Key Takeaways

- Strategic acquisitions and partnerships position Gilat to capture growth in in-flight connectivity and satellite communications, boosting long-term revenue potential.

- Organizational restructuring and focus on emerging markets and sectors promise improved operational efficiency and sustainable profitability.

- Geopolitical risks, fierce competition, and integration costs challenge revenue, market share, and margins, while delays in contracts and launches threaten growth trajectories.

Catalysts

About Gilat Satellite Networks- Provides satellite-based broadband communication solutions in Israel, the United States, Peru, and internationally.

- The acquisition of Stellar Blu and DataPath positions Gilat to expand in the fast-growing in-flight connectivity (IFC) market and defense sector, which is expected to accelerate revenue growth in 2025 and beyond.

- The new organizational structure focusing on the Gilat Defense, Gilat Commercial, and Gilat Peru divisions will streamline operations and sharpen focus on key growth areas, potentially improving net margins and simplifying investor understanding.

- Increasing demand for satellite communications in defense due to macro political dynamics and the need for multi-orbit connectivity drives new opportunities, likely boosting earnings through strategic investments in R&D and sales.

- Strong partnerships with industry leaders like Intelsat and advancements with the SkyEdge IV platform for next-generation satellite networking create new long-term revenue streams as satellite constellations expand.

- Continued progress in bridging the digital divide in Peru, coupled with robust RFPs with Pronatel and government expansion projects, supports sustainable top-line growth and improved EBITDA margins in regional operations.

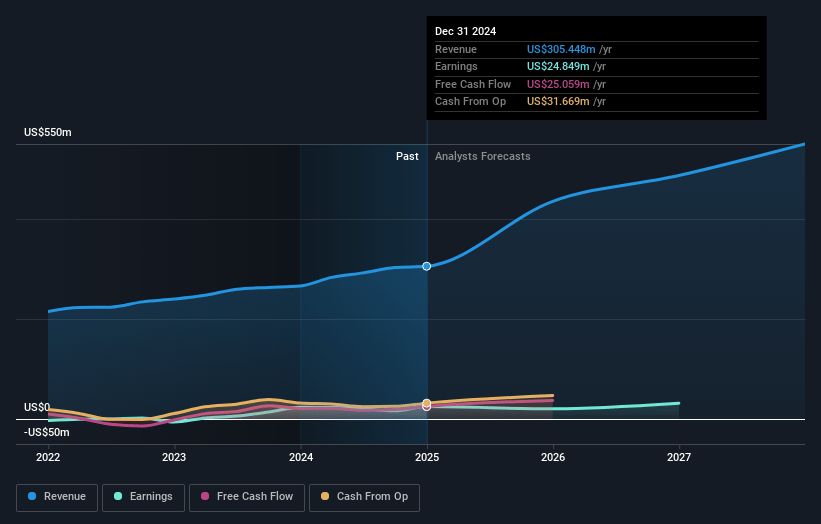

Gilat Satellite Networks Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Gilat Satellite Networks's revenue will grow by 21.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.1% today to 6.5% in 3 years time.

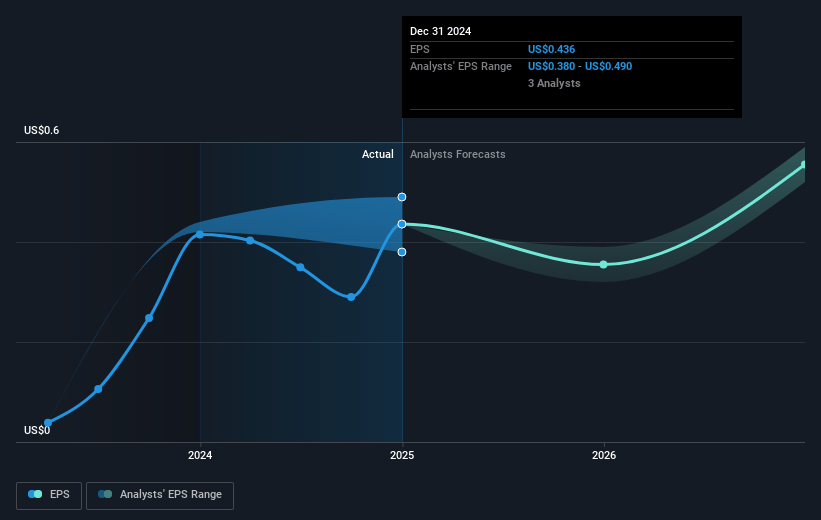

- Analysts expect earnings to reach $35.5 million (and earnings per share of $0.63) by about May 2028, up from $24.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.5x on those 2028 earnings, up from 14.6x today. This future PE is lower than the current PE for the US Communications industry at 20.3x.

- Analysts expect the number of shares outstanding to grow by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.05%, as per the Simply Wall St company report.

Gilat Satellite Networks Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The termination of operations in Russia has negatively impacted revenue, indicating geopolitical risks and potential opportunities lost in large markets. This could affect future revenue streams if similar geopolitical issues arise.

- The integration of Stellar Blu involves upfront costs, lower initial gross profits, and extensive R&D and marketing investments, which might pressure net margins and EBITDA in the near term.

- Increased competition in the IFC market, particularly with companies like SpaceX, poses risks to Gilat's market share and top-line growth if they cannot maintain competitive pricing and technology leadership.

- Potential delays and aggressive timelines in obtaining contracts from significant consortia like IRIS2 may impact projected revenue growth, aligning with uncertainties influencing earnings forecasts.

- Challenges in the commercial segment, including delays in satellite launches affecting new network deployments, suggest potential stagnation in revenue growth from this area if postponed further.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $8.4 for Gilat Satellite Networks based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $549.9 million, earnings will come to $35.5 million, and it would be trading on a PE ratio of 17.5x, assuming you use a discount rate of 9.0%.

- Given the current share price of $6.36, the analyst price target of $8.4 is 24.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.