Key Takeaways

- Qualys's shift to a comprehensive risk analytics platform and new cloud security capabilities enhance its market relevance and potential for revenue growth.

- Strategic partnerships and a focus on federal market opportunities aim to boost sales growth and long-term profitability through partner-led sales strategies.

- Executive departures, partner-focused strategy, and certification delays may disrupt sales execution and revenue growth, particularly amidst economic uncertainties.

Catalysts

About Qualys- Provides cloud-based platform delivering information technology (IT), security, and compliance solutions in the United States and internationally.

- Qualys has transitioned from a vulnerability scanning platform to a comprehensive risk analytics and quantification platform, integrating data analytics and AI models. This shift to a vendor-neutral orchestration platform aims to increase platform adoption, impacting future revenues through enhanced market relevance and customer retention.

- The introduction of new capabilities like TruRisk Eliminate and TruRisk Uninstall aims to address critical vulnerabilities and tech debt, offering competitive advantages that could result in higher margins by reducing cyber risk more efficiently and effectively than competitors.

- Expansion of capabilities in the cloud security space with TotalCloud 3.0 aims to capture more market share in the growing cloud security market, which could drive revenue growth by appealing to organizations seeking comprehensive cloud security solutions.

- Continued development of partnerships with managed security service providers (MSSPs) and progress towards FedRAMP High certification are expected to unlock significant opportunities in the federal market and enhance sales growth through partner-led sales strategies.

- Focus on partner-first sales and potential packaging opportunities around the ETM solution aim to enhance broader platform adoption and increase net dollar expansion rates, thereby positively impacting long-term revenue growth and profitability.

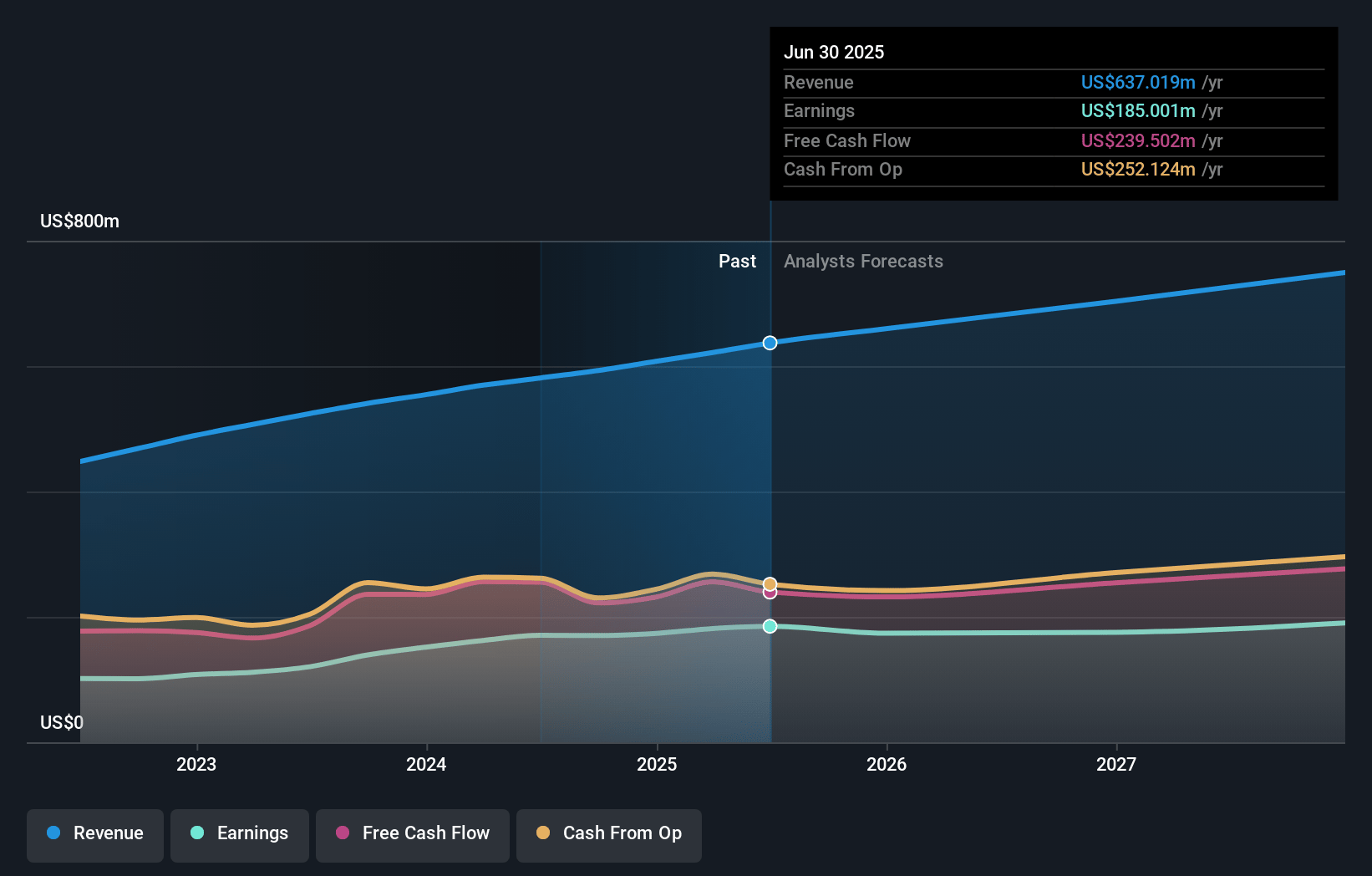

Qualys Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Qualys's revenue will grow by 6.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 28.6% today to 23.9% in 3 years time.

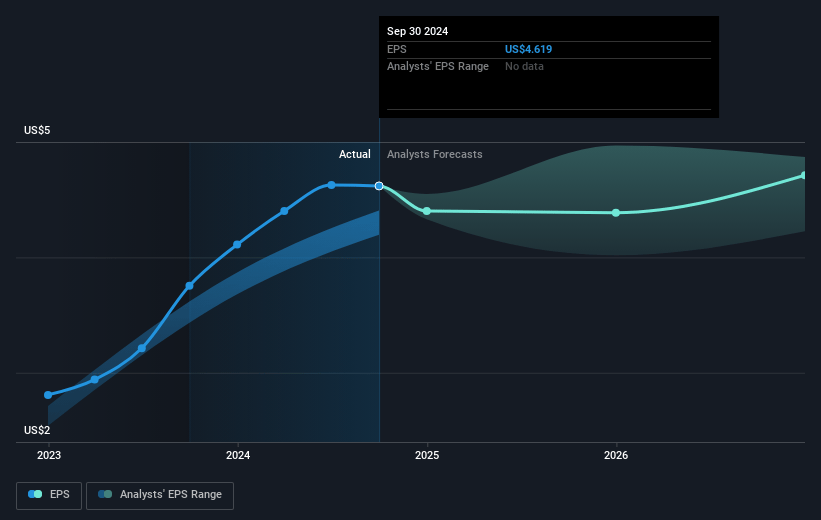

- Analysts expect earnings to reach $176.1 million (and earnings per share of $4.77) by about April 2028, up from $173.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.4x on those 2028 earnings, up from 25.1x today. This future PE is greater than the current PE for the US Software industry at 29.6x.

- Analysts expect the number of shares outstanding to decline by 1.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.61%, as per the Simply Wall St company report.

Qualys Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The departure of Chief Revenue Officer Dino DiMarino raises concerns about potential disruptions in sales execution, which could negatively impact revenue growth.

- Qualys' shift toward a partner-focused sales strategy may carry risks, as it could lead to reduced control over direct sales channels and create shorter-term revenue growth challenges.

- The anticipated administrative changes and FedRAMP High certification delays may slow GSA adoption, affecting revenue growth prospects within the federal sector.

- Budget scrutiny from clients, especially in light of potential recession signals, may lead to slower net revenue retention rates if clients consolidate their cybersecurity spend or delay placing orders.

- The departure of top executives and organizational changes might create execution risks, potentially impacting overall net margins and bottom-line earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $138.899 for Qualys based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $175.0, and the most bearish reporting a price target of just $90.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $737.5 million, earnings will come to $176.1 million, and it would be trading on a PE ratio of 34.4x, assuming you use a discount rate of 7.6%.

- Given the current share price of $119.5, the analyst price target of $138.9 is 14.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.