Key Takeaways

- Strategic partnerships and increased semiconductor capacity are set to boost sales, market share, and profitability as demand for Vishay's products grows.

- Leveraging megatrends like e-mobility and adopting cost-efficient strategies position Vishay to enhance revenue growth and improve net margins.

- Prolonged inventory digestion, execution risks at Newport facility, ASP fluctuations, and high capital expenditure challenge Vishay's revenue growth, margins, and financial flexibility.

Catalysts

About Vishay Intertechnology- Manufactures and sells discrete semiconductors and passive electronic components in the United States, Germany, rest of Europe, Israel, and Asia.

- Vishay Intertechnology is setting itself up to leverage megatrends such as e-mobility and sustainability, positioning to accelerate revenue growth by tapping into these expanding markets. This could enhance future revenues as industry demand increases.

- The company is significantly expanding semiconductor capacity, both internally and externally. This expansion is expected to increase production capabilities, particularly in MOSFETs, which could lead to increased revenues and profitability as they meet higher customer demand.

- Bookings for products related to smart grid infrastructure projects, AI server power, and military defense are improving, suggesting a future increase in demand for Vishay's products. This upward trend in bookings indicates potential revenue growth.

- The strategic partnerships with SK Key Foundry and increased engagement with OEMs and distributors are likely to boost future sales and market share, thereby improving revenue and earnings as these relationships mature.

- Expansion projects like Newport and adopting a subcontractor strategy to produce components with lower capital investment create cost efficiencies that can improve net margins over time, increasing future profitability.

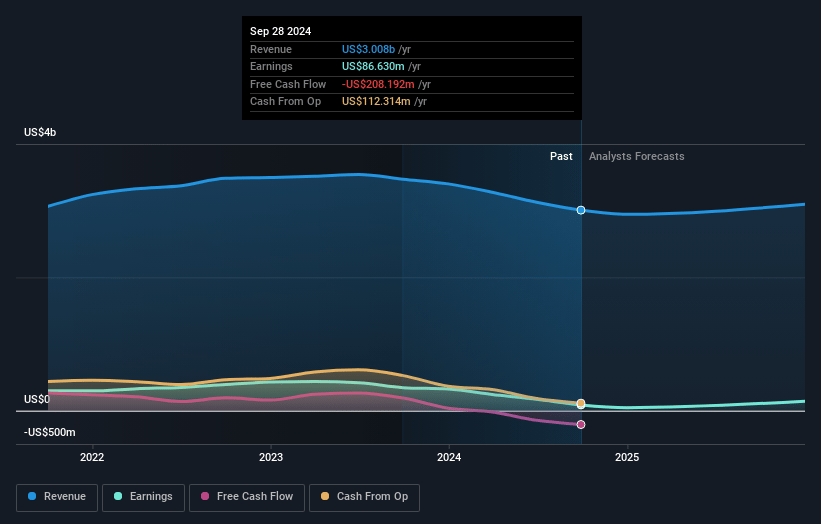

Vishay Intertechnology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Vishay Intertechnology's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -1.1% today to 13.6% in 3 years time.

- Analysts expect earnings to reach $475.6 million (and earnings per share of $3.58) by about April 2028, up from $-31.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 6.2x on those 2028 earnings, up from -57.0x today. This future PE is lower than the current PE for the US Electronic industry at 20.6x.

- Analysts expect the number of shares outstanding to decline by 1.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.99%, as per the Simply Wall St company report.

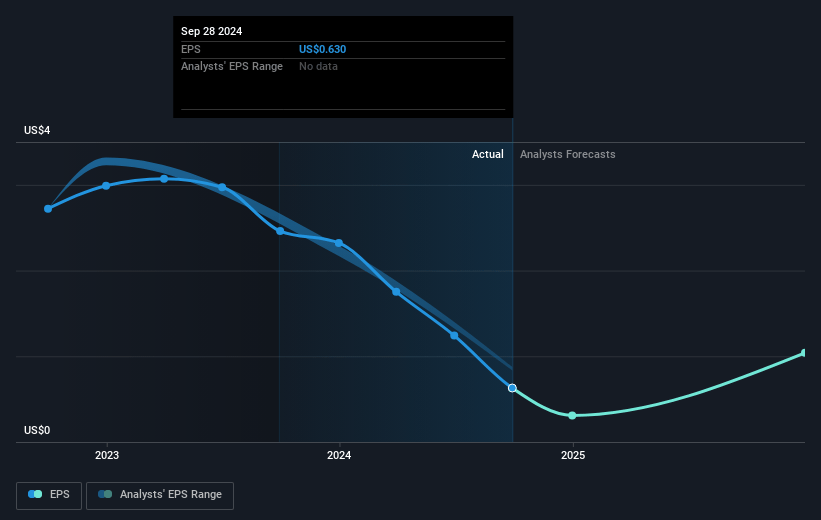

Vishay Intertechnology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The prolonged period of inventory digestion, especially in Europe, due to weak macroeconomic conditions and high component inventory could negatively impact Vishay's revenue growth and financial performance in the coming quarters.

- The company's reliance on capacity expansion projects and technology transfer, particularly at their Newport facility, poses execution risks. Delays in ramping up production or achieving customer qualifications could impact revenue and profitability.

- Vishay's exposure to fluctuations in average selling prices (ASP) could further pressure gross margins, as evidenced by the reported reduction in ASPs impacting both quarterly and annual revenues.

- High capital expenditure plans, combined with expectations of continued negative free cash flow, may limit Vishay's financial flexibility and ability to return capital to shareholders, thus impacting net margins and earnings.

- European market softness, driven by challenging macroeconomic conditions and distribution channel inventory levels, may hinder Vishay's ability to achieve growth targets, putting further pressure on revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.0 for Vishay Intertechnology based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.5 billion, earnings will come to $475.6 million, and it would be trading on a PE ratio of 6.2x, assuming you use a discount rate of 8.0%.

- Given the current share price of $13.09, the analyst price target of $18.0 is 27.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.