Last Update 13 Jun 26

Fair value Decreased 3.81%BCHN: Future Upside Will Depend On Record Margins Offsetting Weaker Orders

Analysts now see fair value for Burckhardt Compression Holding at about CHF 609, down from roughly CHF 634. This reflects updated assumptions around revenue growth, profit margins, the discount rate and a slightly lower future P/E multiple.

Analyst Commentary

Analysts are reassessing what they are willing to pay for earnings, which is feeding directly into the updated fair value of CHF 609 for Burckhardt Compression Holding. The change in assumptions around growth, profitability and the discount rate is similar to what has recently been seen in other stocks where targets have been reset without a clear shift in ratings.

Recent bank sector research, such as the opposing price target moves on Banco de Chile, highlights how different analysts can look at the same fundamentals and still reach different valuation conclusions. That tension between optimism and caution is also relevant for how to think about Burckhardt Compression Holding at the new fair value level.

Bullish Takeaways

- Bullish analysts typically focus on execution and balance sheet quality when supporting valuations, and a fair value near CHF 609 still implies confidence that earnings can support a relatively full P/E multiple over time.

- Where targets in other stocks have been cut without a change in rating, it often reflects fine tuning of models rather than a major shift in conviction, which can be the case here as assumptions on revenue, margins and discount rate are adjusted rather than overhauled.

- Updated models that still support a premium to more cautious scenarios suggest that bullish analysts see room for Burckhardt Compression Holding to justify higher earnings power if it delivers on its operational plans.

- The willingness to maintain constructive views even as targets move reflects a belief that, for patient investors, execution on current projects can still back up the revised valuation framework.

Bearish Takeaways

- Bearish analysts are likely to point to the cut in fair value from roughly CHF 634 to CHF 609 as evidence that prior expectations for revenue growth and profit margins were ambitious relative to updated assumptions.

- A slightly lower future P/E multiple in the models signals some caution around how much investors may eventually pay for each franc of earnings, especially if results stay closer to base case than to optimistic scenarios.

- The need to adjust the discount rate reminds investors that changes in funding costs or perceived risk can quickly affect valuation, even when the underlying business story is unchanged.

- Compared with more optimistic stances, bearish analysts may argue that the recent reset leaves less room for error, so any shortfall in execution or profitability could put further pressure on the fair value estimate.

What's in the News

- Burckhardt Compression Holding reported record operating income of CHF 141 million and net income of CHF 110 million for fiscal year 2026, with an EBIT margin of 13.3% (source: company results, 4 Jun 2026).

- Order intake declined 32% year on year, with management linking the drop to market disruptions, deferred projects in China and the US, and geopolitical uncertainties (source: company results, 4 Jun 2026).

- The company expanded its global service network by opening nine new locations, aiming to strengthen service coverage for its installed base (source: company results, 4 Jun 2026).

- Burckhardt Compression completed acquisitions to build out its service offerings and continues to reference long term growth targets supported by ongoing M&A and global megatrends (source: company results, 4 Jun 2026).

- Guidance for fiscal year 2026 indicates group sales between CHF 900 million and CHF 1 billion and an EBIT margin around 12%, with management highlighting expectations for stronger sales in the second half due to project delivery timing (source: company guidance, 2026).

Valuation Changes

- Fair Value: revised slightly lower from CHF 633.5 to CHF 609.3, reflecting updated model inputs.

- Discount Rate: adjusted modestly lower from 5.45% to 5.34%, which has a direct effect on the present value of projected cash flows.

- Revenue Growth: moved from a prior forecast of a 0.29% decline to a 0.61% increase, indicating a more constructive view on top line trends in the model.

- Net Profit Margin: raised from 9.94% to 11.01%, pointing to higher assumed profitability on each CHF of revenue.

- Future P/E: reduced from 20.39x to 18.02x, suggesting a more cautious stance on how much investors may pay for future earnings in the valuation work.

Key Takeaways

- Sustained demand for clean energy, LNG, and marine infrastructure drives robust order growth, strong revenue streams, and high-margin service opportunities for Burckhardt Compression.

- Digital services, operational improvements, and a growing installed base support margin expansion, recurring revenues, and long-term profitability.

- Reliance on cyclical segments, market headwinds in China, rising credit risk, and macroeconomic uncertainties threaten revenue growth, margin stability, and earnings visibility.

Catalysts

About Burckhardt Compression Holding- Manufactures and sells reciprocating compressor technologies worldwide.

- Growing demand for cleaner energy and decarbonization is accelerating global investments in hydrogen, LNG, and alternative fuels infrastructure, supporting long-term order growth for Burckhardt's advanced compression solutions

- likely to boost topline revenues and the services backlog over the next several years.

- Expansion of natural gas and LNG supply chains, particularly in the US, Middle East, and emerging markets, is driving new marine and transportation compressor orders; sustained high order intake for LPG/LNG tankers and related services is expected to support revenue visibility and margin stability.

- Increased delivery of large, long-life compressors is steadily building a substantial installed base, which will drive a higher proportion of recurring, high-margin aftermarket service and digital solution revenues starting in 2026 and beyond, improving net margins and earnings predictability.

- Investments in digital services (like UP! Detect and integration of PROGNOST) position Burckhardt to capture value from the digitalization trend in industrial equipment, differentiating the firm and enabling new, higher-margin service revenue streams that enhance long-term profitability.

- Operational leverage from productivity initiatives (Fit4Growth, factory expansions, and supply chain flexibility) allows for revenue growth without significant increases in fixed costs, supporting continued EBIT margin expansion and strong capital returns as global energy and industrial trends play out.

Burckhardt Compression Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

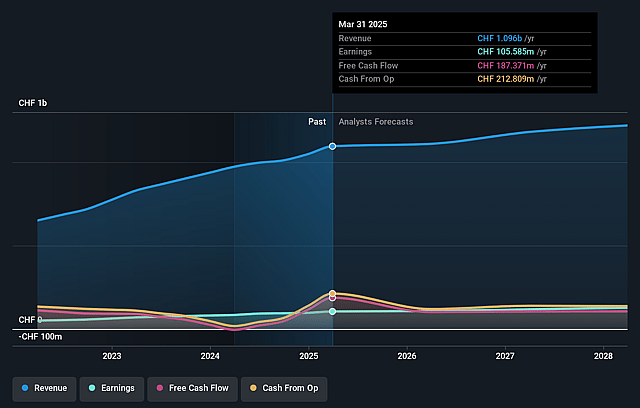

- Analysts are assuming Burckhardt Compression Holding's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 10.4% today to 11.0% in 3 years time.

- Analysts expect earnings to reach CHF 118.6 million (and earnings per share of CHF 33.57) by about June 2029, up from CHF 110.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 20.1x on those 2029 earnings, up from 14.0x today. This future PE is lower than the current PE for the GB Machinery industry at 24.1x.

- Analysts expect the number of shares outstanding to decline by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing normalization and potential decline of demand in key segments, such as petrochemicals (solar-related Hyper Compressors) and a recalibrated hydrogen market, suggest mid-term order intakes could decrease, putting pressure on future revenue growth and earnings visibility.

- Increased push for localization and self-reliance in China presents a structural headwind, risking erosion of Burckhardt's market share and limiting pricing power in its largest regional market-potentially impacting both top-line revenues and net margins.

- High dependence on cyclical, large-scale projects and certain high-margin subsegments (e.g., LPG marine, solar-linked Hyper) exposes the company to backlog volatility, project deferrals, and execution risks, leading to possible swings in revenue, cash flow, and earnings.

- Rising overdue receivables (over 90 days) more than doubling year-on-year-in markets like China and India-alongside the need for increasing bad debt provisions, indicates heightened credit risk and may compromise net income and margin stability.

- Exposure to indirect macro headwinds like US tariffs, currency fluctuations (particularly Swiss franc appreciation), and slower GDP growth in key markets adds uncertainty to future demand, price competitiveness, and cost structure, with negative consequences for both revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF609.33 for Burckhardt Compression Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF700.0, and the most bearish reporting a price target of just CHF505.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CHF1.1 billion, earnings will come to CHF118.6 million, and it would be trading on a PE ratio of 20.1x, assuming you use a discount rate of 5.3%.

- Given the current share price of CHF458.0, the analyst price target of CHF609.33 is 24.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Burckhardt Compression Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.