Last Update01 May 25Fair value Increased 0.37%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- Investment in Neoen and asset recycling enhances position in grid stability and profitability, supporting revenue growth and margin expansion.

- Landmark agreement with Microsoft and strategic liquidity usage set the stage for stable, long-term earnings and growth opportunities.

- Regulatory uncertainties in the U.S. renewable sector could impact Brookfield Renewable's project timelines, revenue growth, and capital-raising capabilities.

Catalysts

About Brookfield Renewable- Owns and operates a portfolio of renewable power and sustainable solution assets.

- The AI revolution is driving a dramatic increase in electricity demand, which positions Brookfield Renewable to capitalize on new growth opportunities, potentially boosting revenue.

- Brookfield Renewable's investment in Neoen, a leading global renewable platform and battery energy storage systems operator, positions them to benefit from increasing demand for grid stability solutions and potentially higher margins from storage solutions.

- The landmark renewable energy agreement with Microsoft for 10.5 gigawatts of new capacity between 2026 and 2030 could significantly increase future revenues and secure stable cash flows.

- Asset recycling activities, with high returns on invested capital, provide additional revenue and liquidity to fund growth, positively impacting net margins and supporting profitable expansion.

- Strong balance sheet and significant liquidity (over $4.3 billion) enable opportunistic investments and acquisitions at attractive valuations, likely driving earnings growth.

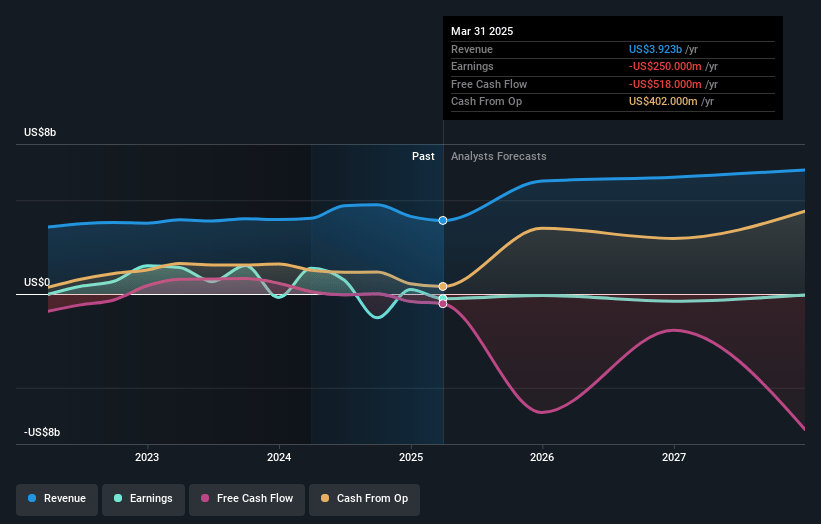

Brookfield Renewable Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Brookfield Renewable's revenue will grow by 13.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 5.2% today to 0.4% in 3 years time.

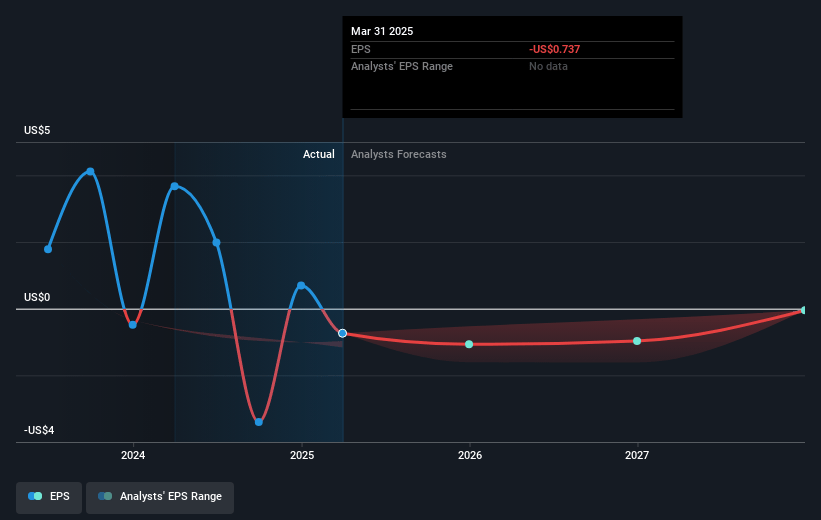

- Analysts expect earnings to reach $26.6 million (and earnings per share of $1.77) by about May 2028, down from $236.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $240.9 million in earnings, and the most bearish expecting $-187.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 430.7x on those 2028 earnings, up from 41.4x today. This future PE is greater than the current PE for the US Renewable Energy industry at 31.8x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.15%, as per the Simply Wall St company report.

Brookfield Renewable Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Elevated volatility in public markets due to uncertainty on potential regulatory changes affecting the renewable sector in the U.S., which could impact investment sentiment and valuation, ultimately affecting earnings.

- The supply-demand imbalance and permitting bottlenecks mean the pace of development may not keep up with demand, potentially affecting future revenue from new projects.

- While Brookfield Renewable is not extensively exposed to U.S. wind projects on federal land, regulatory uncertainties in permitting could delay projects, affecting revenue growth and project timelines.

- The threat of changes to U.S. tax credits (PTCs and ITCs) could impact the financial models for new developments, potentially leading to higher required PPA prices to maintain margins, affecting contracted revenue.

- The market bifurcation between private and public investments could limit funding and growth in the public markets, impacting the company's capital-raising ability and future acquisition or development plans that drive revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.333 for Brookfield Renewable based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.7 billion, earnings will come to $26.6 million, and it would be trading on a PE ratio of 430.7x, assuming you use a discount rate of 8.1%.

- Given the current share price of $28.8, the analyst price target of $33.33 is 13.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.