Key Takeaways

- Strategic positioning in maritime, IoT, and government sectors supports sustained revenue growth and market share expansion.

- Investment in Aireon's growth and new partnerships enhances revenue streams and financial metrics.

- Rising competition and strategic risks could pressure Iridium's revenue, market position, and profitability due to aggressive pricing, changing subscriber dynamics, and new project complexities.

Catalysts

About Iridium Communications- Provides mobile voice and data communications services and products to businesses, the United States and international governments, non-governmental organizations, and consumers worldwide.

- Iridium is positioning itself as a reliable companion to VSAT offerings, including Starlink, in the maritime sector. The introduction of Iridium service GMDSS for mariners and a focus on safety services aim to bolster their market share in safety-critical maritime applications, potentially driving future service revenue growth.

- The development and testing of Iridium NTN Direct, supporting standards-based narrowband IoT connections, are slated to begin in 2026. This advancement could significantly contribute to Iridium's IoT service revenue by expanding its reach in the satellite direct-to-device market by tapping into a new customer base and supporting broader commercial launches.

- Aireon, partially owned by Iridium, has expanded its aviation surveillance business and commercial data analytics services, providing significant opportunities for new revenue streams. As Aireon continues to grow its commercial partnerships, this may enhance Iridium's equity value and potential dividend income from Aireon, contributing indirectly to Iridium's financial metrics.

- New government contracts and a focus on strategic government partnerships, particularly with U.S. agencies, have boosted Iridium's service revenue and will likely continue to do so. The potential for expanded government contracts and sustained engagement with the U.S. Space Development Agency could ensure robust engineering and support revenue.

- The investment in new partners and product certifications, especially in IoT and land mobile sectors, presents expansion opportunities. By leveraging Iridium Certus IoT and integrating with cloud infrastructure, Iridium expects higher average revenue per user (ARPU) from IoT products, further driving top-line growth.

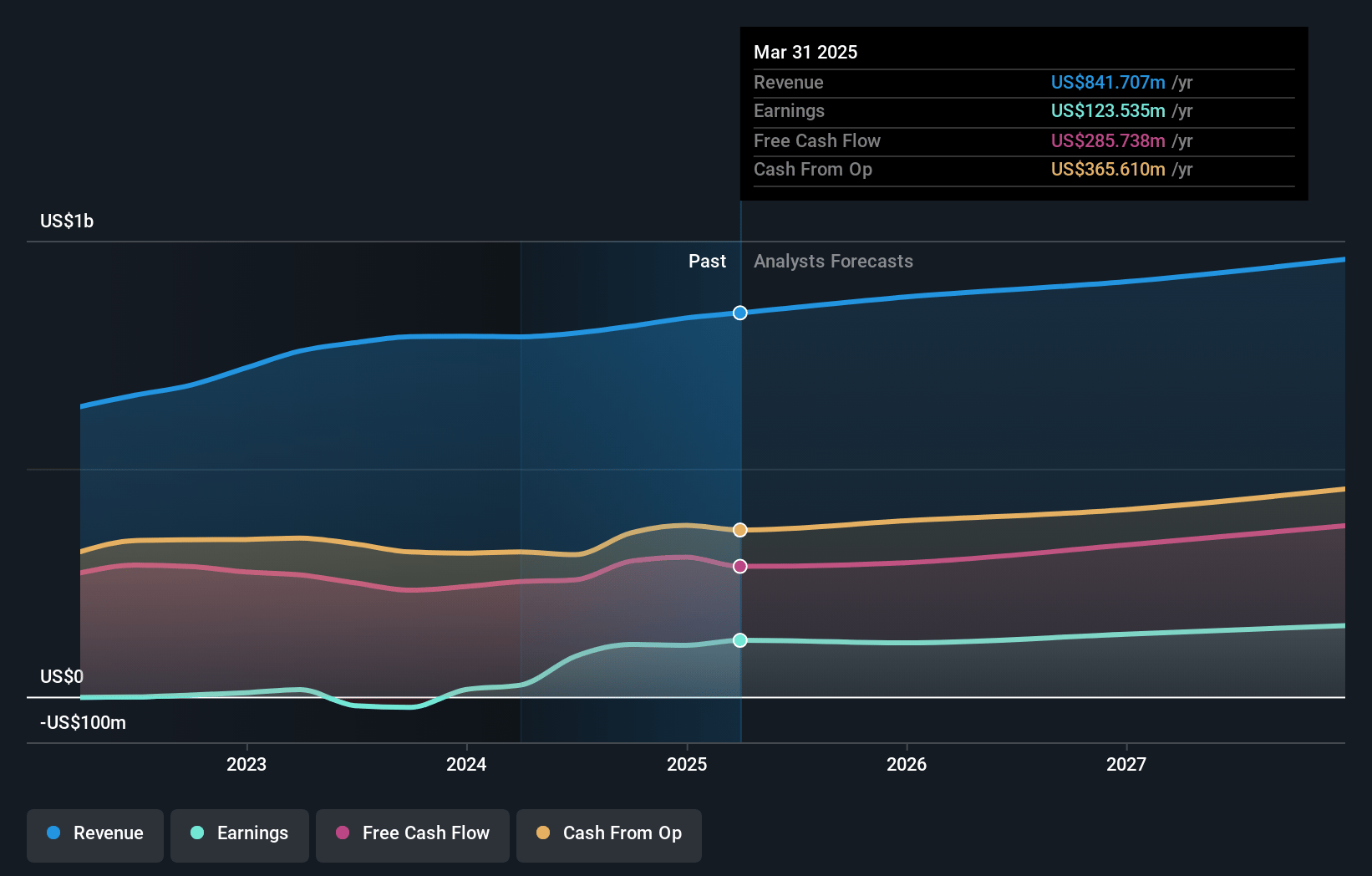

Iridium Communications Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Iridium Communications's revenue will grow by 4.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.6% today to 16.0% in 3 years time.

- Analysts expect earnings to reach $152.8 million (and earnings per share of $1.61) by about March 2028, up from $112.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $180.6 million in earnings, and the most bearish expecting $125.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.1x on those 2028 earnings, down from 28.7x today. This future PE is greater than the current PE for the US Telecom industry at 11.1x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

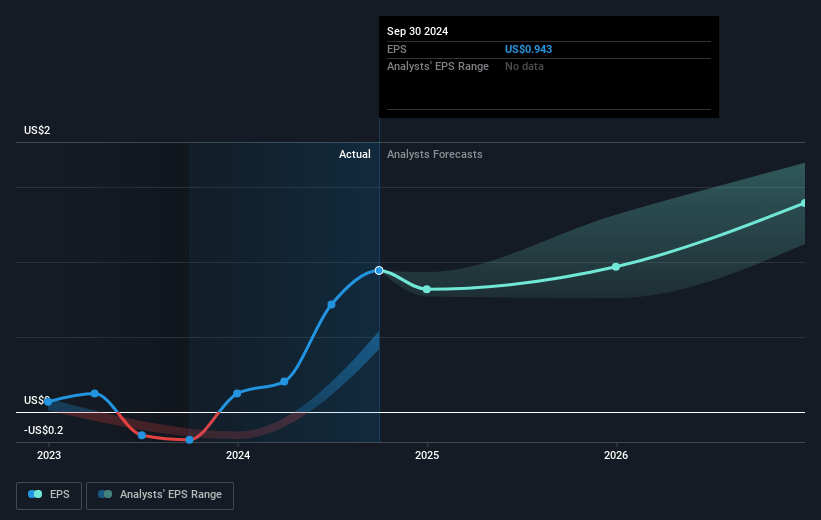

Iridium Communications Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The rise in short interest in Iridium's shares reflects a bearish sentiment on the broader satellite sector, driven by aggressive pricing and adoption by competitors like Starlink, which could pressure Iridium's future revenue and market position.

- Expectations of greater seasonality in Iridium's IoT subscriber base due to pricing plan changes might lead to fluctuations in subscriber numbers, potentially impacting revenue stability.

- The observed decline in ARPU for broadband services could continue as more customers transition from primary to companion services, potentially affecting net margins and profitability.

- The increased competition in the safety and mission-critical service sectors from companies offering complementary solutions to Starlink may limit Iridium’s market share growth and therefore its potential revenue and earnings.

- Strategic risks are associated with execution, particularly the involvement in complex new projects like the D2D market entry and the next-generation IoT technology, which may require significant investment and could impact future net margins if not managed efficiently.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $39.714 for Iridium Communications based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $49.0, and the most bearish reporting a price target of just $30.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $952.8 million, earnings will come to $152.8 million, and it would be trading on a PE ratio of 27.1x, assuming you use a discount rate of 6.2%.

- Given the current share price of $29.75, the analyst price target of $39.71 is 25.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.