Narratives are currently in beta

Key Takeaways

- Strategic focus on cloud and AI capabilities enhances revenue growth prospects through subscriptions, partnerships, and enterprise AI strategies.

- Scalability demonstrated by high transaction volume anticipates improved operational efficiency and positive net margin impact.

- Dependence on cloud migrations and new cloud strategies amidst declining traditional revenues and risks from an evolving macroeconomic environment poses future revenue and earnings challenges.

Catalysts

About Informatica- Develops an artificial intelligence-powered platform that connects, manages, and unifies data across multi-vendor, multi-cloud, and hybrid systems at enterprise scale worldwide.

- Informatica's focus on accelerating on-prem to cloud migrations, particularly with PowerCenter Cloud Edition, is expected to modernize mission-critical workloads and drive cloud subscription ARR growth. This could have a positive impact on future revenue opportunities.

- The company's strong expansion in new cloud workloads, as evidenced by the 36% year-over-year growth in cloud subscription ARR, and strategic engagement with large enterprises spending over $1 million in subscription ARR, indicates potential for significant revenue growth.

- Informatica's AI capabilities, especially in GenAI with the expansion of CLAIRE GPT, aim to simplify data estates and support enterprise AI strategies, which can drive higher customer retention and usage, positively affecting net margins and earnings.

- Informatica’s increasing number of partnerships with significant ecosystem players like AWS, Azure, and Oracle, as well as with partners like Capgemini and Deloitte, hint at an expanded market reach and potential acceleration in revenue and net margins.

- Informatica's recent achievement of processing 100 trillion cloud transactions per month underscores the scalability of its cloud platform, which could lead to improvements in revenue and operational efficiencies impacting net margins positively.

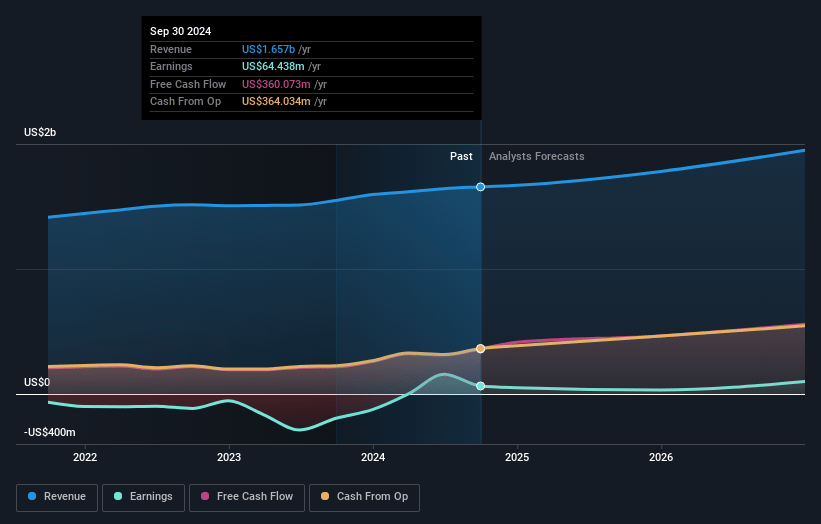

Informatica Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Informatica's revenue will grow by 9.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.9% today to 4.8% in 3 years time.

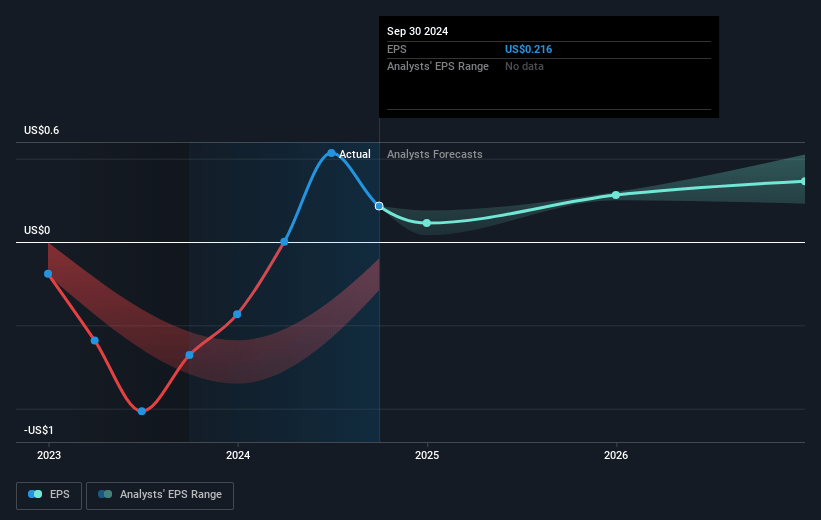

- Analysts expect earnings to reach $104.6 million (and earnings per share of $0.47) by about November 2027, up from $64.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $155.9 million in earnings, and the most bearish expecting $29.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 86.5x on those 2027 earnings, down from 122.0x today. This future PE is greater than the current PE for the US Software industry at 41.0x.

- Analysts expect the number of shares outstanding to decline by 10.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.43%, as per the Simply Wall St company report.

Informatica Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in self-managed subscriptions and maintenance revenue indicates a potential drop in traditional product lines, possibly impacting total revenue growth if new cloud strategies do not fully compensate for these losses.

- Despite positive cloud ARR growth, a notable dependency on migrations from on-premise to cloud systems underscores potential risk if these migrations slow down or customers opt for competing services, impacting future revenue streams and ARR.

- The evolving macroeconomic environment, although currently stable, could pose risks depending on global economic conditions, potentially affecting customer budgets and thus impacting Informatica's revenue and earnings.

- The focus on GenAI developments carries inherent risks, including technological execution risks and competition from other AI-driven data management solutions, which could affect market share and earnings if not managed effectively.

- Changes in public sector projects or funding levels could lead to variability in revenue, posing risks if significant portions of revenue rely on government contracts that may be subject to budget shifts or policy changes.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $32.89 for Informatica based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $25.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $2.2 billion, earnings will come to $104.6 million, and it would be trading on a PE ratio of 86.5x, assuming you use a discount rate of 7.4%.

- Given the current share price of $25.74, the analyst's price target of $32.89 is 21.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives