Last Update 17 Jun 26

Fair value Decreased 1.55%ROP: Cash Returns And AI Software Mix Will Support Post Reset Re Rating

The updated analyst price target for Roper Technologies now stands at $446.80, down from $453.82. Analysts attribute this change to a balance between slightly higher revenue growth and profit margin assumptions and a modestly lower future P/E outlook.

Analyst Commentary

Recent Street research around Roper Technologies highlights a mix of optimism and caution, with several firms adjusting their price targets in different directions. For you as an investor, the key themes center on how the company might execute on its growth plans and how that lines up with current valuation expectations.

Bullish Takeaways

- Bullish analysts who raised their price targets point to assumptions of stronger revenue growth and solid profit margins, which they view as supportive of a higher long term earnings profile for Roper Technologies.

- These analysts appear comfortable that the current P/E leaves some room for upside if the company delivers on its operational targets and aligns capital allocation with earnings quality.

- Supportive price target changes suggest confidence that Roper Technologies can sustain its business model without needing major shifts to justify the current valuation framework.

- Positive revisions also indicate that some forecasts factor in a resilient earnings stream, which can be attractive for investors who prioritize consistency over rapid acceleration.

Bearish Takeaways

- Bearish analysts who trimmed their price targets highlight a more cautious stance on how much investors should be willing to pay in terms of future P/E for Roper Technologies.

- The lower target move suggests concern that valuation already reflects a lot of the expected growth, leaving less cushion if execution on revenue or margins comes in below forecasts.

- More conservative views emphasize the risk that any setback in operational performance could lead to pressure on the stock if current expectations remain high.

- Overall, the downward adjustment in at least one target signals that not all analysts see the risk and reward trade off as skewed positively at current valuation levels.

What’s in the News for Roper Technologies

- Roper Technologies reported Q1 2026 results with 11% revenue growth, including 6% organic growth, supported by acquisitions, according to recent earnings coverage.

- The company raised its full-year 2026 adjusted diluted EPS guidance, with one source citing an increase of $0.50 at the midpoint and another citing a new range of $21.80 to $22.05, reflecting higher earnings expectations. (Source: Q1 2026 earnings reports)

- Roper Technologies accelerated AI initiatives across its portfolio, with several businesses launching AI-enabled products and an AI accelerator team supporting development and commercialization. (Source: Q1 2026 earnings reports)

- Capital returns increased, with about 6,000,000 shares repurchased for US$2.2b during the quarter. The board also authorized an additional US$3b, bringing remaining buyback capacity to US$3.8b. (Source: Q1 2026 earnings reports and buyback plan update)

- The company indicated ongoing interest in acquisitions. Management highlighted an active M&A pipeline focused on high quality software businesses and a continued balance between acquisitions and opportunistic share repurchases. (Source: Q1 2026 earnings call commentary)

Valuation Changes for Roper Technologies

- Fair Value: The updated estimate has fallen slightly from $453.82 to $446.80, reflecting a modestly lower implied valuation for Roper Technologies stock.

- Discount Rate: The assumed discount rate has risen slightly from 9.38% to 9.46%, indicating a small increase in the required return used in the valuation model.

- Revenue Growth: The revenue growth assumption has risen slightly from 7.98% to 8.47%, pointing to a somewhat higher expected top line trajectory in the model.

- Net Profit Margin: The profit margin assumption has edged higher from 20.29% to 20.38%, suggesting a marginally stronger earnings profile on each dollar of revenue.

- Future P/E: The future P/E assumption has fallen from 23.78x to 23.03x, indicating that the model now applies a slightly lower earnings multiple to Roper Technologies.

Key Takeaways

- Accelerating adoption of AI-driven, vertical-specific SaaS platforms is expanding margins, boosting subscription revenue stability, and fueling long-term organic growth.

- Significant opportunity remains in under-digitized, data-rich sectors, supporting ongoing market share gains and recurring revenue expansion as digital transformation advances.

- Heavy dependence on acquisitions and niche markets, alongside regulatory, technological, and integration risks, threatens Roper's margin sustainability and future organic revenue growth.

Catalysts

About Roper Technologies- Designs and develops vertical software and technology enabled products in the United States, Canada, Europe, Asia, and internationally.

- The rapid adoption of AI and cloud-native solutions across Roper's portfolio is unlocking significant productivity gains (cited 30% R&D productivity increase in some business units) and enabling monetization of new, AI-driven products and upgrades, which is expected to accelerate organic revenue growth and expand operating margins over time.

- Penetration of under-digitized, data-rich sectors-including faith-based organizations, healthcare, legal, and government contracting-remains nascent, with large TAMs only 50% served in some cases (e.g., Subsplash), indicating substantial runway for recurring revenue and market share gains as digital transformation accelerates within these verticals.

- Increased focus on integrating mission-critical, vertical-specific SaaS platforms that combine software, payments, and network effects is driving higher gross/net customer retention, enabling a higher mix of stable, subscription-based revenues, which enhances earnings predictability and cash flow stability.

- Ongoing, disciplined capital deployment into high-growth, high-margin vertical market software leaders (e.g., Subsplash, CentralReach) is incrementally raising the portfolio's underlying organic growth rate and long-term margin profile, supporting robust free cash flow compounding and the potential for EBITDA margin expansion.

- Secular increases in data proliferation, automation needs, and regulatory complexity, especially within healthcare and compliance-driven segments, are fueling demand for analytics-rich, secure, and integrated software solutions-well aligned with Roper's core offerings, underpinning sustainable revenue growth and margin resilience.

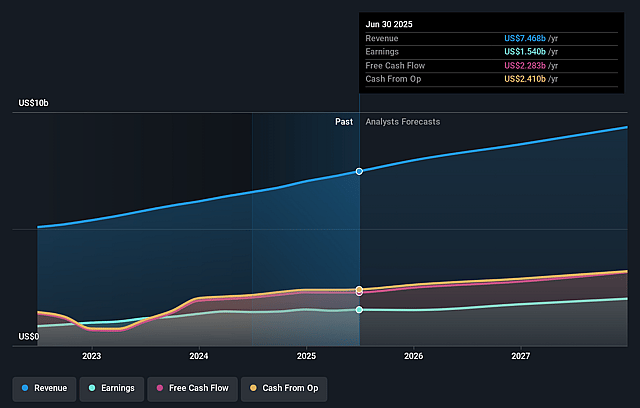

Roper Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Roper Technologies's revenue will grow by 8.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 21.1% today to 20.4% in 3 years time.

- Analysts expect earnings to reach $2.1 billion (and earnings per share of $20.54) by about June 2029, up from $1.7 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $2.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.1x on those 2029 earnings, up from 19.9x today. This future PE is lower than the current PE for the US Software industry at 26.4x.

- Analysts expect the number of shares outstanding to decline by 6.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Roper's continued reliance on M&A-driven growth, as evidenced by their focus on acquiring vertical market software businesses (e.g., CentralReach, Subsplash), increases the risk of integration challenges and may lead to operational inefficiencies or diluted net margins over time, as shown by initial underperformance at Procare and related management turnover.

- The company's outlook assumes market stability and ongoing organic growth in niche verticals such as education, legal, and faith-based organizations; however, these markets may approach saturation, resulting in slowing organic revenue growth and limiting the company's ability to sustain its historic top-line trajectory.

- The rising complexity of regulatory requirements (e.g., healthcare coverage changes, potential government spending volatility) and increased scrutiny on data privacy and cybersecurity could raise compliance costs, expose the company to reputational or operational risk, and negatively impact earnings and margin profiles for its software platforms.

- Intensifying competition and rapid technological change in the software sector-especially from large enterprise software providers and new entrants offering more advanced AI capabilities-pose a threat to Roper's market share, pricing power, and may require increased R&D investment just to maintain current revenue streams.

- The risk of commoditization in business software, particularly as clients expect more AI-native or cloud-integrated solutions, may lead to downward pressure on pricing and margins if Roper is unable to sustain differentiated value, impacting both future revenue growth and long-term net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $446.8 for Roper Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $550.0, and the most bearish reporting a price target of just $349.78.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $10.4 billion, earnings will come to $2.1 billion, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 9.5%.

- Given the current share price of $337.33, the analyst price target of $446.8 is 24.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roper Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.