Key Takeaways

- Diversification into medical and aerospace sectors reduces dependency on transportation, enhancing revenue and profit margins.

- Strategic acquisitions and product innovation suggest robust future growth in diversified markets, fueled by operational efficiencies.

- Tariffs and geopolitical uncertainties threaten revenue and margins, with potential earnings fluctuations from acquisition delays and declining transportation sales.

Catalysts

About CTS- Manufactures and sells sensors, connectivity components, and actuators in North America, Europe, and Asia.

- CTS's diversification strategy, shown by strong growth in medical, aerospace, defense, and industrial markets, is likely to boost future revenue and earnings, reducing reliance on the more volatile transportation sector.

- The new product line in transportation and increased bookings in diversified end markets with a book-to-bill ratio of 1.28 point to significant future revenue growth potential.

- Expansion into minimally invasive medical applications and a strong pipeline in medical ultrasound indicate future revenue growth in the medical sector, enhancing profitability due to the higher-margin nature of these products.

- The integration and synergies from the SyQwest acquisition in aerospace and defense, along with a healthy backlog, suggest future revenue and profitability improvement due to operational efficiencies and reduced seasonality impacts.

- A planned increase in hybrid and electrification solutions in transportation, despite potential tariffs, points to potential revenue growth and margin stability due to product agnosticism to drivetrain technology.

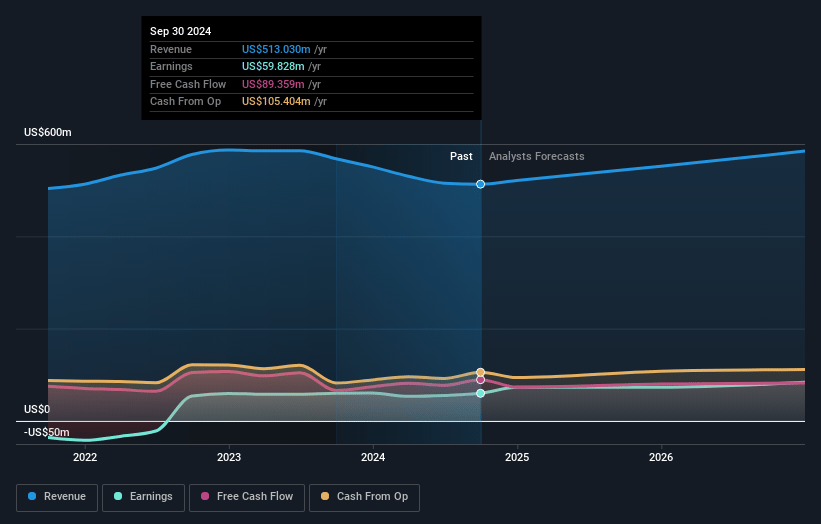

CTS Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CTS's revenue will grow by 5.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.3% today to 14.0% in 3 years time.

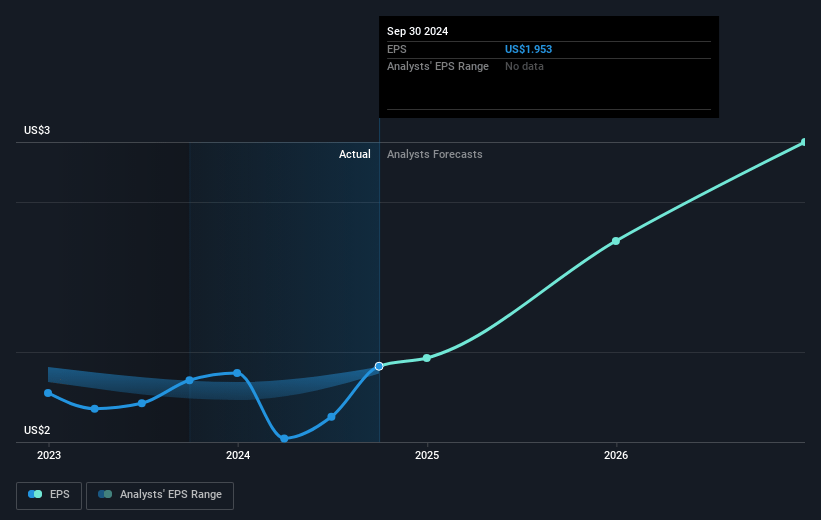

- Analysts expect earnings to reach $84.0 million (and earnings per share of $2.69) by about May 2028, up from $58.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.8x on those 2028 earnings, down from 20.6x today. This future PE is lower than the current PE for the US Electronic industry at 20.6x.

- Analysts expect the number of shares outstanding to decline by 1.73% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.53%, as per the Simply Wall St company report.

CTS Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of tariffs and the geopolitical environment is creating uncertainty, which could lead to decreased production volumes in transportation markets, impacting future revenue and potentially affecting net margins due to increased costs.

- The seasonality and potential delays in revenue recognition from the SyQwest acquisition could cause fluctuations in quarterly earnings and may not align with expectations, impacting overall earnings consistency.

- Transportation sales experienced a 12% decline due to challenges in the China market and competitive pressures, which could lead to lower revenue and profitability if this trend continues.

- The company's reliance on successful negotiations around tariffs and pricing with customers could impact operating profitability if these costs cannot be fully passed on, potentially squeezing net margins.

- Any further escalation in tariffs or changes to trade agreements (such as USMCA exemptions on Mexican imports) could negatively affect overall demand and disrupt supply chains, impacting revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $43.0 for CTS based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $599.5 million, earnings will come to $84.0 million, and it would be trading on a PE ratio of 17.8x, assuming you use a discount rate of 7.5%.

- Given the current share price of $39.89, the analyst price target of $43.0 is 7.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.