Last Update 29 May 26

SBLK: Future Returns Will Hinge On Dry Bulk Conditions And Capital Returns

Analysts have increased their average price target on Star Bulk Carriers to $32 from $31, citing an improving dry bulk market following the Q1 earnings beat as the primary driver for the change.

Analyst Commentary

Recent research points to a more constructive tone on Star Bulk Carriers, with the latest published target of US$32 framed around an improving dry bulk market following the Q1 earnings beat. Earlier reports also referenced upbeat initiation commentary and prior target changes, signaling active reassessment of the stock as new data comes through.

While some readers may see the US$32 target as a directional marker, it is better viewed as one input among many, especially as opinions across the Street can vary based on assumptions around freight demand, fleet utilization, and capital allocation.

Bearish Takeaways

- Bearish analysts may question whether current forecasts already bake in optimistic assumptions around dry bulk conditions following the Q1 results, which could limit upside if spot rates or volumes do not match expectations.

- Some cautious views are likely to focus on execution risk, including the ability to sustain earnings performance if charter rates soften or if operating costs trend higher.

- Valuation concerns may arise if investors push the stock to levels that assume continued strength in earnings without a clear buffer for weaker quarters or unforeseen disruptions in shipping demand.

- Growth oriented investors may see risk in the pace and timing of any fleet expansion or renewal, especially if new capacity is added into a less favorable freight market, which could weigh on returns.

What's in the News

- Star Bulk Carriers Corp. declared a quarterly dividend of US$0.50 per share, with an ex-date and record date of June 12, 2026, and payment scheduled for June 22, 2026 (Key Developments).

Valuation Changes

- Fair Value: $25.90 is unchanged, with the latest update matching the prior estimate of $25.90.

- Discount Rate: has fallen slightly from 10.50% to 10.22%, reflecting a modest shift in the required return used in the model.

- Revenue Growth: is projected to decline more sharply, moving from a 2.05% decline to a 3.72% decline in the updated assumptions.

- Net Profit Margin: has risen slightly from 36.15% to 37.22%, pointing to a small uplift in expected profitability on each dollar of revenue.

- Future P/E: has moved slightly higher from 9.57x to 9.74x, indicating a modest increase in the earnings multiple applied to the stock.

Key Takeaways

- Decarbonization trends and supply chain localization threaten core revenue streams, shrinking Star Bulk's market and pressuring growth prospects.

- An aging fleet and slow modernization risk higher operating costs and reduced competitiveness, magnifying profitability challenges and hurting long-term returns.

- Cost synergies, fleet modernization, and reduced debt position Star Bulk for improved profitability and competitiveness as tighter regulations and modest industry growth support freight rates.

Catalysts

About Star Bulk Carriers- A shipping company, engages in the ocean transportation of dry bulk cargoes through the ownership and operation of dry bulk carrier vessels worldwide.

- The accelerating global shift toward decarbonization and energy transition is set to steadily erode long-term demand for seaborne transportation of coal, iron ore, and other fossil fuel-related cargoes, which represent a significant portion of Star Bulk Carriers' revenues. This secular decline in core cargo volumes is likely to suppress top-line growth and lead to recurring pressure on long-term company revenue.

- Major economies are increasingly prioritizing localized manufacturing and supply chain resiliency, reflected in policy shifts toward nearshoring and reshoring production. As a result, the addressable market for global seaborne bulk trade is likely to shrink structurally, leading to reductions in vessel utilization rates and day rates, which will negatively impact Star Bulk's revenue and earnings power over the next decade.

- Star Bulk's aging fleet, with an average age of nearly 12 years, faces escalating capital expenditure requirements for retrofitting or replacement to comply with tightening environmental regulations. As the International Maritime Organization introduces stricter greenhouse gas emissions targets and fuel intensity standards, recurring high CapEx and increased depreciation will depress operating margins and erode long-term return on assets.

- Heavy reliance on global commodity cycles exposes Star Bulk to volatility in freight rates and charter markets. With projected contractions in bulk trade volumes for iron ore, coal, and grains in the coming years, combined with persistent overcapacity in the dry bulk shipping sector due to sluggish demolition of older vessels, there is a severe risk of suppressed profitability and earnings through recurring market downturns.

- Anticipated ramp-up of digitalization and operational efficiency among competitors, coupled with adoption of larger, more fuel-efficient vessels industrywide, could outpace Star Bulk's current fleet renewal efforts and push operating costs higher relative to peers. This competitive disadvantage will compress margins and erode Star Bulk Carriers' earnings unless dramatic reinvestment occurs, which would further pressure free cash flow and long-term shareholder returns.

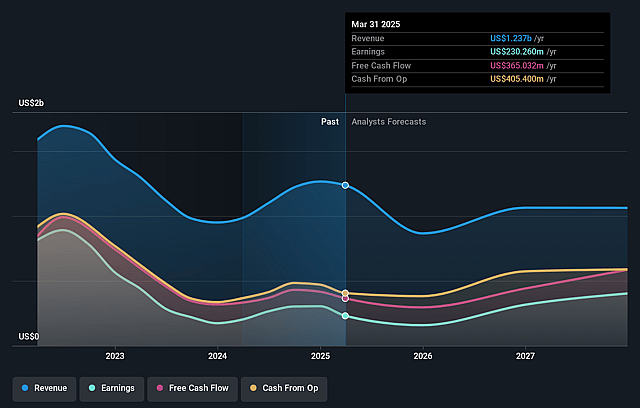

Star Bulk Carriers Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Star Bulk Carriers compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Star Bulk Carriers's revenue will decrease by 3.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 13.0% today to 37.2% in 3 years time.

- The bearish analysts expect earnings to reach $363.1 million (and earnings per share of $3.27) by about May 2029, up from $142.2 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $653.1 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.8x on those 2029 earnings, down from 21.3x today. This future PE is lower than the current PE for the US Shipping industry at 12.1x.

- The bearish analysts expect the number of shares outstanding to decline by 2.63% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company has achieved nearly $40 million in cost synergies from the Eagle Bulk integration, with significant reductions in operating expenses, dry dock costs, and interest expenses, which are likely to support profitability and net margins even in a challenging market environment.

- Star Bulk has been actively deleveraging, reducing its average net debt per vessel by over 50% since 2021 and now holds a net debt position covered by fleet scrap value, greatly strengthening its balance sheet and lowering financial risk, which supports future earnings and dividends.

- The company is modernizing its fleet by disposing less efficient, older vessels and investing in new eco-friendly ships and energy-saving retrofits, a strategy that should enhance fleet efficiency, reduce operating costs, and help safeguard future net margins and vessel utilization as regulations tighten.

- Supply discipline in the industry is evident, with the global order book at multi-year lows, high newbuilding costs, uncertainty around future fuel technologies, and limited shipyard capacity, all of which are expected to keep fleet growth modest and tighten supply-demand balance, providing potential upside to vessel charter rates and Star Bulk's revenue.

- Regulatory changes, such as the new IMO greenhouse gas fuel intensity metric and stricter emission targets, may incentivize slow steaming and support higher freight rates for compliant operators like Star Bulk, giving them a competitive advantage and potentially boosting long-term revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Star Bulk Carriers is $25.9, which represents up to two standard deviations below the consensus price target of $30.98. This valuation is based on what can be assumed as the expectations of Star Bulk Carriers's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $33.0, and the most bearish reporting a price target of just $25.9.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $975.4 million, earnings will come to $363.1 million, and it would be trading on a PE ratio of 9.8x, assuming you use a discount rate of 10.2%.

- Given the current share price of $27.18, the analyst price target of $25.9 is 4.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Star Bulk Carriers?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.