Catalysts

About Taylor Morrison Home

Taylor Morrison Home is a U.S. homebuilder focused on entry level, move up and resort lifestyle buyers, along with single family rental communities through its Yardly platform.

What are the underlying business or industry changes driving this perspective?

- While a large and well located lot position and an increasing share of controlled, off balance sheet land can support long term community growth, a cautious approach to new land investment and deal deferrals may limit the number of higher margin new projects flowing into the portfolio, which can cap revenue and gross margin expansion.

- Although the Premier Esplanade resort lifestyle brand benefits from an affluent customer base and a growing pipeline of new communities, reliance on discretionary buyers that are sensitive to confidence and amenity delivery timing could lead to uneven order patterns and margin mix, affecting earnings consistency.

- Despite cycle times improving by about 90 days over two years and around 30 days over the last year, further gains are described as incremental, so the bulk of efficiency benefits may already be realized, which can limit additional help for gross margin and earnings from construction savings.

- While the Yardly build to rent platform and the US$3b financing facility introduce capital efficient growth in single family rental, greater use of off balance sheet structures and land banking also brings higher interest expense, as seen in the move from US$3 million to US$13 million of net interest expense year on year in the quarter, which can weigh on net margins if not offset by pricing and volume.

- Although tech enabled sales tools such as the new AI powered digital assistant and the online reservation system are helping with cost efficiencies and lower broker commissions, competitive conditions and the need to keep incentives compelling, especially for entry level buyers, may absorb some of these savings and keep SG&A and gross margins from expanding meaningfully.

Assumptions

This narrative explores a more pessimistic perspective on Taylor Morrison Home compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

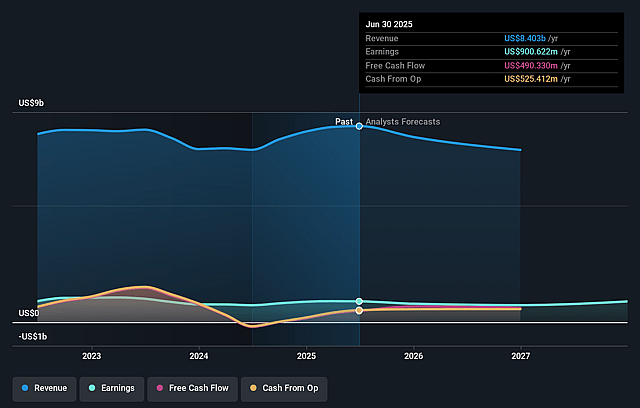

- The bearish analysts are assuming Taylor Morrison Home's revenue will decrease by 9.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 10.2% today to 11.3% in 3 years time.

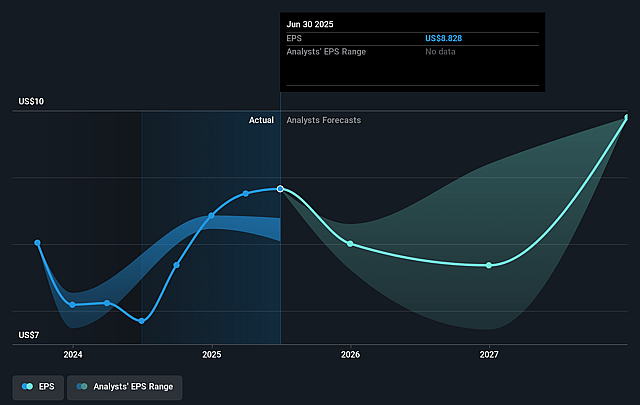

- The bearish analysts expect earnings to reach $710.1 million (and earnings per share of $5.66) by about January 2029, down from $850.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.9x on those 2029 earnings, up from 7.1x today. This future PE is lower than the current PE for the US Consumer Durables industry at 11.3x.

- The bearish analysts expect the number of shares outstanding to decline by 3.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.47%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- A large pipeline of more than 100 new communities expected to open next year and mid to high single digit anticipated outlet growth in 2026 could support higher sales volumes than today. This would challenge the assumption that revenue and earnings stay flat.

- Cycle times are about 90 days faster than two years ago and roughly 30 days faster than a year ago, and management still sees room for further efficiency gains. This could support stronger home delivery volumes and cost savings and therefore put upward pressure on earnings and net margins.

- Renegotiated land deals covering roughly 3,400 lots and more than US$500m of purchase price, including an 8% average land price reduction and development cost relief, can support future project economics and help sustain or improve gross margins and returns over time.

- The Yardly build to rent platform, backed by a US$3b financing facility that shifts projects off balance sheet and frees more than US$190m of capital, may allow Taylor Morrison Home to scale an additional revenue stream with less capital intensity. This could support higher long run earnings and cash flow than implied by a flat share price view.

- Affluent Esplanade resort lifestyle buyers, a growing pipeline of new Esplanade communities scheduled to open in 2026 and continued population and net move in growth in key markets such as Florida and Texas can provide long term demand support for higher average selling prices and volumes, which could underpin growth in revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Taylor Morrison Home is $62.0, which represents up to two standard deviations below the consensus price target of $75.25. This valuation is based on what can be assumed as the expectations of Taylor Morrison Home's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $95.0, and the most bearish reporting a price target of just $62.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $6.3 billion, earnings will come to $710.1 million, and it would be trading on a PE ratio of 9.9x, assuming you use a discount rate of 9.5%.

- Given the current share price of $62.24, the analyst price target of $62.0 is 0.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Taylor Morrison Home?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.