Catalysts

About Century Aluminum

Century Aluminum produces primary aluminum through smelters in the U.S., Iceland and interests in alumina refining.

What are the underlying business or industry changes driving this perspective?

- The outage at Grundartangi Line 2 and the 11 to 12 month repair window leave Century exposed to prolonged operational risk at a key smelter, so any delays, technical issues with repaired transformers or insurance disputes could pressure shipments and earnings beyond what current pricing assumes.

- The plan to restart more than 50,000 tonnes at Mt. Holly and the proposed U.S. greenfield smelter both rely heavily on current power arrangements and supportive policy. Any change in power pricing, delays in permitting or weaker counterparties could weigh on project returns and future EBITDA.

- The business increasingly leans on Section 45X tax credits and Section 232 tariffs to support cash generation. Policy revisions, timing slippage on remaining 45X receivables or any adjustment to tariff structures could materially affect net margins and free cash flow.

- The tight U.S. and European aluminum markets and elevated regional premiums currently support strong realized pricing. New supply from restarts, greenfield capacity or import shifts could reduce premiums and put pressure on revenue and adjusted EBITDA once contractual protections roll off.

- The large pipeline of capital projects, including Mt. Holly expansion, ongoing Jamalco investment and potential Hawesville or greenfield spend, raises execution and cost overrun risk. This could dilute returns, slow the path toward the US$300 million net debt target and constrain future earnings growth.

Assumptions

This narrative explores a more pessimistic perspective on Century Aluminum compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Century Aluminum's revenue will grow by 9.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.2% today to 19.9% in 3 years time.

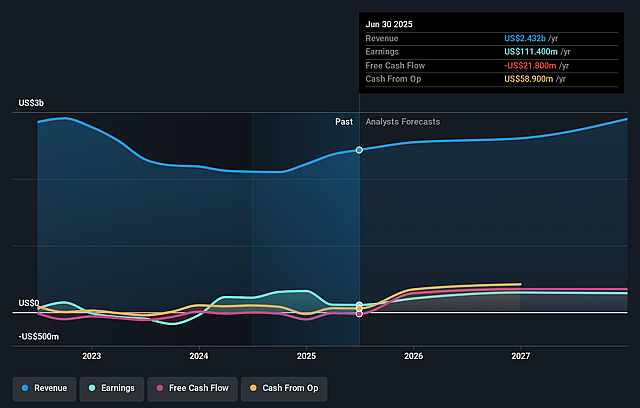

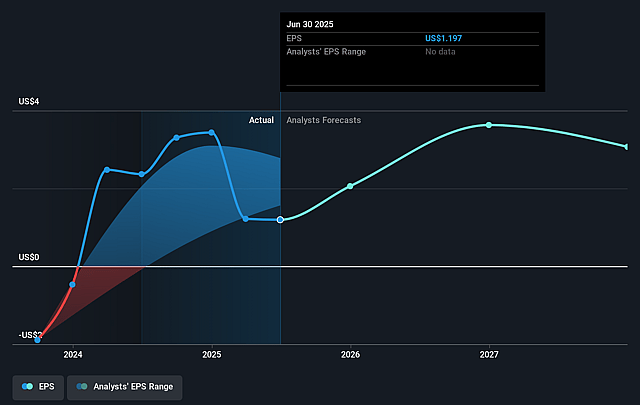

- The bearish analysts expect earnings to reach $659.1 million (and earnings per share of $6.68) by about January 2029, up from $80.8 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $967.9 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 6.9x on those 2029 earnings, down from 55.4x today. This future PE is lower than the current PE for the US Metals and Mining industry at 27.8x.

- The bearish analysts expect the number of shares outstanding to grow by 1.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.45%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Century is planning to restart more than 50,000 tonnes per year at Mt. Holly, with total project spend of about US$50 million. Management discussed the potential for this additional volume to contribute roughly US$25 million of EBITDA per quarter at current spot prices, which could support higher revenue and earnings if execution and power costs remain on track.

- The company is progressing a new U.S. greenfield smelter that it expects to be among the most modern and efficient in the industry. Management highlighted strong interest from potential joint venture partners, which could increase long term production scale and support revenue and EBITDA if the project proceeds on economic terms.

- Section 232 tariffs and Section 45X tax credits currently support the U.S. aluminum industry and Century specifically, with US$220 million of 45X receivables recorded as of 30 September 2025 and a US$75 million 2024 refund already received in October. These items could help reduce net debt toward the US$300 million target and support future earnings resilience if these policies remain in place.

- Management described global aluminum markets as tight, with low inventories, strong demand in the U.S. and Europe, higher LME prices and rising regional premiums. They indicated that these conditions are supporting Q4 2025 adjusted EBITDA guidance of US$170 million to US$180 million, so continued strong market pricing could sustain or expand revenue and margins rather than weaken them.

- Century reported Q3 2025 net sales of US$632 million, adjusted EBITDA of US$101 million and improving liquidity of US$488 million. The company is openly discussing potential future share buybacks once it reaches its net debt target, which could signal confidence in long term cash generation and support earnings per share.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Century Aluminum is $37.0, which represents up to two standard deviations below the consensus price target of $45.0. This valuation is based on what can be assumed as the expectations of Century Aluminum's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $52.0, and the most bearish reporting a price target of just $37.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $3.3 billion, earnings will come to $659.1 million, and it would be trading on a PE ratio of 6.9x, assuming you use a discount rate of 8.4%.

- Given the current share price of $47.92, the analyst price target of $37.0 is 29.5% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Century Aluminum?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.