Narratives are currently in beta

Key Takeaways

- Investments in technology and strategic hub focus aim to enhance customer experience and operational efficiency, supporting revenue and margin growth.

- International and loyalty program expansions are set to capitalize on global travel recovery, potentially improving revenue and margins.

- Staffing challenges and OEM delays, combined with inflation and competitive pressures, could affect operational efficiency, margin stability, and future growth.

Catalysts

About United Airlines Holdings- Through its subsidiaries, provides air transportation services in North America, Asia, Europe, Africa, the Pacific, the Middle East, and Latin America.

- United Airlines has been investing heavily in technological advancements, such as Starlink and app enhancements, which are expected to improve customer experience and operational efficiency, potentially boosting revenue and margins.

- The airline's strategic focus on its hubs, particularly in building connectivity and gauge improvements, provides opportunities for margin expansion and revenue growth in its core markets.

- United's international strategy, including doubling down on international markets and optimizing Pacific and Atlantic routes, positions it for stronger margins and revenue growth as global travel demands recover.

- The company's focus on its MileagePlus and loyalty programs, alongside expansion in Basic Economy and premium offerings, can drive incremental revenue and margin improvements.

- United's disciplined approach to fleet management and capacity deployment, despite delivery delays, is expected to drive gauge improvements and cost efficiencies, benefiting margins in the coming years.

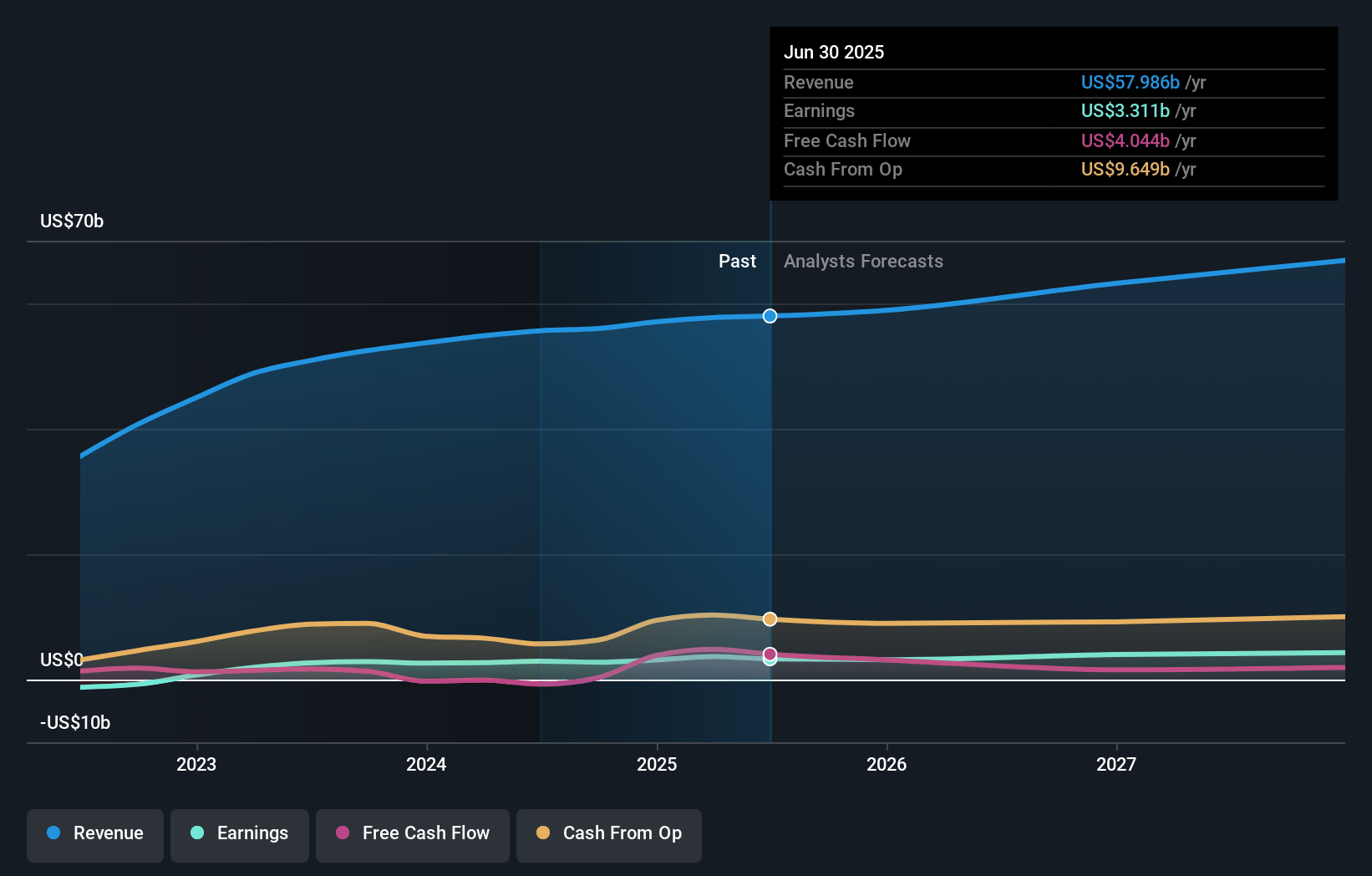

United Airlines Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming United Airlines Holdings's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.5% today to 6.9% in 3 years time.

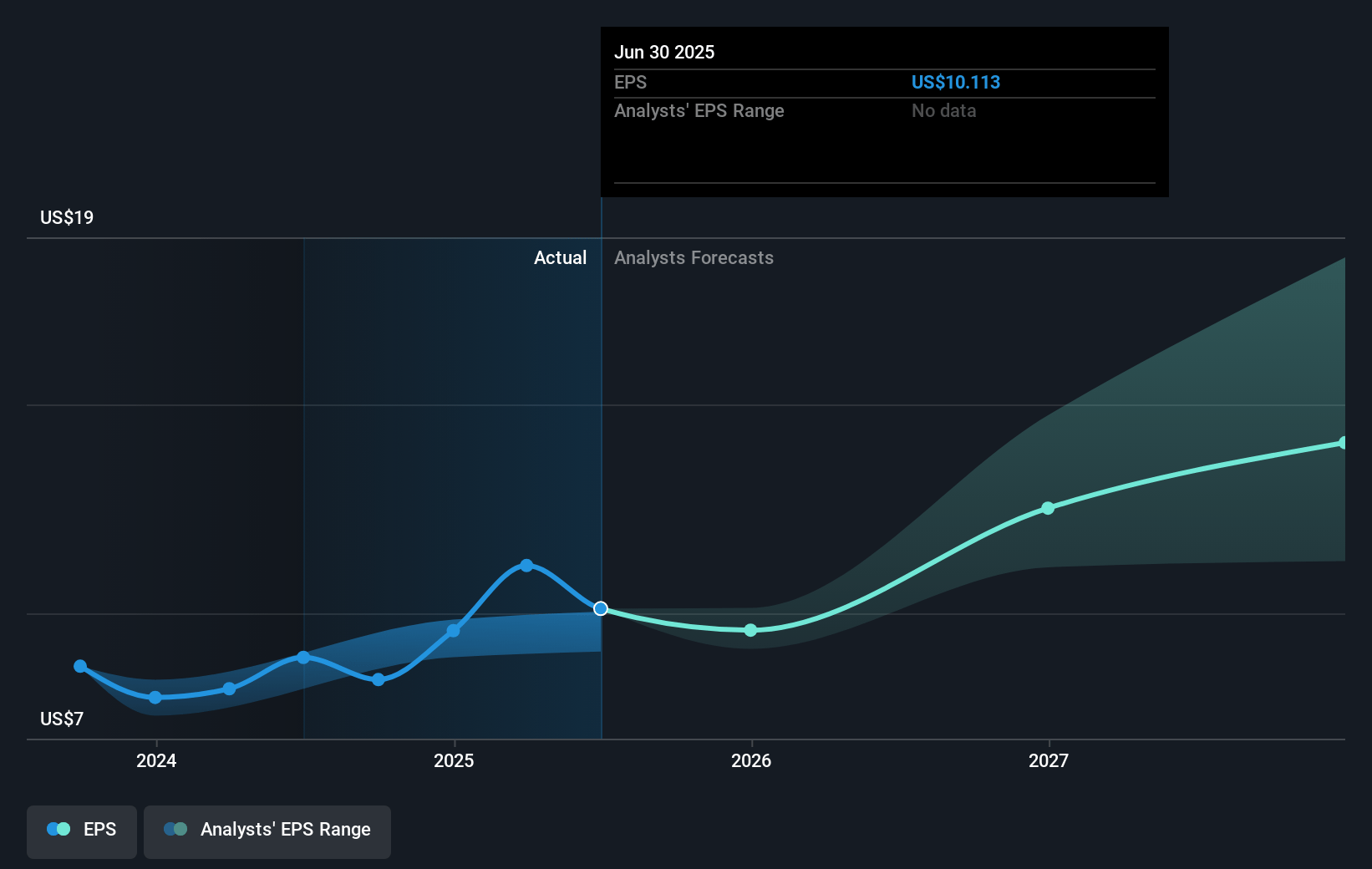

- Analysts expect earnings to reach $4.7 billion (and earnings per share of $14.83) by about January 2028, up from $3.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $5.5 billion in earnings, and the most bearish expecting $3.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.2x on those 2028 earnings, up from 11.1x today. This future PE is lower than the current PE for the US Airlines industry at 12.5x.

- Analysts expect the number of shares outstanding to decline by 1.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.72%, as per the Simply Wall St company report.

United Airlines Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The persistent staffing challenges at the FAA, leading to significant delays, could negatively impact operational efficiency and increase costs, thereby affecting net margins and earnings.

- OEM production delays impacting aircraft deliveries could constrain capacity growth and alter capital expenditure plans, potentially affecting future revenue growth and free cash flow.

- The significant inflationary pressures on labor and other operational costs could erode profit margins if not fully passed on to customers, affecting net earnings.

- The competitive landscape and structural changes in capacity deployment, particularly by low-cost carriers pivoting strategies, could pressure pricing and revenue if not managed effectively.

- The geopolitical and macroeconomic uncertainties around trade, tariffs, and economic growth could impact international revenue streams and overall demand for air travel, influencing future earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $129.5 for United Airlines Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $165.0, and the most bearish reporting a price target of just $39.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $68.2 billion, earnings will come to $4.7 billion, and it would be trading on a PE ratio of 11.2x, assuming you use a discount rate of 8.7%.

- Given the current share price of $106.34, the analyst's price target of $129.5 is 17.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives