Last Update 23 Jun 26

Fair value Increased 0.65%BJ: Q1 Margin Pressures And Membership Strength Will Shape 2026 Comp Outlook

The analyst price target for BJ's Wholesale Club Holdings has shifted modestly higher to reflect a fair value estimate of $80.43, with analysts pointing to mixed sector valuations, recent Q1 margin commentary, and expectations for a near term share price rebound after what they view as an overdone pullback.

Analyst Commentary

Recent Street research on BJ's Wholesale Club Holdings points to a more cautious tone, even as some firms keep positive or Neutral ratings in place. The key debate centers on how much near term margin pressure, tariff related effects, and sector wide valuation resets should weigh on what analysts view as the stock's fair value.

Several bearish analysts have trimmed their price targets after the latest Q1 update, with particular focus on merchandise margin commentary and the impact of tariff rebates. While one major bank, JPMorgan, has inched its target higher following what it describes as an overdone pullback and potential for a near term bounce, the broader tone of research has shifted toward balancing upside scenarios against execution and growth risks.

Across reports, analysts highlight that the recent Q1 beat was tied to better sales and lower spending, but they also flag higher freight costs and ongoing pricing investments as sources of pressure for future estimate revisions. In addition, some see lower sector valuations as a key reason to reset targets, rather than a company specific call on BJ's Wholesale Club Holdings alone.

Membership economics remain an important offset in many models, with one research note arguing that tariff rebates might have weighed on comparable sales due to lower pricing in relatively inelastic grocery categories, while potentially supporting longer term membership renewal value. Even so, several bearish analysts stress that the market may want clearer evidence of comp consistency and improvement before assigning higher valuation multiples to BJ's Wholesale Club Holdings.

Bearish Takeaways

- Bearish analysts have reduced price targets into the US$90 to US$105 range, citing weaker Q1 merchandise margin performance and lower sector valuations as reasons to reset expectations for BJ's Wholesale Club Holdings.

- Commentary that Q1 merchandise margins would have faced heavier pressure without tariff rebates has raised concerns about underlying profitability trends once those rebates normalize.

- Some research points to a challenging near term path for positive estimate revisions, given elevated freight costs and ongoing pricing investments that could constrain margin expansion.

- Several bearish analysts argue that for BJ's Wholesale Club Holdings to command higher valuation multiples, investors may need to see more consistent same store sales performance and clearer improvement in core operating metrics.

What’s in the News for BJ's Wholesale Club Holdings

- BJ's Wholesale Club reported Q1 revenue up 9.9% year over year, coming in 4.2% above analyst expectations, with management highlighting membership, fuel, and digital sales as key contributors to the quarter’s performance, according to recent earnings coverage.

- Despite the Q1 earnings beat, BJ's Wholesale Club stock edged slightly lower following the report, reflecting mixed market reaction to the results and guidance referenced in the same coverage.

- From February 1, 2026 to May 2, 2026, BJ's Wholesale Club repurchased 2,114,000 shares for US$206.6 million, completing a total of 4,713,000 shares repurchased for US$457.89 million under the buyback announced on November 21, 2024, according to company event disclosures.

- BJ's Wholesale Club outlined plans to open new clubs in Kentucky, Florida and Indiana this fiscal year as part of a broader plan to open 25 to 30 new clubs every two years. This includes 12 new clubs in the 2026 fiscal year and recent openings in Texas, based on company expansion announcements.

- The company is rolling out new clubs in multiple Texas locations, including Fort Worth, Grand Prairie, Waxahachie and Forney, with associated community partnerships and fuel promotions, according to recent company opening and expansion updates.

Valuation Changes for BJ's Wholesale Club Holdings

- Fair Value has been updated to $80.43 from $79.92, indicating a slight upward adjustment in the estimated share valuation.

- The Discount Rate is now 7.27% compared with 7.27% previously, reflecting a very small change in the risk assumption used in the model.

- Revenue Growth has been updated to 6.28% from 6.06%, pointing to a modestly higher growth assumption for BJ's Wholesale Club Holdings.

- Net Profit Margin is now 2.41% versus 2.45% previously, indicating a small reduction in expected profitability levels.

- Future P/E has been revised to 18.09x from 19.16x, reflecting a slightly lower valuation multiple applied to forward earnings estimates.

Key Takeaways

- BJ's faces competition from established players and may struggle with market share and revenue in new regions like Texas.

- Rising costs and tariff risks could pressure margins and profitability if not offset by price adjustments.

- BJ's strong sales, high membership renewal, and digital growth indicate potent revenue potential and successful expansion strategy for future market share gains.

Catalysts

About BJ's Wholesale Club Holdings- Operates membership warehouse clubs on the eastern half of the United States.

- BJ's expansion plans into new markets like Texas could face significant competition, potentially impacting their revenue and ability to capture market share, especially if consumer preferences lean towards established competitors like Costco and Sam's Club.

- Tariff risks and rising costs of key commodities could lead to increased pricing pressures. This may result in margin compression, affecting BJ's profitability if they are unable to fully pass these costs on to consumers.

- As BJ's continues to invest heavily in digital and real estate initiatives, capital expenditures are expected to rise to approximately $800 million. High investment levels without proportional revenue growth could impact net margins and result in less efficient earnings growth.

- The increase in membership fees and potential consumer backlash could offset the growth in membership fee income, especially if renewed interest in spending slows down or if members are sensitive to price changes, impacting overall earnings.

- The expected slowdown in comparable club sales growth to 2% to 3.5% from higher previous growth rates suggests possible revenue deceleration. This slowdown may not align with investor expectations, negatively affecting future earnings and stock valuation.

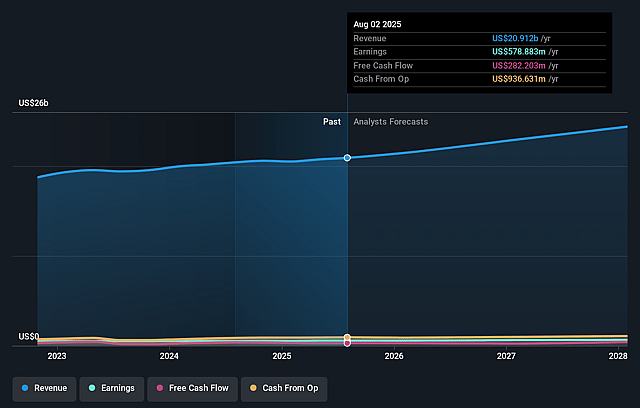

BJ's Wholesale Club Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on BJ's Wholesale Club Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming BJ's Wholesale Club Holdings's revenue will grow by 6.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 2.6% today to 2.4% in 3 years time.

- The bearish analysts expect earnings to reach $636.7 million (and earnings per share of $5.19) by about June 2029, up from $571.3 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $709.2 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.1x on those 2029 earnings, down from 18.7x today. This future PE is lower than the current PE for the US Consumer Retailing industry at 18.6x.

- The bearish analysts expect the number of shares outstanding to decline by 3.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.27%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- BJ's Wholesale Club Holdings achieved record net sales, membership, and adjusted earnings per share for fiscal 2024, indicating strong financial health and potential for future revenue and earnings growth.

- The company reported a 4.6% growth in comparable club sales excluding gas sales in the fourth quarter, driven by robust traffic and unit growth, which may sustain or improve revenue.

- Membership is at an all-time high with a 90% renewal rate, showcasing strong customer loyalty and potential for continued membership fee income growth.

- BJ's digital sales grew by 26% year-over-year in the fourth quarter, with 53% growth on a two-year stack, indicating significant revenue potential through enhanced digital engagement and convenience offerings.

- The company's aggressive expansion strategy, including the opening of new clubs and gas stations, might lead to increased market share and revenue generation across existing and new markets.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for BJ's Wholesale Club Holdings is $80.43, which represents up to two standard deviations below the consensus price target of $101.1. This valuation is based on what can be assumed as the expectations of BJ's Wholesale Club Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $120.0, and the most bearish reporting a price target of just $79.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $26.4 billion, earnings will come to $636.7 million, and it would be trading on a PE ratio of 18.1x, assuming you use a discount rate of 7.3%.

- Given the current share price of $83.82, the analyst price target of $80.43 is 4.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on BJ's Wholesale Club Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.