Last Update 17 Jun 26

HCKT: AI And Workflow Solutions Will Support Future Stock Upside

Analysts have trimmed their price target on Hackett Group stock by $1, citing updated views on discount rates, profit margins, and future P/E expectations reflected in recent research commentary.

What’s in the News for Hackett Group

- Hackett Group joined the ServiceNow Partner Program as a Consulting and Implementation partner to help organizations identify high-value AI opportunities and accelerate workflow transformation using Hackett AI XPLR and the ServiceNow AI Platform. (Source: Company client announcement)

- The company issued earnings guidance for Q2 2026, estimating total revenue before reimbursements in a range of $68.5 million to $70.0 million. (Source: Corporate guidance)

- From December 27, 2025 to March 27, 2026, Hackett Group repurchased 211,807 shares for $2.97 million, bringing cumulative buybacks under the July 30, 2002 program to 36,183,741 shares for $347.04 million, which the company states is 97.34% of the announced authorization. (Source: Buyback tranche update)

- Hackett Group released the Spring 2026 SolutionMap and TechMatch procurement technology assessments, covering 118 vendors across 16 source-to-pay categories and integrating SolutionMap data into its Solution Intelligence programs after the Spend Matters acquisition in 2025. (Source: Product-related announcement)

- The company introduced Applied Intelligence, an expert-led decision support model, and AskHackett, a Gen AI-powered conversational agent, aimed at helping senior leaders in finance, procurement, HR, technology and global business services apply Hackett Group benchmark and process data to their own organizations. (Source: Product-related announcement)

Valuation Changes for Hackett Group Stock

- Fair Value: Model fair value for Hackett Group is unchanged at $17.67.

- Discount Rate: The discount rate has risen slightly from 9.28% to 9.59%, which indicates a modestly higher required return in the updated assumptions.

- Revenue Growth: The long-term revenue growth input remains effectively stable, with the updated figure at a 0.71% decline compared with the prior 0.71% decline assumption.

- Net Profit Margin: The profit margin assumption has risen from 19.36% to 21.74%, which implies a higher expected share of revenue flowing through to earnings in the model.

- Future P/E: The future P/E multiple has been trimmed from 8.32x to 7.47x, which points to a slightly more conservative valuation multiple applied to Hackett Group earnings.

Key Takeaways

- Expanding AI-driven products, partnerships, and recurring revenue streams is set to accelerate growth, enhance margins, and increase pricing power.

- Investments in proprietary technology, client-focused innovation, and operational efficiency are driving stronger service delivery, larger pipelines, and improved earnings quality.

- Delays in Gen AI monetization, declining legacy revenues, execution risks, rising costs, and client uncertainty threaten margin growth, stability, and predictable revenue for Hackett Group.

Catalysts

About Hackett Group- Operates as an intellectual property platform-based generative artificial intelligence strategic consulting and executive advisory digital transformation in the United States, Europe, and internationally.

- The imminent full release and licensing of AI XPLR version 4, paired with ZBrain and a new JV focused on a SaaS platform, is poised to transform Hackett Group's revenue mix by unlocking high-margin, recurring licensing and ARR streams, which should drive faster revenue growth and boost operating/net margins.

- The accelerated adoption of Gen AI solutions across enterprise clients-evidenced by strong growth in Gen AI consulting, high client engagement, and a rising share of AI in new projects-is expected to expand Hackett's addressable market and result in a sustained, higher-value project pipeline, directly supporting top-line and earnings growth.

- Strategic alliances, such as the just-announced Celonis partnership and active discussions with additional channel partners, will enhance Hackett Group's access to large enterprise client bases and speed go-to-market for its differentiated Gen AI offerings, likely increasing new client acquisition and bolstering revenue growth.

- Ongoing investment in integrating proprietary IP, process intelligence, and Gen AI into advisory and benchmarking solutions-along with positive client feedback on recently launched features-positions Hackett Group to reinforce pricing power and margin expansion as clients increasingly require advanced, technology-enabled transformation support.

- Productivity improvements and cost efficiencies from Gen AI-assisted platforms (like Accelerator), coupled with targeted restructuring, are expected to improve service delivery margins and allow Hackett to redeploy resources towards higher-growth, higher-margin areas, strengthening overall earnings and margin trajectory.

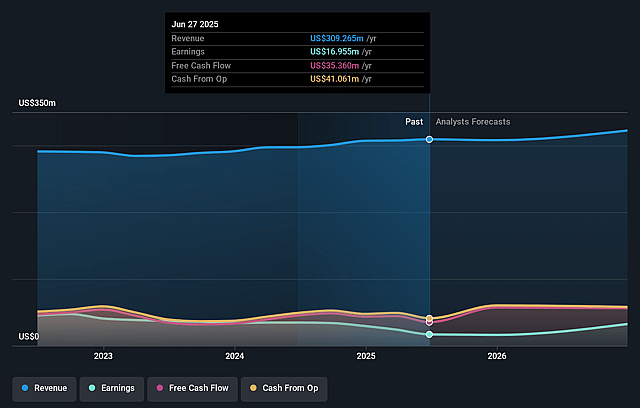

Hackett Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Hackett Group's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 4.8% today to 21.7% in 3 years time.

- Analysts expect earnings to reach $62.2 million (and earnings per share of $2.24) by about June 2029, up from $14.1 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.6x on those 2029 earnings, down from 19.2x today. This future PE is lower than the current PE for the US IT industry at 18.6x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged delays in licensing and monetization of key Gen AI platforms (like AI XPLR), as highlighted by management's acknowledgment that licensable products are still not released and prospects are taking longer than expected, could limit revenue growth and recurring ARR expansion in the near to medium term, negatively impacting topline growth.

- Ongoing weakness and uncertain recovery in core legacy segments such as Oracle Solutions and OneStream, with management projecting a 20%+ year-over-year decline for Oracle in Q3 and continued negative revenue impact from the inability to replace large engagements, suggest potential for flat or declining segment revenues and earnings volatility.

- Rising dependence on rapid innovation and pivot to Gen AI may pose operational and execution risks-if client adoption of proprietary solutions or new SaaS offerings lags, or if competitors outpace Hackett in feature development, this could threaten margin expansion and reduce the pricing power the company anticipates.

- Increasing SG&A expenses (up year-over-year as a percentage of revenues) and the need for restructuring charges, particularly as headcount is adjusted for AI productivity gains, highlight cost pressures and risks of sub-optimal utilization during project transitions, with potential negative impact on net margins and near-term profitability.

- Elevated client decision-making uncertainty, as seen in delayed project starts and shifting IT budgets, could persist as organizations navigate macro conditions and evolving Gen AI technology landscapes, which may result in continued lumpy demand, longer sales cycles, and unpredictable cash flow and revenue forecasts.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $17.67 for Hackett Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $286.3 million, earnings will come to $62.2 million, and it would be trading on a PE ratio of 7.6x, assuming you use a discount rate of 9.6%.

- Given the current share price of $10.76, the analyst price target of $17.67 is 39.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Hackett Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.