Narratives are currently in beta

Key Takeaways

- GoDaddy's enhanced pricing, marketing, and platform initiatives aim to boost customer value, accelerate acquisition, and grow revenue across segments.

- AI and infrastructure investments focus on cost efficiency and operational leverage, potentially improving net margins and expanding EBITDA margins.

- GoDaddy's strategic initiatives in AI, pricing, and capital allocation are enhancing efficiency, customer retention, and shareholder value, supporting robust revenue and margin growth.

Catalysts

About GoDaddy- Engages in the design and development of cloud-based products in the United States and internationally.

- GoDaddy's pricing and bundling initiatives, which leverage software platforms and machine learning to offer greater customer value, are set to expand beyond the Applications & Commerce (A&C) segment into the core platform. This could favorably drive growth in both segments, impacting future revenue positively.

- Increased investment in marketing to support the broader launch of Airo means GoDaddy plans to accelerate customer acquisition through more discovery and engagement, potentially improving top-line growth and impacting future revenue.

- GoDaddy is enhancing the Airo platform, introducing monetization paths such as paywalls for Websites + Marketing and other products. If successful, this could significantly boost earnings growth as Airo becomes a larger on-ramp for products.

- The expansion of AI and machine learning, such as the company’s new generative AI-powered conversational bot, aims to improve customer service efficiency and contain costs, which could enhance future net margins.

- Commitment to increasing investment in infrastructure simplification and global talent recruitment suggests continued operational leverage and cost optimization, which could lead to EBITDA margin expansion and improved earnings.

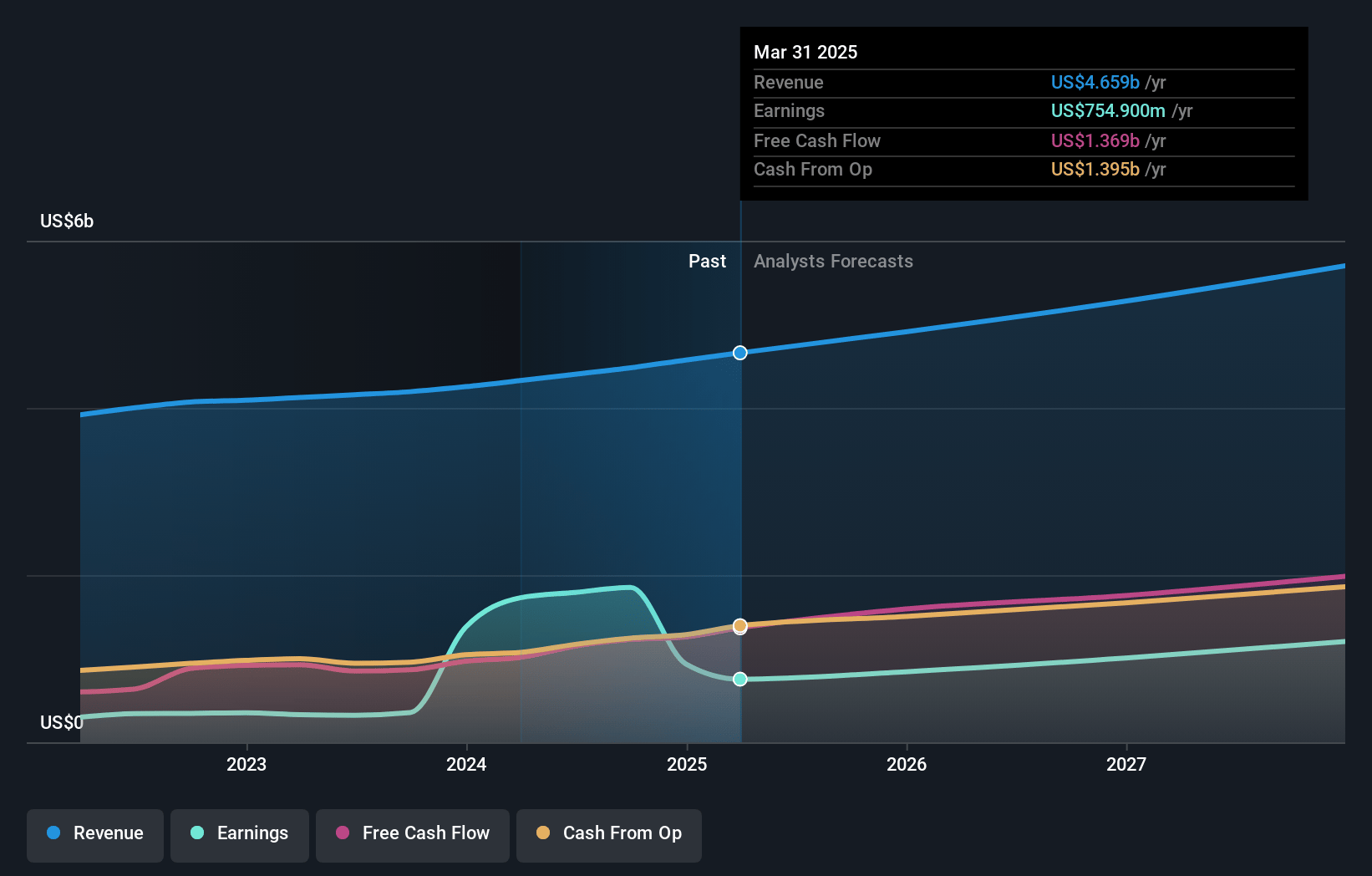

GoDaddy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GoDaddy's revenue will grow by 8.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 41.3% today to 21.8% in 3 years time.

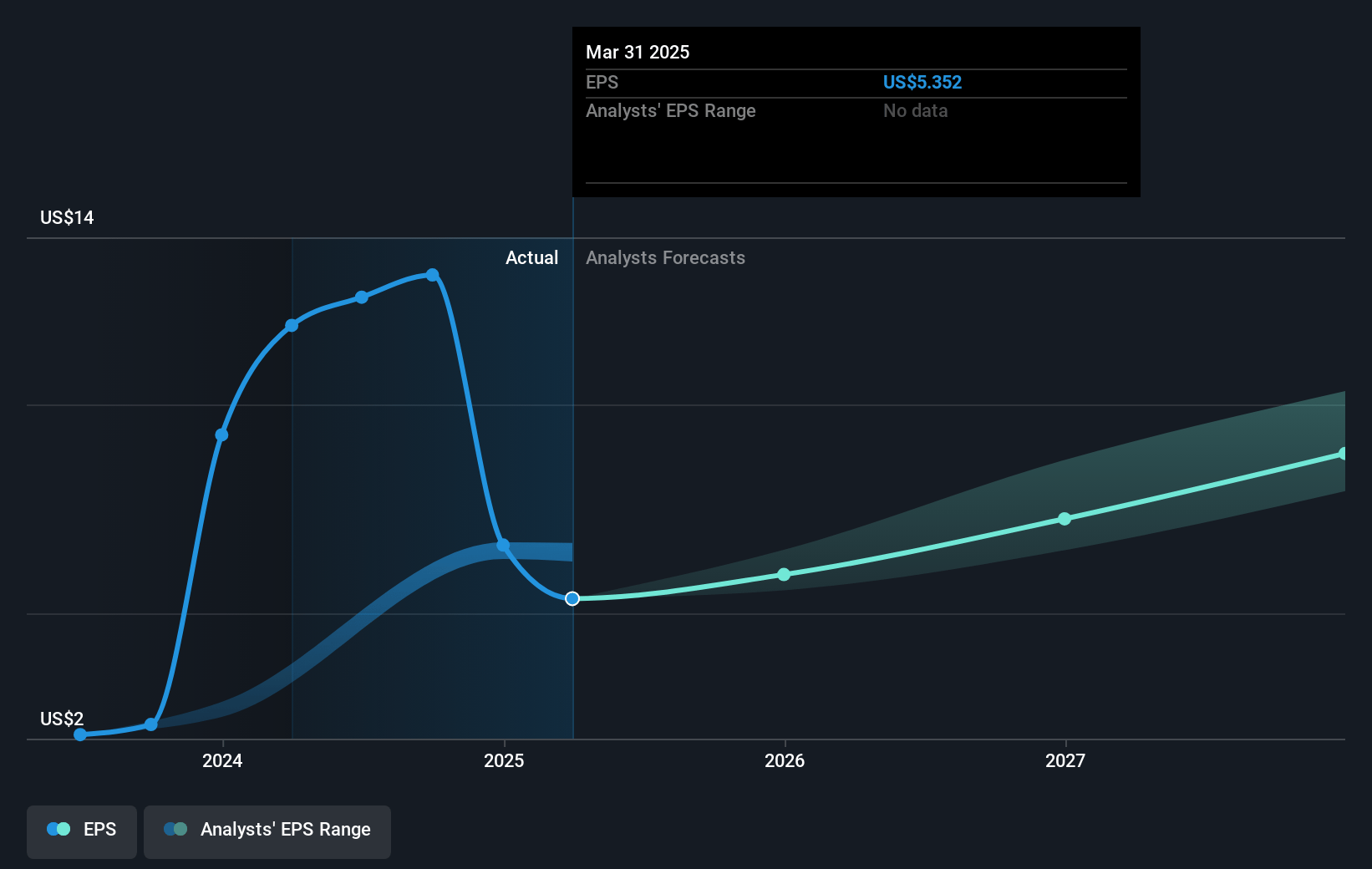

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $9.83) by about November 2027, down from $1.9 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $955 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.6x on those 2027 earnings, up from 12.7x today. This future PE is lower than the current PE for the US IT industry at 44.5x.

- Analysts expect the number of shares outstanding to decline by 3.34% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 7.41%, as per the Simply Wall St company report.

GoDaddy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- GoDaddy's focus on Pricing & Bundling, combined with machine learning capabilities, is driving productivity and could positively impact both Application & Commerce (A&C) and core platform segments, supporting revenue growth.

- Initiatives to enhance the seamless customer experience by reducing friction in purchase, onboarding, and renewal could improve customer conversion and retention, likely boosting net margins and long-term revenue stability.

- GoDaddy's conversational AI, Airo, and broader AI-powered features are demonstrating positive adoption and engagement trends, potentially enhancing operational efficiency and reducing costs, which could improve net margins and profitability.

- The commitment to share buybacks and disciplined capital allocation strategy may positively influence earnings and shareholder value, indicating potential resilience in the company's financials.

- With a robust growth in free cash flow and normalized EBITDA margin expansion, GoDaddy's financial forecasting reflects confidence in sustained margin improvement and cash generation, which contradicts a bearish outlook on earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $179.95 for GoDaddy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $200.0, and the most bearish reporting a price target of just $135.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $5.7 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 22.6x, assuming you use a discount rate of 7.4%.

- Given the current share price of $167.63, the analyst's price target of $179.95 is 6.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives