertainty for revenue growth, margin stability, and long-term earnings potential in core markets.

Catalysts

About Independence Realty Trust- Independence Realty Trust, Inc. (NYSE: IRT) is a real estate investment trust that owns and operates multifamily communities, across non-gateway U.S.

- The tapering of new multifamily supply and a 43% year-over-year reduction in deliveries projected for IRT's Sun Belt-focused markets in 2026 positions the company for a reacceleration of rent growth and stronger occupancy as demand continues to outpace incoming inventory, which should drive future revenue and NOI growth.

- Sustained strong demographic tailwinds-including millennial and Gen Z household formation and Sun Belt migration-are reflected in rising lead and tour volumes and high retention rates, supporting expectations for high occupancy and steady rent roll, which directly underpin future top-line revenue and stabilized net operating margins.

- Ongoing capital recycling-selling older, higher CapEx assets to acquire newer, lower CapEx communities with higher growth profiles in high-demand regions-allows IRT to enhance portfolio quality, capture operating synergies, and improve overall net margins and earnings growth potential.

- Accelerated implementation of technology, such as AI-driven leasing tools and market cluster acquisitions in Orlando, is delivering expense efficiencies and scale-driven operating synergies, which will lower G&A and property management costs, enhancing operating margins and supporting long-term FFO per share growth.

- High affordability barriers for single-family homeownership, underpinned by elevated home prices and mortgage rates, continue to extend renter tenure and bolster demand for mid-market multifamily rentals, strengthening IRT's pricing power and cash flow visibility, positively impacting future revenue stability and earnings resilience.

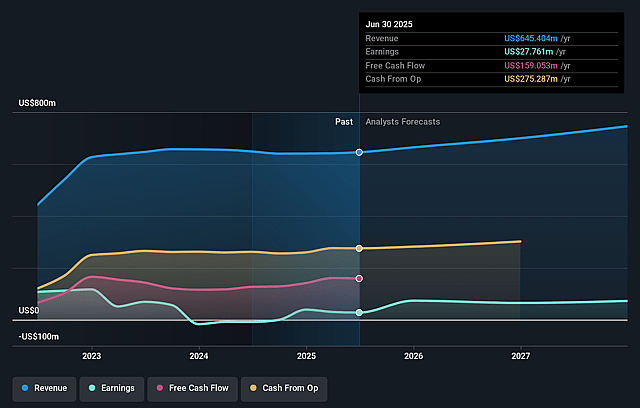

Independence Realty Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Independence Realty Trust's revenue will grow by 2.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 7.2% today to 4.1% in 3 years time.

- Analysts expect earnings to reach $29.0 million (and earnings per share of $0.11) by about June 2029, down from $48.1 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 198.5x on those 2029 earnings, up from 78.3x today. This future PE is greater than the current PE for the US Residential REITs industry at 30.0x.

- Analysts expect the number of shares outstanding to grow by 0.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.66%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing and unexpected oversupply in key Sun Belt markets such as Dallas, Denver, and Charlotte is leading to negative new lease trade-outs and suppressed rent growth, which directly pressures revenue and net operating income (NOI).

- Aggressive leasing concessions from new Class A apartment deliveries are attracting tenants away from IRT's predominantly Class B portfolio, making it harder to push rents and increasing the risk of stagnating or declining earnings growth.

- Reliance on disposing older, higher CapEx assets to fund acquisitions poses a risk if market conditions change or if projected accretive acquisitions underperform, which could lead to lower returns on invested capital and potentially compress margins.

- Lower-than-expected revenue growth, even as expense reductions have helped offset this in the near term, indicates underlying softness that could reverse if operating costs begin to rise again or if supply pressures persist, constraining long-term earnings power.

- Delays or inaccuracies in supply forecasts-such as deliveries being pulled forward into current periods-signal that IRT's core growth markets may continue to face volatility, making sustained blended rent growth and occupancy improvement less predictable and putting medium

- to long-term revenue and FFO-per-share growth at risk.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.14 for Independence Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $17.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $715.4 million, earnings will come to $29.0 million, and it would be trading on a PE ratio of 198.5x, assuming you use a discount rate of 7.7%.

- Given the current share price of $16.01, the analyst price target of $19.14 is 16.4% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Independence Realty Trust?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.