Key Takeaways

- JFrog’s strategy focuses on enterprise subscriptions and cloud partnerships, driving consistent revenue growth through software supply chain tools and cloud services.

- Investments in AI and security, including the acquisition of Qwak AI, aim to enhance customer value and sustain earnings growth by expanding capabilities.

- Dependency on large deals and cloud adoption introduces volatility, with cautious spending and heavy investments posing risks to revenue growth and margins.

Catalysts

About JFrog- Provides software supply chain platform in the United States, Israel, India, and internationally.

- JFrog’s enterprise-focused go-to-market strategy has secured multiyear sizable platform subscriptions, driving durable revenue growth as enterprises consolidate software supply chain tools, expected to strengthen revenues.

- The company’s cloud success, bolstered by strategic partnerships with cloud providers like AWS, Google Cloud, and Microsoft Azure, is expected to continue fueling cloud revenue growth, impacting overall revenue positively.

- JFrog’s integrated DevOps and security vision has attracted enterprise customers who are replacing point solution tools with JFrog's holistic security platform, potentially enhancing net margins due to higher-value, more comprehensive contracts.

- Investments in AI and MLOps, especially the acquisition of Qwak AI, position JFrog to capitalize on the growing demand for AI-driven technologies, expected to contribute to revenue growth as AI and security capabilities gain adoption.

- The shift towards larger enterprise customers is expected to lead to higher customer lifetime value and operating efficiencies, potentially improving net margins and sustaining earnings growth.

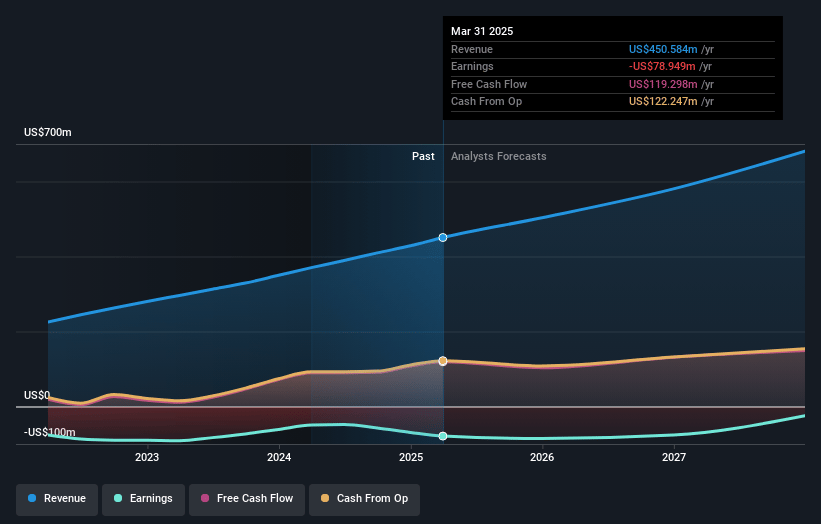

JFrog Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming JFrog's revenue will grow by 16.7% annually over the next 3 years.

- Analysts are not forecasting that JFrog will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate JFrog's profit margin will increase from -16.2% to the average US Software industry of 11.8% in 3 years.

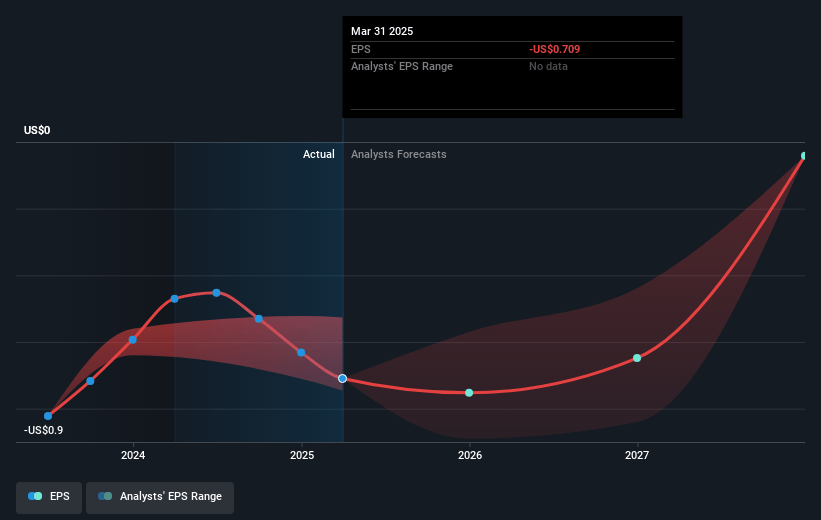

- If JFrog's profit margin were to converge on the industry average, you could expect earnings to reach $80.6 million (and earnings per share of $0.63) by about April 2028, up from $-69.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 88.3x on those 2028 earnings, up from -51.8x today. This future PE is greater than the current PE for the US Software industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 4.11% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

JFrog Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on large customer wins and multiyear commitments suggests potential volatility in revenue if such deals slow down, impacting consistent revenue growth.

- The company's heavy focus on cloud growth and migration assumes consistent customer commitment; any slowdown or hesitance in cloud adoption could adversely affect projected cloud revenues.

- A conservative guidance approach suggests possible caution regarding future financial performance, indicating potential concerns about achieving aggressive revenue targets.

- Tight budgetary environments and cautious customer spending could limit growth in cloud usage beyond minimum commitments, thus affecting long-term revenue and net margins.

- Heavy investments in non-GAAP measures point to significant costs that could strain net margins and earnings if not managed alongside revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $45.0 for JFrog based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $50.0, and the most bearish reporting a price target of just $39.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $681.1 million, earnings will come to $80.6 million, and it would be trading on a PE ratio of 88.3x, assuming you use a discount rate of 7.6%.

- Given the current share price of $31.8, the analyst price target of $45.0 is 29.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.